Unlike most trade deals where the terms are readily available, the details of the Phase One trade agreement between China and the U.S. will not be announced nor signed in public.

Accordingly, investors are left to cobble together official comments, anonymous statements from officials, and rumors to ascertain how it might affect their portfolios.

Based on official and unofficial sources, existing tariffs will remain in place, new tariff hikes will be delayed, and China will purchase $40-50 billion in agricultural goods annually.

At first blush, the “deal” appears to be a hostage situation- China will buy more goods in exchange for tariff relief.

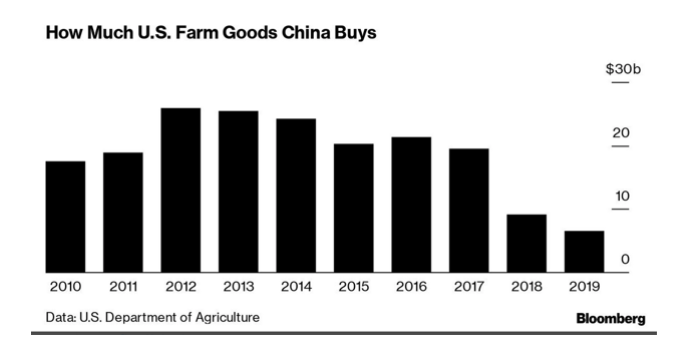

The chart below, courtesy of Bloomberg, provides reasons for skepticism. The rumored $40-50 billion in goods is nearly double what China purchased from the U.S. in any year of the last decade.

It is over four times what they bought in 2018 before the trade war started in earnest.

The commitment is even more questionable when one considers that China recently agreed to purchase agricultural products from Brazil, Argentina, and New Zealand.

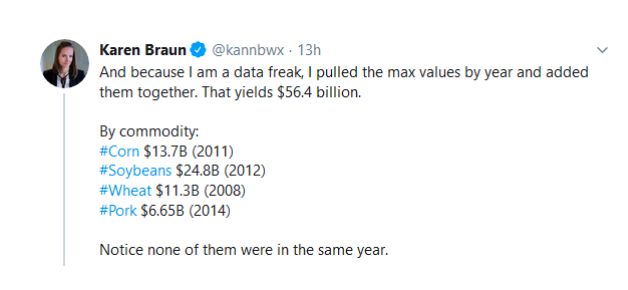

The following tweet by Karen Braun, (@kannbwx), a Global Agricultural Columnist for Thomson-Reuters, puts the massive commitment into further context. She claims that the maximum annual totalimport of four key agriculture products, only adds up to $56 billion. As she stresses in the tweet, the figures are based on the maximum amount China bought for each respective good in any one year.

Either China will buy more agriculture than they need and stockpile a tremendous amount of agriculture, which is possible, or they have agreed to something else that is not being disclosed. That, to us, seems more likely. We have a theory about what might not be disclosed and why it may matter to our investment portfolios.

Donald’s Dollar

Given the agreement as laid out in public, what else can China can offer that would satisfy President Trump? While there are many possibilities, the easiest and most beneficial commitment that China can offer the U.S. is a stronger yuan, and thus, a weaker dollar.

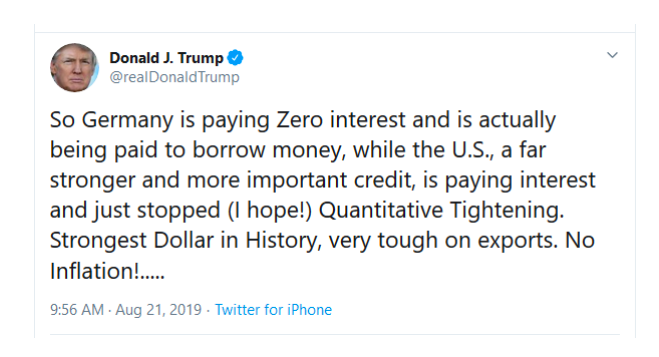

The tweets below highlight Trump’s disdain for the strengthening dollar.

A weaker dollar would reduce the U.S. trade deficit by making exports cheaper and imports more expensive. If sustained, it could provide an incentive for some companies to move production back to the U.S. This would help fulfill one of Trump’s core promises to voters, especially in “fly over” states that pushed him over the top in the last election. Further, a weaker dollar is inflationary, which would boost nominal GDP and help satisfy the Fed’s craving for more inflation.

From China’s point of view, a weaker dollar/ stronger yuan would hurt their exporting sectors but allow them to buy U.S. goods at lower prices. This is an important consideration based on what we wrote on December 11, in my firm’s RIA Pro daily Commentary:

“In part, due to skyrocketing pork prices, food prices in China have risen 19.1% year over year. In addition to hurting consumers, inflation makes monetary stimulus harder for the Bank of China to administer as it is inflationary. From a trade perspective, consumer inflation will likely be one factor that pushes Chinese leaders to come to some sort of Phase One agreement.”

Food inflation is a growing problem for China and its leadership. In part, due to the issues in Hong Kong, Chairman Xi benefits from pleasing his people. While a stronger yuan would result in some lost trade and possibly jobs, the price of the agricultural goods will be lower which benefits the entire population.

A stronger yuan is not ideal for China, but it appears to be a nice tradeoff and something that benefits Trump. This is speculation, but if correct, and recent weakness in the dollar suggests it is, then we must assess how a weaker dollar affects our investment stance.

Investment Implications

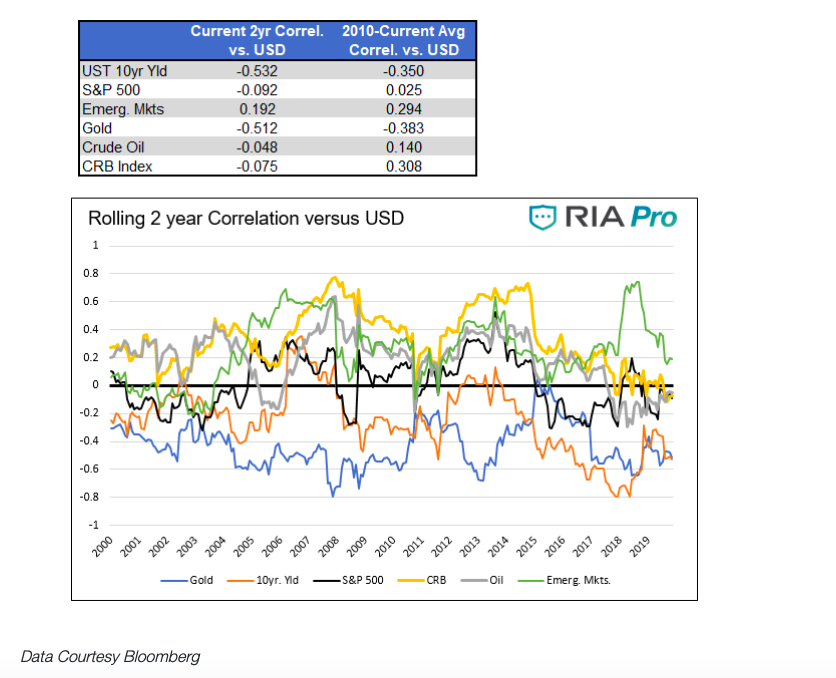

The following table shows the recent and longer-term average monthly correlations between the U.S. dollar and various asset classes. Below the table is a graph that shows the history of the two-year running monthly correlations for these asset classes to provide more context.

Twitter: @michaellebowitz

Any opinions expressed herein are solely those of the author, and do not in any way represent the views or opinions of any other person or entity.

: Worrisome to Broader Market?")