- Tech capex and geopolitics have dominated the headlines this year, but opportunities emerge elsewhere

- Dividend growth investing could be hitting its stride amid shifting macro and micro trends

- Novel, forward-looking strategies may help asset allocators find alpha beyond traditional income approaches

The corporate world is awash in capex. Leaders in the artificial intelligence (AI) arms race are pouring hundreds of billions of dollars into tech projects, and uncertainty surrounds their profitability. For now, the market rewards this use of cash, but it’s not without pitfalls. Share buybacks, for instance, are seen as a net loser, while the S&P 500® dividend yield has sunk toward all-time lows near 1%.

Away from the AI mega-theme, cyclical and even defensive areas of the global stock market have unique stories. Sectors such as Financials, Energy, and Industrials remain quite shareholder-friendly, as evidenced by rising dividend payouts and robust yields, particularly outside the U.S.

Indeed, global investors may be well served by widening their geographic aperture to find resilient income plays. That’s what the TMX team will do this week. Join us on Thursday, June 25, for an in-depth look at spotting resilient income ideas. Our indexing, quantitative research, and data strategy experts will explore how advanced predictive forecasting (not backward-looking data) redefines index construction.

We’ll showcase the S&P/TSX Composite High Dividend Growth Index, highlighting its next-generation construction process and how corporate payout shifts can help traders, investors, and global portfolio managers assess risk.

Dividend Growth Isn’t Dead

Leading into the event, dividend growth has seemingly been cast aside by the market. Income investors are finding fewer dividend-growth ideas, and even companies with a long track record of increasing their payouts have seen their stock prices lose ground to high-capex names.

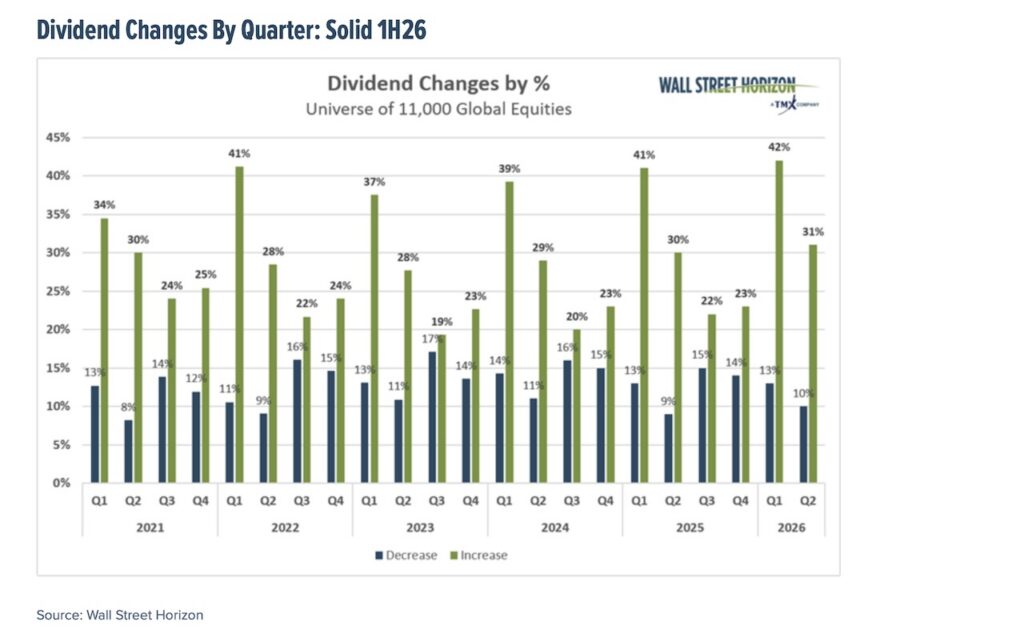

But here’s the good news: Wall Street Horizon’s data reveal that a solid 31% of global firms lifted their dividends this quarter. That’s fractionally higher than 30% in Q2 2025. And while we are not quite halfway through the year, we track an uptick in net dividend increasers year to date through the solstice. So maybe it’s not all about pouring operating cash flow into semiconductors, DRAM memory, and agentic AI projects.

It turns out there are plenty of dividend-growth ideas out there… we just have to know where to look.

Dividend Changes By Quarter: Solid 1H26

The panel will delve into that topic on Thursday. Of course, dividend aristocrats are not only for income investors. So-called “growth at a reasonable price” portfolio management goes hand in hand with dividend-growth. Analyzing companies with potential top- and bottom-line strength in the years ahead might matter more than decades of dividend policy for modern asset allocators.

This mix of forward-looking estimates and historical capital-discipline scoring shapes the S&P/TSX Composite High Dividend Growth Index.

A Different Approach to Dividend-Growth Investing

Another defining feature of the Index is its weighting scheme. Some arguably riskier income mutual funds and ETFsweight purely by dividend yield, which can result in “accidental high-yielders” creeping to the top of the portfolio. Other, more traditional dividend strategies rank equity holdings by market capitalization, which might turn a product into more of a broad index fund.

The S&P/TSX Composite High Dividend Growth Index, by contrast, first selects eligible positions based on the highest forecasted dividend-yield growth and then weights them by yield. As a result, unlike standard backward-looking dividend aristocrat indices that screen strictly for historical growth, this index integrates forward-looking metrics to capture accelerating payouts.

Financials & Energy In Focus

Returning to the sector discussion, Financials and Energy currently command the largest Index stakes. Banks and other financial institutions may be taking a more conservative approach in today’s uncertain macro backdrop, while oil and gas companies face volatility in WTI and Brent, along with the key LNG market.

Perhaps for these reasons, shareholders are top of mind, rather than risky capex projects.

Trading Catalyst: The Q2 Earnings Season

We’ll find out more in just a few weeks. In the U.S., JPMorgan Chase (JPM) unofficially kicks off the Q2 reporting season. CEO Jamie Dimon and his team will post revenue and earnings figures on Tuesday, July 14, BMO. Before that, early bellwether reports include PepsiCo (PEP) on the Thursday morning after Independence Day, followed the next day by Delta Air Lines (DAL).

That trio of earnings movers could also shed light on non-tech capital-allocation trends. JPM is, of course, from the Financials sector, while PEP is a Consumer Staples stalwart and DAL resides in Industrials. Along with Utilities, those are among the Index’s top sector allocations.

Jobs, Inflation, and the Fed

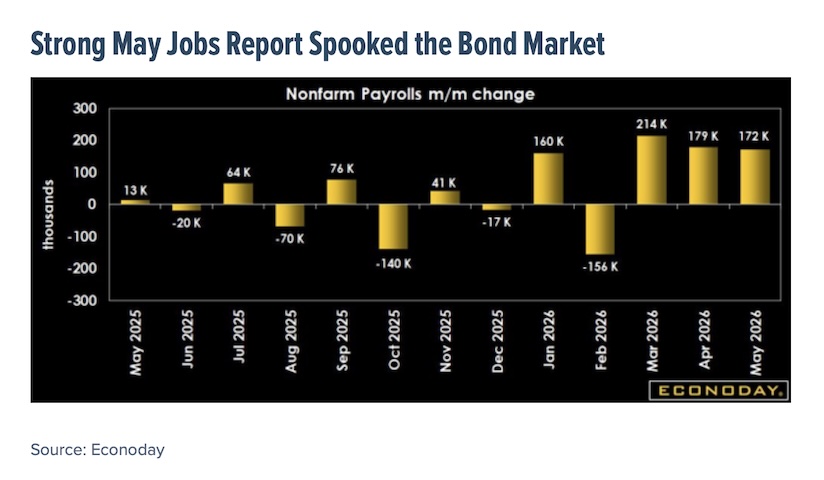

Ahead of earnings season, key U.S. jobs data arrive on Thursday, July 2. Recall that the May employment numbers were strong across the board, though a portion of the 172,000-payroll gain may have been due to seasonal and one-off hiring in advance of the FIFA World Cup 2026. Economists forecast June job growth, while the unemployment rate could remain relatively steady in the low-to-mid-4% range.

Taken together with this week’s May PCE inflation data, investors should soon have more information regarding potential moves by Fed Chair Kevin Warsh and the rest of the FOMC.

Strong May Jobs Report Spooked the Bond Market

Watching Oil and Consumer Sentiment

Geopolitical strategists remain fixated on developments in the Middle East as well. Brent and WTI crude oil have dipped into the $70s per barrel, and gas prices in the U.S. have been in full retreat mode in recent weeks, now below $4 per gallon.

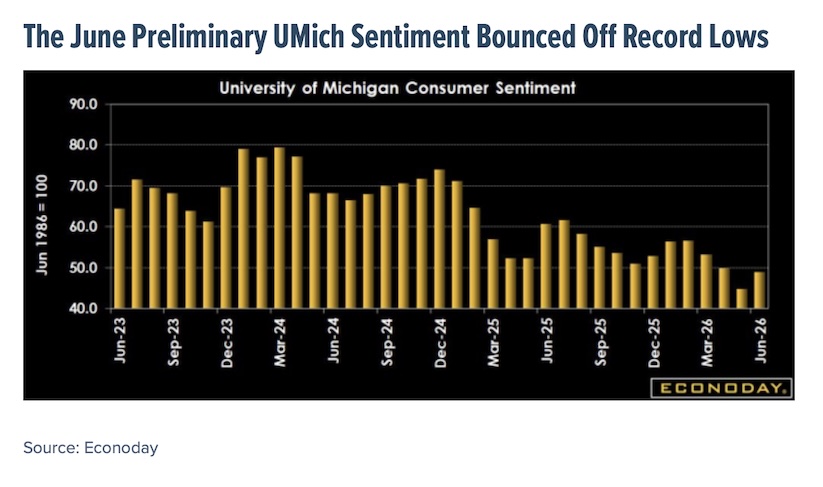

Consequently, this Friday’s final June reading of the University of Michigan Consumer Sentiment Index could see a modest uptick. Maybe it even gets a boost from all the SpaceX (SPCX) hoopla.

The June Preliminary UMich Sentiment Bounced Off Record Lows

The Bottom Line

There’s plenty for market participants to digest as we approach midyear. The AI trade has been volatile but generally up and to the right, while geopolitics unexpectedly became the macro focus during the first half of the year. Going forward, investors should consider new alpha strategies to diversify their exposure and manage risk.

Join us this Thursday to dive deeper into how predictive modeling can be harnessed to identify alpha opportunities.

Twitter: @ChristineLShort

The author may hold positions in mentioned securities. Any opinions expressed herein are solely those of the author, and do not in any way represent the views or opinions of any other person or entity.