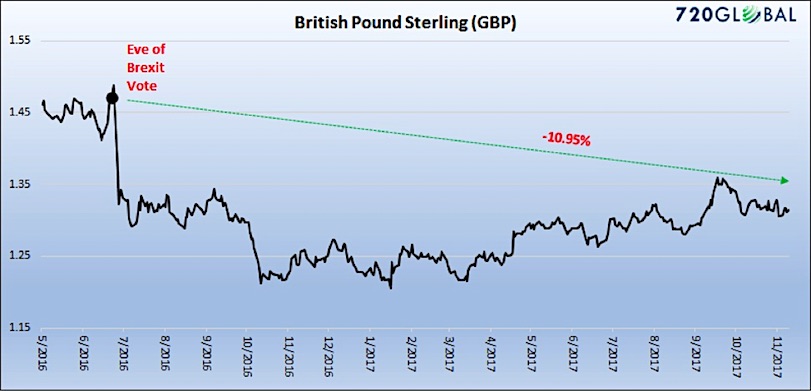

Conversely, what has not recovered is the currency of the United Kingdom (chart below).

The British Pound Sterling (CURRENCY:GBP) closed at 1.4877 per U.S. dollar on June 23, 2016, and dropped by 15 points (-10%) to 1.33 by the end of the month following the Brexit vote. Over the past several months the pound has fallen to as low as 1.20 but more recently it has recovered to 1.33 on higher inflation readings and hawkish monetary policy language from Bank of England (BoE) governor Mark Carney. Despite following through on his recent threats to hike interest rates, the pound has begun to again trend lower.

Data Courtesy: Bloomberg

Carney has voiced concern over Brexit-induced inflation by saying that if global integration in recent decades suppressed price growth then the reduced openness to foreign markets and workers due to Brexit should result in higher inflation. This creates a potential problem for the BoE as a disorderly exit from the EU hurts the economy while at the same time inducing inflation. Such a stagflation dynamic would impair the BoE’s ability to engage in meaningful monetary stimulus of the sort global financial markets have become accustomed since the financial crisis. If the central bankers lose control of inflation, QE becomes worthless.

Some astute observers of the currency markets and BoE pronouncements argue that Carney’s threat of rate hikes are aimed at halting the deterioration of value in the pound and preventing a total collapse of the currency. That theory is speculative but plausible when analyzing the chart. Either way, whether the pound’s general weakness is driven by inflation concerns or the rising risks associated with a hard Brexit, the implications are stark.

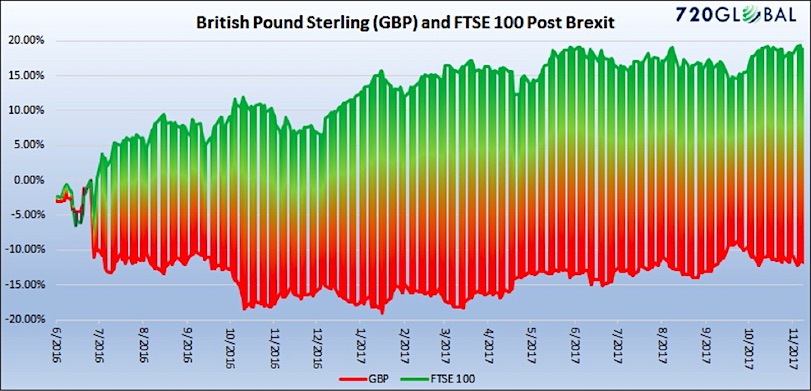

What is equally evident, as shown below, is the laissez-faire attitude of the FTSE as opposed to the caution and reality being priced in by the currency markets. In Lehman’s case, the stock market was similarly complacent while the ten year Treasury yield dropped by nearly 2.00% from June 2007 to March 2008 (from a yield of 5.25% to 3.25%) on growing economic concerns and a flight-to-quality bid.

Data Courtesy: Bloomberg

A Familiar Problem

As discussed above, the Bank of England may find itself in a predicament where it is constrained from undertaking extreme measures due to inflation concerns or even being forced to tighten monetary policy despite an economic slowdown. Those actions would normally serve to support the pound. Further, if the prospect of a hard Brexit continues to take shape, capital flight out of the UK may overwhelm traditional factors. In efforts to prevent the disorderly movement of capital out of the country, the BoE may be required to hike interest rates substantially. Unlike the resistance of equity markets to bad news, the currency markets are more inclined, due to their size and much higher trading volume, to fairly reflect the dynamics of the economy and the central bank in a reasonable time frame.

Our perspective is not to presume a worst case scenario but to at least entertain and strategize for the range of possibilities. Equity markets, both in the UK and throughout the world, transfixed by the shell game of global central bankers’ interventionism, are clearly not properly assessing the probabilities and implications of a hard Brexit.

All things considered, the pound has rallied back to the high end of its post-Brexit range which seems to suggest the best outcome has been incorporated. If forced to act against inflation, the Bank of England will be hiking rates against a stagnant economy and a poor economic outlook. This may provide support for the pound in the short term but it will certainly hurt an already anemic economy in the midst of Brexit uncertainty.

Summary

Timing markets is a fool’s errand. Technical and fundamental analysis allows for an assessment of the asymmetry of risks and potential rewards, but the degree of central bank interventionism is not quantifiable. With that premise in mind, we can evaluate different asset classes and their adherence to fundamentals while allowing a margin of error for the possibility of monetary intervention. After all, if central banks print money to inflate asset prices to create a wealth effect, some other asset should reveal the negative effects of conjuring currency in a fiat regime – namely the currency itself. In the short term, it may appear as though rising asset prices create new wealth, but over time, the reality is that the currency adjustments off-set some or all of the asset inflation.

Investors should take the time, while it is available, to consider the gravity of the disruptions a hard Brexit portends and look beyond high flying UK stocks to the more telling movement of the British pound. Like with Lehman and the global financial system in 2008, stocks may initially be blind to the obvious. Although decidedly not under the threats present during World War II, the British Government and the EU lack the leadership of that day and will likely need more than central banker propaganda to weather the economic storm ahead.

Keep calm and carry on, indeed.

Twitter: @michaellebowitz

Any opinions expressed herein are solely those of the author, and do not in any way represent the views or opinions of any other person or entity.

– Warren Buffett’s Biggest Holding!")