On July 20, 2015 we wrote a strategic article entitled “Finding Value in the Ninth Inning of the Great Bond Rally” which made the case for an investment in closed end mutual funds (CEF’s) backed by municipal bonds. This article reviews the original investment thesis, updates the reader on the performance and attributes of these securities and concludes with some thoughts on what investors may want to do with these positions.

In the original article, we analyzed 50 muni-backed CEF’s in order to select a manageable sub-set of securities offering the most potential. The analysis supporting the recommendation relied upon many self-imposed factors and risk constraints, many of which we will not rehash in this article and some of which we did not detail in the prior article.

Time to Extract Value from Our Prior CEF Investment Recommendation

There are three factors, however, which are worth reviewing as we evaluate and potentially change our investment thesis and recommendation to our clients. They are as follows:

- Discount to Net Asset Value (NAV) – Closed end funds frequently trade at a premium or discount to their net asset value (current market value of the securities held by the fund). One of the driving factors behind our investment decision was the fact that many muni-backed CEF’s were trading at historically large discounts to their NAVs. We believed at that time, barring severe credit dislocations in the municipal bonds sector that CEF investors would benefit from the normalizing discounts.

- Interest Rate Forecast – We have written numerous times that we expect the U.S. economy will continue to be plagued with weak economic growth and increasing deflationary pressures. Such an environment typically bodes well for fixed income assets, specifically those that are investment grade. This theory which would result in even lower interest rates was another factor supporting our recommendation.

- Municipal Bonds Yield Spread to Treasuries – Like all bonds, municipal bonds trade at a yield spread, or differential, to U.S. Treasury bonds. Statistically, the relationship between municipal bond yields and Treasury bond yields exhibits a strong correlation. The spread can help astute investors create more dependable risk/reward forecasts. When the original paper was written, we calculated that municipal bonds were trading at a premium versus U.S. Treasury bonds. While the risk existed that the yield spread would normalize, we thought the advantages of the discount to NAV and our overriding interest rate forecast would more than offset the potential yield spread risk.

Performance and Investment Attributes

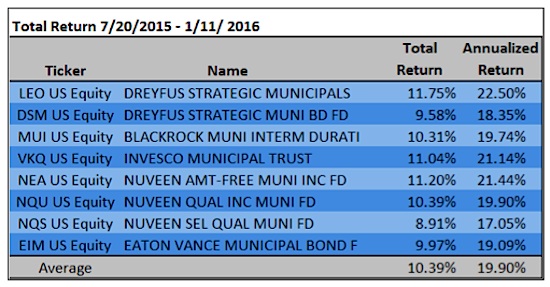

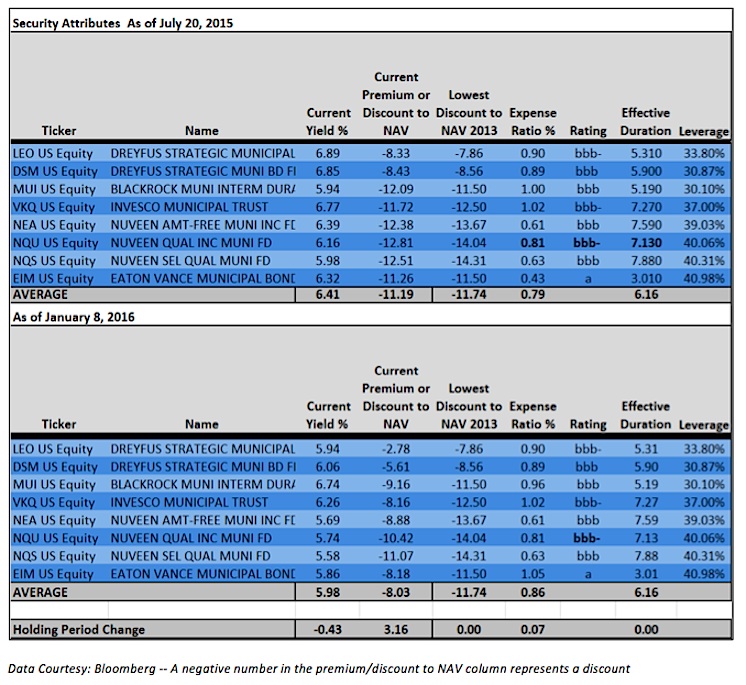

Since recommending the trade, the selected CEF’s have performed very well. The first table below highlights the performance of the CEF’s and the second set of tables, on the following page, compares the original attributes table to an updated version.

Within the tables are a few points worth detailing.

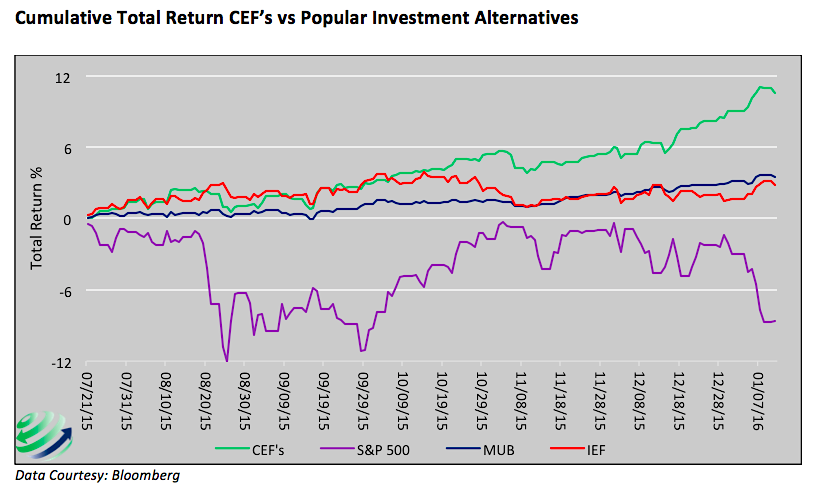

First, the CEF’s, on average, have a total return of +10.39% or nearly +20% annualized. The graph below compares the cumulative total return of the CEF’s to that of the S&P 500 (-8.64%), IEF a 7-10 year U.S. Treasury ETF (+2.82%), and MUB a municipal bonds ETF (+3.51%). The returns include both price appreciation and dividends.

Second, the discount to NAV, for all of the securities, improved. The CEF’s, on average, witnessed a 3% decrease in the discount. Think of this as appreciation in the value of the fund above and beyond changes to the value of the fund’s holdings. While all of the securities still trade at attractive discounts, they are currently trading back in line with their 3 year average.

Third, the CEF’s also benefited from a drop in yields during this holding period. The lower CEF yields were a function of the aforementioned decrease in the discount to NAV, as well as a general move lower in municipal bonds yields and Treasury yields. During the period, the average yield on the selected CEF’s fell by .43% while comparable Treasury yields fell by .22% and the Bond Buyer GO 20 Municipal Bonds Index fell by .32%. The bonds underlying the funds, likely saw yields on average decrease more than Treasury bonds during this period. In bond market parlance one would say the municipal -Treasury yield spread tightened or became richer, to the benefit of municipal bond holders.

Investment Review

As previously mentioned at the time we wrote the article we were comfortable with the risk that municipal bond yields might underperform Treasury bond yields. Our thought being that any widening of municipal/Treasury spreads would likely be more than offset by our expectation for lower yields in general and the normalization of discounts to NAVs.

continue reading on the next page…

: Showing Some Signs of Emerging Strength")