Not As Advertised

The flexibility and customizability offered through the world of index mutual funds and ETFs is remarkable. As such, there is a natural inclination by investors to assume that one will get precisely what has been advertised by these funds.

However, confidence in that idea is easily challenged. Much of what has been developed over the past several years, especially with many ETFs, remains untested. The following are concerns investors should be aware of:

Tracking Error: ETF exposures to certain markets might not be precisely what the investor receives. For example, it has been documented that an investor who wishes to invest in an ETF for the equity market in Spain actually gets exposure to a variety of companies that although domiciled in Spain, produce most of their revenue outside that country. In that instance, and many others like it, an investor would not get the exposure to Spain he or she expects and may indeed be very disappointed in the ETFs tracking of the index for Spain.

Optimization: The structure of index funds and ETFs are such that in many cases the fund managers are only able to establish positions in the underlying stocks or bonds of the indexes they track with some imprecision. This means they will use creative means of gaining desirable exposures and then gradually, if possible, reposition over time in order to more closely track the index. This tends to be a much bigger problem for bond funds. Since full replication of a bond index is generally not possible, bond funds rely on “optimizing” the portfolio in order to most effectively replicate the index.

Bond offerings, like stocks, are finite so if the size of a fund grows as a percentage of the underlying index constituents, it will increasingly face the constraint of replicating the index and effectively mimicking index performance. Optimization is imperfect so the ETF will suffer performance drift from the target index. Unfortanately, the flaws of replicating are often exagerated during periods of market stress when investors expectations are the highest.

Underlying Liquidity: Another related issue that arises with bond funds is that of establishing daily market value. The market price of some bonds held in a fund, especially those that are investing in less liquid markets, may not be readily available. If a bond fund holds securities that are illiquid, meaning they do not trade very often, then a realistic current price may be difficult to obtain. Many fixed income ETFs hold thousands of securities some of which do not trade daily or even weekly.

This means that pricing is dependent upon estimatesof the value on those bonds. These estimates of value may be derived from a third-party pricing service, surveys of bond market trading desks and internally generated models. Mis-pricing of securities is a known problem and one not typically considered until the fund is forced to sell. If the fund receives an inordinate number of redemption requests, what happens if they have bonds that do not trade very often but are nevertheless required to liquidate based upon investor requests? It is likely the sale price could vary, and sometimes significantly, from the last assumed price. Again this is most likely to occur at the wrong time for investors.

These concerns have not yet emerged as a deterent in the new age of passive investing popularity. We have only seen slight glimpses of what may be ahead in terms of challenges for the passive investor but it is fair to say this could be a major problem.

Investors naturally assume they will be able to exit as easily as they entered these funds and at the stated value seen on their statements or trading screens. In a calm market the concerns are minor but there are serious questions about that reality should a wave of selling hit bond ETFs all at once.

Although somewhat unique in its characteristics and certainly not a bond ETF, the recent debacle related to the inverse VIX ETF, XIV, seems to foreshadow some of the issues highlighted here. The graph below shows the price of XIV over the last two years. Investors unaware of how the NAV for XIV was calculated were certainly in for quite the shock.

Data Courtesy Bloomberg

Risk Analysis – The Benefit of Stress Testing

Given the importance of the issue of liquidity and what may transpire in an adverse scenario, we decided to look at the performance of a few ETFs and their related indices through the financial crisis as an indication of what a possible “worst-case” scenario might hold. In doing so, we acknowledge no two historical events are the same but the analysis seems important to consider.

From peak to trough, between April and November 2008, the Barclays Corporate Investment Grade index fell -10.8%. At the same time the LQD ETF which tracks that index fell -12.2%. The Barclays High Yield index fell -32.3%. In the same time frame the two high yield ETF alternatives, HYG and JNK, fell -29.8% and -34.5% respectively.

Today, these funds and others like them are much larger than they were in 2008. Furthermore, Bloomberg recently reported that many corporate debt funds are reaching further down the credit and liquidity spectrum in efforts to boost returns and some are even replacing high yield bond exposure with equities. As Lisa Abramowicz put it, “While this is somewhat concerning, it’s also logical. Fund managers don’t see any imminent risks on the horizon that could shake markets, and clients will penalize lower returns.”

The remarkable thing about this observation is that paying too high a price for an asset is in itself an imminent risk. One could convincingly argue that point as the most basic definition of risk. Nonetheless, it does indeed offer an accurate profile of the current character of the market. Unlike actively managed funds where the manager evaluates individual securities, there is no price discovery mechanism for index funds and ETF’s as their only consideration is whether or not they received a dollar to invest.

Summary

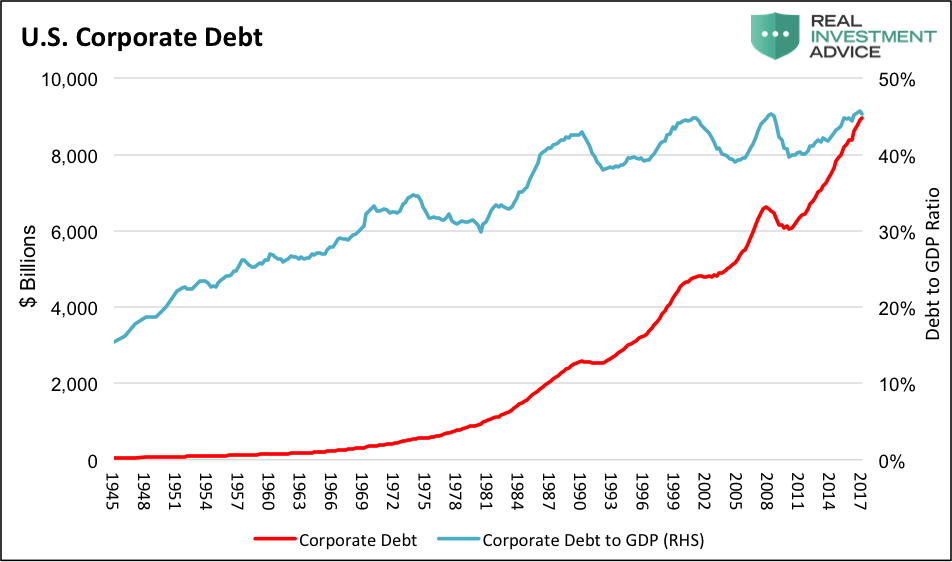

According to Benjamin Graham, this approach to putting money to work in the market defines the term speculation as it does not apply “thorough analysis” nor does it “promise safety of principal and an adequate return.” Although sympathetic to the idea that it is different this time as profit margins do indeed remain unusually high, the more defining characteristic is the means companies are using to sustain those profits. It is what has been referred to as corporate self-cannibalism as debt is ever accumulated as a means of buying back shares or paying dividends. The eventuality is credit downgrades and self-destruction.

Data Courtesy St Louis Federal Reserve

The cyclical nature of passive and active investing will continue to play out and that which is wildly popular today will eventually turn unpopular. The hidden risks embedded in passive vehicles will emerge and those who so enjoyed the cheap grace of effortless and exceptional market gains will end up begging yet again for mercy amid the markets’ unforgiving justice.

Twitter: @michaellebowitz

Any opinions expressed herein are solely those of the author, and do not in any way represent the views or opinions of any other person or entity.

: Showing Some Signs of Emerging Strength")