The Federal Open Market Committee (FOMC) ends its two-day Federal Reserve meeting today, the significance of which cannot be stressed enough. A lot is riding on this. After this Fed meeting, there will be two more left this year – one in late October and one in mid-December. What comes out of this meeting will decide if the remaining two will be viewed as insignificant or of consequence.

If the Federal Reserve hikes interest rates and then gives a nod and a wink that they are ‘one and done’, the remaining two this year will end up being nondescript. Risk-on assets could not be asking for more in this scenario. If on the other hand there is no hike in interest rates, but the Fed maintains its data-dependency posture, a sword of uncertainty will continue to hang over markets’ heads.

Which way might they go?

Prior to the August 11th yuan devaluation by China, it increasingly looked like the FOMC – at least a good majority of the voting members – was leaning toward a hike come the September Fed meeting. Now their message is not as uniform. Of late, there has been a distinct rise in volatility in global financial markets. The division among FOMC members has gotten quite stark.

At Jackson Hole, Stanley Fischer, Federal Reserve vice chair, hinted a September hike is still on the table. Just a few days before that, Bill Dudley, president of the New York Federal Reserve, was not so sure.

Staying with the U.S., the economy, as is the case with FOMC members, continues to send a conflicting message. In the end, their decision likely depends on what sets of data they give more weight to.

If between jobs and inflation the focus shifts to the former, the decision to hike interest rates becomes easier. If it is on inflation instead, the case for a ‘wait and see’ strengthens. Even within their dual mandate, there are conflicting signals.

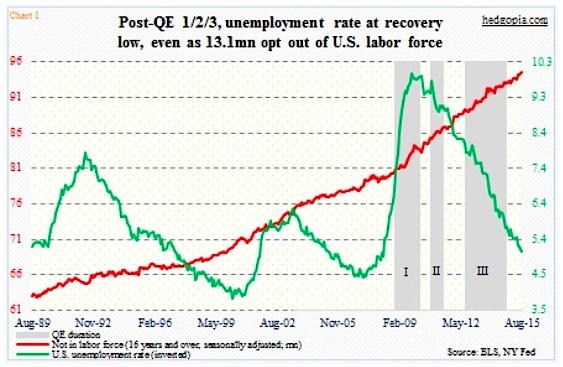

If they focus on the unemployment rate, it is a go, but not so if they consider for instance the number of Americans that have opted out of the workforce. In August, the unemployment rate dropped to 5.1 percent – nearly cut in half from 10 percent in October 2009 – but at the same time there are 94 million Americans that are not in the labor force, versus 81 million in June 2009 (Chart 1 above). Is Quantitative Easing (QE) – or zero interest-rate policy, for that matter – a success or a failure?

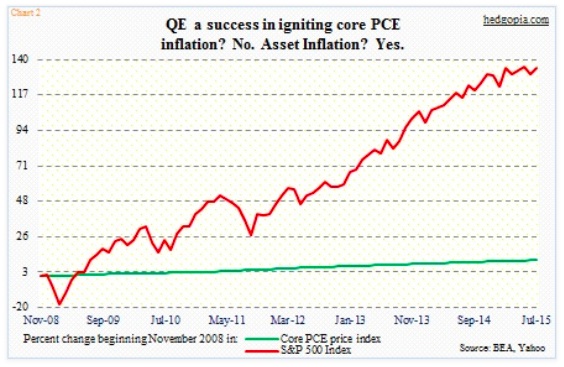

Within inflation, core PCE (personal consumption expenditures) inflation grew at a seasonally adjusted annual rate of 1.2 percent in August – the lowest since March 2011.

The last time it grew at two percent – the Fed’s stated goal – was in April 2012. The first iteration of QE was launched in November 2008, along with zero-bound Fed funds rate. Since then, the PCE price index has gone up a puny 10.3 percent.

The S&P 500 Index, on the other hand, has surged a massive 134.7 percent, pushing stocks higher (Chart 2 above).

continue reading on next page…