The following is a recap of The COT Report (Commitment Of Traders) released by the CFTC (Commodity Futures Trading Commission) looking at futures positions of non-commercial holdings. This was released within the January 29 Commitment of Traders report (with data through January 19). Note that the change in COT report data is week-over-week.

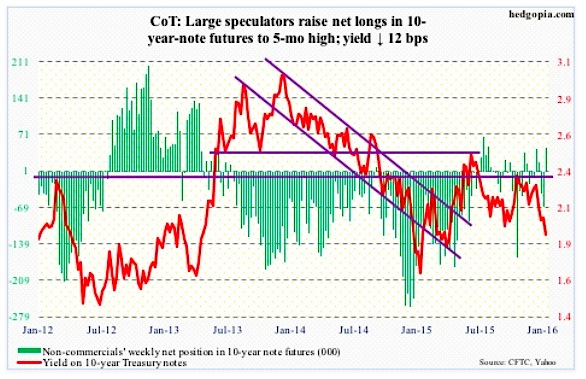

10-Year Treasury Note: Two important developments took place this week across the global central banking system.

First, the Federal Reserve. This week’s FOMC meeting was a non-event. No interest-rate decision was expected. At the same time, given the rout in stocks globally as soon as the year began, markets were hoping the Fed would dial back its rate-hike projection this year. It did not oblige.

Is the so-called Yellen put still good? Or is the message ‘we have done enough, now you are on your own?’

The FOMC statement did drop the median estimate for the normal rate of unemployment to 4.9 percent from a previous range of 5.2 percent to 5.5 percent. By doing so, it may be opening up the door to wait on interest rate hike, should the need be. As well, risks were no longer viewed as “balanced.” One can argue the Fed thinks recent global developments has increased downside risks for economic growth expectations.

Tough to say. The Fed statement was as vague as can be. It did not signal a March interest rate hike was imminent, but did not explicitly suggest it was off the table either, which is what markets were hoping for. Now the wait begins for Ms. Yellen’s February 10th semi-annual Congressional testimony for hopefully clearer signals.

Secondly, the Bank of Japan, in a five-to-four vote, lowered its target interest rate by 20 basis points to minus 0.1 percent. It was a surprise move, but Haruhiko Kuroda, BoJ governor, is probably not thrilled by markets’ reaction. On Friday, stocks were up, down and up again. The initial 3.1-percent euphoria in the stock market was gone within 28 minutes, followed by a drop of as much as 1.6 percent, before making a comeback and ending up 2.8 percent. This is not how it is supposed to happen. Markets should have embraced this wholeheartedly and gone full risk-on right from the word go.

Hence the question, are central banks pushing on a string and no longer getting the desired effect of their activism? Even worrisome, are markets beginning to conclude that central banks are pushing on a string? That would be a worrisome development.

For now, non-commercials rightly bet that rates were headed lower, with the 10-year losing 12 basis points.

January 29 Commitment of Traders Report: Currently net long 44.5k, up 112.3k.

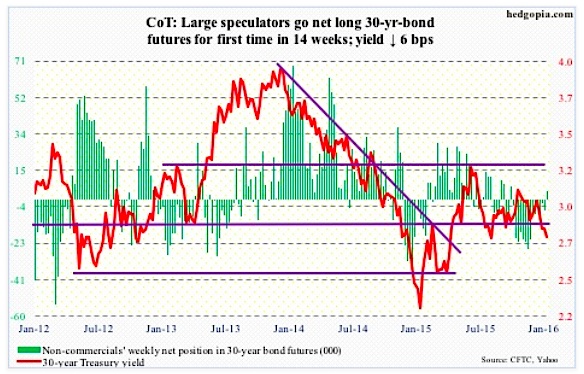

30-Year Treasury Bond: Major economic releases next week are as follows.

Personal income and spending data for December is due out on Monday. The core PCE price index – the Fed’s favorite measure of inflation – rose a mere 1.33 percent in November annually. The last time it increased at two percent was in April 2012. That said, it has been inching higher since 1.26-percent increase in July last year, which was the lowest since March 2011.

Also on Monday, we get ISM manufacturing index for December. It has been sub-50 for two consecutive months, the first time this has happened since July 2009. The new orders index, too, was under 50 in both November and December – the first such occurrence since May 2013.

The ISM non-manufacturing index comes out on Wednesday. It is still in expansion mode. The last time it dipped below 50 was in July 2009.

Preliminary productivity numbers for the fourth quarter will be published on Thursday. In 3Q15, non-farm output per hour increased 2.2 percent, revised up from previously reported 1.6 percent. Unit labor costs were revised up as well, rising 1.8 percent instead of previously reported 1.4 percent. The upward revision to productivity was smaller than a one-percentage point upward revision to hourly compensation growth.

Thursday also brings the full report on durable goods for December. The advance report came out this Thursday, and it was ugly. Orders for non-defense capital goods ex-aircraft were down 7.5 percent year-over-year – the sharpest decline since November 2009.

Friday is January’s employment report. Non-farm jobs momentum picked up steam in the fourth quarter, with monthly average gains of 284,000, much stronger than 2015 average of 221,000. Recent strength in job creation is yet to positively impact wages. The average hourly earnings of private-sector employees rose 2.5 percent annually in December. The last time the metric grew with a three handle was in April 2009. This Friday’s report will have implications for stocks.

January 29 Commitment of Traders Report: Currently net long 4.4k, up 10.2k.

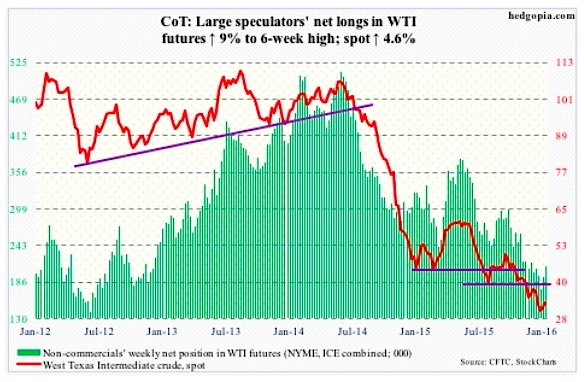

Crude Oil: The EIA report for the week of January 22nd was mixed at best and bearish at worst.

Crude oil production dropped by 14,000 barrels per day, to 9.22 million barrels per day. Last week was a 21-week high. Oil production peaked at 9.61 mbpd in the June 5th week.

Crude oil imports fell by 170,000 bpd, to 7.61 mbpd. In the past couple of weeks, imports have dropped by 579,000 mbpd.

Distillate stocks declined by 4.1 million barrels, to 160.5 million barrels. Two weeks ago, stocks (165.6 million barrels) were the highest since the January 21, 2011 week.

Now on to the negatives:

Refinery utilization fell by 3.2 percentage points, to 87.4 – a 14-week low. Utilization peaked at 96.1 percent in the August 7th week.

Gasoline stocks increased by 3.5 million barrels, to 248.5 million barrels. This was the 11th straight weekly increase, and at the highest since the March 2, 1990 week.

Even worse, crude oil stocks increased by 8.4 million barrels, to 494.9 million barrels – the highest ever (data goes back to 1982).

Spot West Texas Intermediate crude oil went on to rally 4.3 percent in the week. It was part fatigue – fatigue of going down – and part rumors of possible Russian willingness to discuss output cutbacks.

Later on Friday, talking to Bloomberg, Russian energy minister said Russia would participate in talks with both OPEC and non-OPEC nations that Venezuela has proposed for February. But there is no date and no confirmed meeting yet.

Saudi Arabia, by the way, continues to say it would continue to maintain its capital expenditures.

The Russians and the Saudis do not trust each other, with the former thinking the Saudis are in cahoots with the Americans and are out to get them. So we will see what comes out of these rumors.

For now, between the January 20th low and the 28th high, spot West Texas Intermediate crude oil rallied 26 percent. On Thursday, it rallied up to 34.82, before pulling back. Friday produced a doji. Getting past this resistance will be a sign that oil bulls are making progress. They have a tough task at hand.

Non-commercials continued to add this week, per the January 29 Commitment of Traders report. Two weeks ago, holdings were at the lowest since July 2012.

January 29 Commitment of Traders Report: Currently net long 210.9k, up 17.5k.

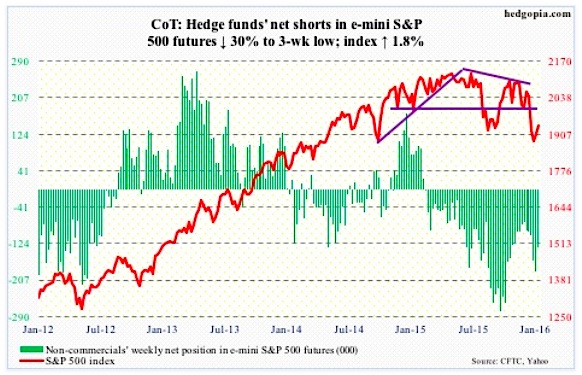

E-mini S&P 500: As of Wednesday, another $1.2 billion came out of U.S.-based equity funds (courtesy of Lipper). Year-to-date, outflows have now totaled north of $27 billion. Since September 30th, $36 billion has left.

This pretty much explains the 5.1-percent decline in the S&P 500 Index in January (was down as much as 11.3 percent at one point).

That said, there are some signs of buying interest in the stock market. For the week ended Thursday, $1.9 billion moved into the SPDR S&P 500 ETF (SPY) – courtesy of ETF.com. The ETF rose 1.7 percent for the week.

The path of least resistance on the S&P 500 continues to be 1990.

Shorts obviously have done well, and as of mid-January were not rushing to cover. Rather, on both the NYSE and Nasdaq, as well as several leading ETFs, short interest rose in the latest period – a potential recipe for a mini squeeze in stocks. We probably saw some of that on Friday.

Non-commercials, too, had raised net shorts to a 13-week high last week, and cut those down by 30 percent this week (per the January 29 Commitment of Traders Report).

January 29 Commitment of Traders Report: Currently net short 131.9k, down 56.7k.

continue reading on the next page…

")