That is all true, but every single time in history the 100-day dropped below the 300-day (as it did early in 2019) there were serious and legitimate fundamental concerns.

How do we know that?

The stock market declined in a manner that caused the 100-day to drop below the 300-day (a significant event requiring significant fundamental issues).

WHAT CAN WE LEARN FROM MARKET BREADTH?

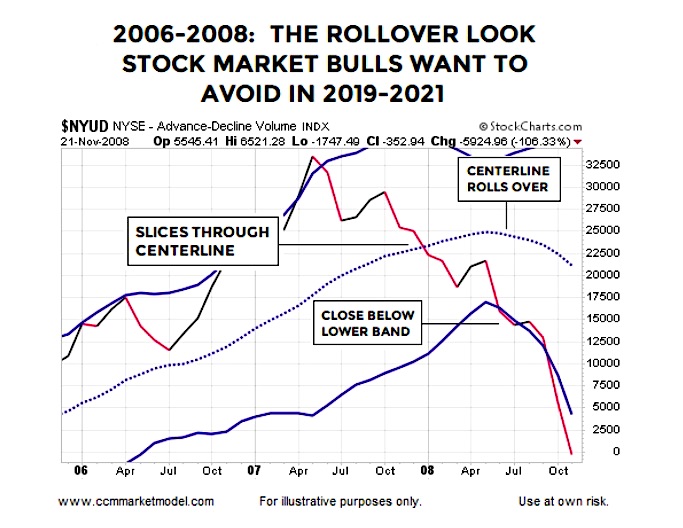

The 2006-2008 chart below shows NYSE advancing volume less declining volume near the stock market’s 2007 major peak. Three noteworthy factual events are shown on the monthly breadth chart below: (1) NYSE Advance-Decline Volume (NYUD) dropped below the Bollinger Band (BB) centerline, (2) NYUD closed below the lower BB, and (3) the BB centerline rolled over in a concerning manner.

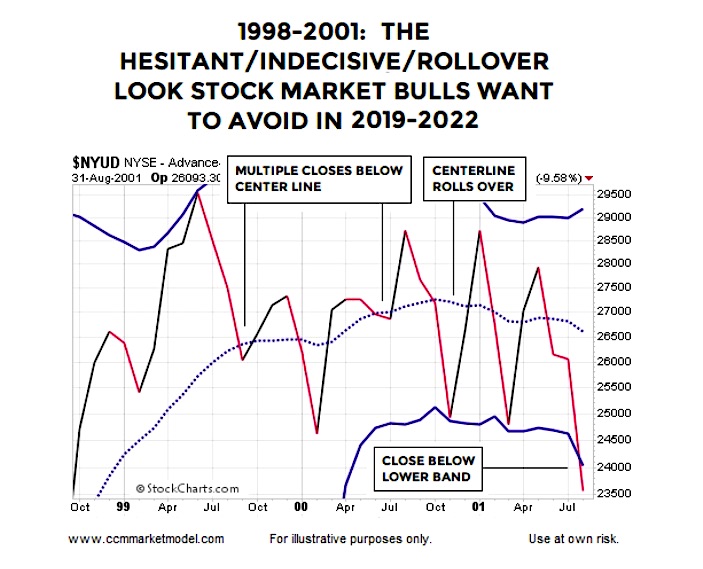

The same monthly breadth chart in 1998-2001 was a confused and indecisive mess, but ultimately all three boxes were checked (drop below centerline, close below lower Bollinger Band, and centerline rolled over).

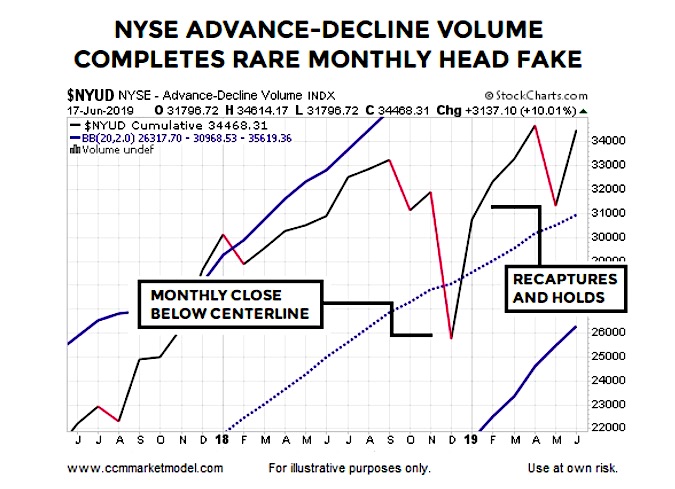

How does the same stock market breadth chart look today? The answer is a lot more constructive. After box one was checked (monthly close below the centerline), market breadth improved dramatically as noted on January 21, 2019.

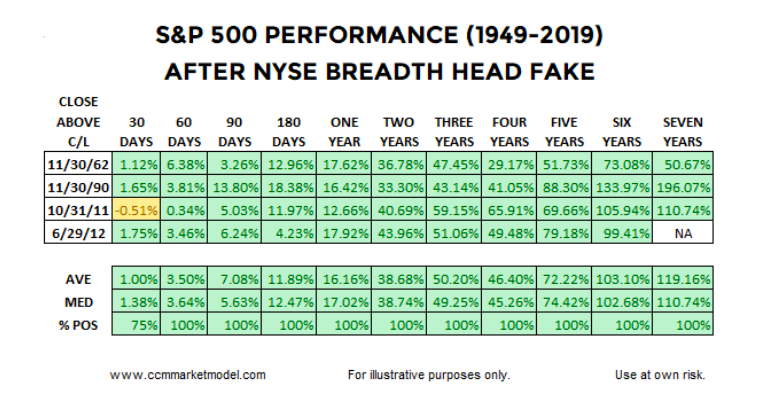

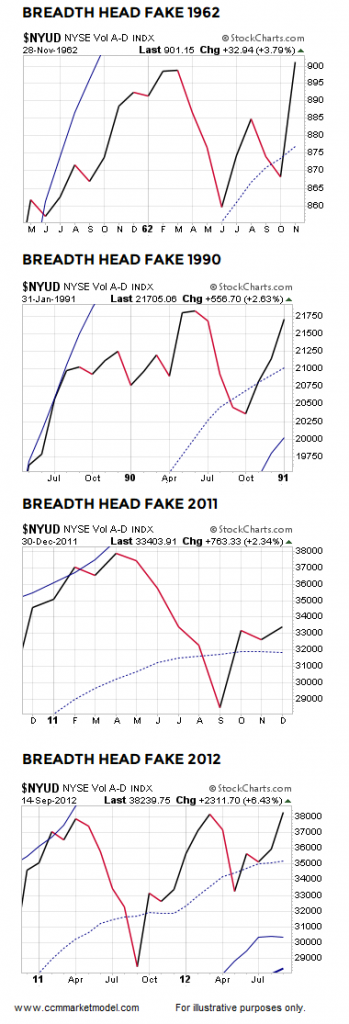

Dating back to 1949, how many times has a similar head-fake look appeared on the monthly chart of NYSE Advance-Decline Volume?The answer is four times: 1962, 1990, 2011, and 2012. What happened next in the stock market? After closing back above the monthly Bollinger Band centerline, good things happened in the historical cases looking out thirty days to seven years.

The charts below allow us to compare the 2019 stock market chart to the four previous market breadth head fake cases and the major stock peaks in 2000 and 2007.

Given what we know today, the present day looks more like the head fake cases relative to the major stock market top cases. If the present day chart morphs into something that looks more like 2000 or 2007, our concerns would increase. The historical cases (bullish and bearish) provide us with factual guideposts going forward, which speaks to the need for ongoing flexibility and open-mindedness.

WHAT DOES HISTORY SAY ABOUT THE FIRST INTEREST RATE CUT?

The market places high odds on the Fed cutting rates in either June or July. If so, it would represent the first rate cut since December 2008. Since some market participants have limited first-hand experience with the first rate cut in a new cycle, it might be helpful to review the longer-term history of Fed actions to lower the Federal Funds Rate.

This week’s video also reviews last week’s scary economic data point, allowing us to better understand subsequent historical S&P 500 performance.

WHAT ABOUT SMALL SAMPLE SIZES?

The limited sample size of the breadth cases above is what it is. We cannot control sample sizes. There have only been three 40%-plus declines in the S&P 500 since 1950 (1973-74, 2000-2002, and 2007-2009), which also represents a very small sample size. Are we supposed to totally ignore these major declines because of the small sample size? According to Reuters, the S&P 500 was officially launched on March 4, 1957, meaning any S&P 500 study deals with a very limited historical data set. It is what it is.

When we study rare events, we acknowledge the sample size and try to learn anything that can add value in the present day. The same concepts apply to the breadth case and trend studies above. There are countless economic and market studies that are based small sample sizes. Typically, the small sample size argument is only raised when the results run counter to someone’s personal opinion. When results agree with someone’s personal view, the small sample size is suddenly not a problem. If you believe a study or data set is irrelevant, there is an easy solution – ignore it.

MORAL OF THE STORY

The look of the S&P 500’s 100-day and 300-day aligns better with the major bottoms in 2002 and 2009 relative to the major tops in 2000 and 2007, telling us to remain open to longer-term bullish outcomes in theyearsahead. The rare breadth head fake also looks more like constructive cases in 1962, 1990, 2011, and 2012 relative to the concerning looks in 2007-2008 and 2000-2001. The studies above tell us very little about what could happen in the next two days or two weeks.

The market still has a Fed statement and press conference coming Wednesday and important dates remain on the trade calendar. Numerous market events in 2019 have aligned with bullish probabilities including those covered on February 19, March 3, March 22, April 3, April 15, April 22, and April 30. Thus far, nothing has transpired that significantly discounts the previous bullish-leaning setups, including the recent pullback that was in line with historical expectations. We will continue to take it day by day with an open mind about all outcomes from wildly bullish to wildly bearish.

“For all the concern about the economy, the spread between junk-rated U.S. bonds and Treasuries hovers at 390 points, below its five-year average of 441 points, signaling that anticipation of corporate defaults is going down.” — Bloomberg – June 18, 2019

Twitter: @CiovaccoCapital

The author or his clients may hold positions in mentioned securities at the time of publication. Any opinions expressed herein are solely those of the author, and do not in any way represent the views or opinions of any other person or entity.

: Showing Some Signs of Emerging Strength")