Outcome versus Process Strategies

It is that time of year when the markets play second fiddle to debates about which twelve seed could be this year’s Cinderella in the NCAA basketball tournament. For college basketball fans, this particular time of year has been dubbed March Madness. The widespread popularity of the NCAA tournament is not just about the games, the schools, and the players, but just as importantly, it is about the brackets. Brackets refer to the office pools based upon correctly predicting the 67 tournament games. Having the most points in a pool garners office bragging rights and, in many cases, your colleague’s cash.

Interestingly the art, science, and guessing involved in filling out a tournament bracket provides insight into how investors select assets and structure portfolios. Before explaining, answer the following question:

When filling out a tournament bracket do you:

A) Start by picking the expected national champion and then go back and fill out the individual games and rounds to meet that expectation?

B) Analyze each opening round matchup, picking winners and advance round by round until you reach the championship game?

If you chose answer A, you fill out your pool based on a fixed notion for which team is the best in the country. In doing so, you disregard the potential path, no matter how hard, that team must take to become champions.

If you went with the second answer, B, you compare each potential matchup, analyze each team’s respective records, strengths of schedule, demonstrated strengths and weaknesses, record against common opponents and even how travel and geography might affect performance. While we may have exaggerated the amount of research you conduct a bit, such a methodical game by game evaluation is repeated over and over again until a conclusion is reached about which team can win six consecutive games and become the national champion.

Outcome Based Strategies

Outcome-based investment strategies start with an expected result, typically based on recent trends or historical averages. Investors following this strategy presume that such trends or averages, be they economic, earnings, prices or a host of other factors, will continue to occur as they have in the past. How many times have you heard Wall Street “gurus” preach that stocks historically return 7%, and therefore a well-diversified portfolio should expect the same thing this year? Rarely do they mention corporate and economic fundamentals or valuations. Many investors blindly take the bait and fail to question the assumptions that drive the investment selection process.

Pension funds have investment return assumptions which, if not realized, have negative consequences for their respective plans. Given this seemingly singular aim of the fund manager, most pension funds tend to buy assets whose expected returns in aggregate will achieve their return assumption. Accordingly, pension funds tend to be managed with outcome-based strategies.

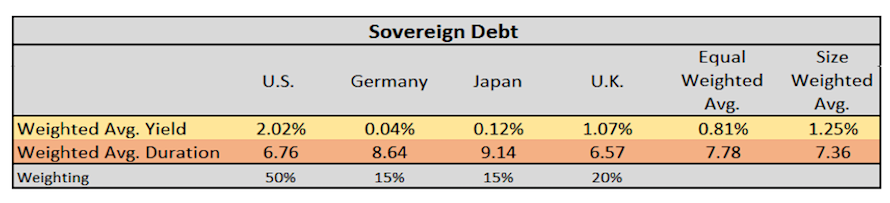

For example, consider a pension fund manager with an 8% return target that largely allocates between stocks and bonds.

Given the current yields in the table above, and therefore expectations for returns on sovereign bonds of approximately 1%, the manager must instead invest in riskier fixed income products and equities to achieve the 8% return objective. Frequently, a pension fund manager has a mandate requiring that the fund hold a certain minimum amount of sovereign bonds. The quandary then is, how much riskier “stuff” do they have to own in order to offset that return drag? In this instance, the manager is not allocating assets based on a value or risk/reward proposition but on a return goal.

To illustrate, the $308 billion California Public Employees Retirement System (CalPERS), the nation’s largest pension fund, has begun to shift more dramatically towards outcome-based management. In 2015, CalPERS announced that they would fire many of their active managers following repeatedly poor performance. Despite this adjustment, they still badly missed their 7.5% return target in 2015 and 2016. Desperate to right the ship, CalPERS maintains a plan to increase the amount of passive managers and index funds it uses to achieve its objectives.

In speaking about recent equity allocation changes, a CalPERS spokeswoman said “The goal is to eventually get the allocation to the right mix of assets, so that the portfolio will likely deliver a 10-year return of 6.2%.” That sounds like an intelligent, well-informed comment but it is similar to saying “I want to be in Poughkeepsie in April 2027 because the forecast is sunny and 72 degrees.” The precision of the 10-year return objective down to the tenth of a percent is the dead giveaway that the folks at CalPERS might not know what they’re doing.

Outcome-based strategies sound good in theory and they are easy to implement, but the vast amount of pension funds that are grossly underfunded tells us that investment policies based on this process struggle over the long term. “The past is no guarantee of future results” is a typical investment disclaimer. However, it is this same outcome-based methodology and logic that many investors rely upon to allocate their assets.

Process Based Strategies

Process-based investment strategies, on the other hand, have methods that establish expectations for the factors that drive asset prices in the future. Such analysis normally includes economic forecasts, technical analysis or a bottom-up assessment of an asset’s ability to generate cash flow. Process-based investors do not just assume that yesterday’s winners will be tomorrow’s winners, nor do they diversify just for the sake of diversification. These investors have a method that helps them forecast the assets that are likely to provide the best risk/reward prospects and they deploy capital opportunistically.

Well managed absolute return and value funds, at times, hold significant amounts of cash. This is not because they are enamored with cash yields per se, but because they have done significant research and cannot find assets that offer value in their opinion. These managers are not compelled to buy an asset because it “promises” a historical return. The low yield on cash clearly creates a “drag” on short-term returns, but when an opportunity develops, the cash on hand can be quickly deployed into cheap investments with a wider margin of safety and better probabilities of market-beating returns. This approach of subordinating the short-term demands of impatience to the long-term benefits of waiting for the fat pitch dramatically lowers the risk of a sizable loss.

A or B?

Most NCAA basketball pool participants fill out tournament brackets starting with the opening round games and progress towards the championship match. Sure, they have biases and opinions that favor teams throughout the bracket, but at the end of the day, they have done some analysis to consider each potential matchup. So, why do many investors use a less rigorous process in investing than they do in filling out their NCAA tournament brackets?

Starting at the final game and selecting a national champion is similar to identifying a return goal of 10%, for example, and buying assets that are forecast to achieve that return. How that goal is achieved is subordinated to the pleasant but speculative idea that one will achieve it. In such an outcome-based approach, decision-making is predicated on an expected result.

Considering each matchup in the NCAA tournament to ultimately determine the winner applies a process-oriented approach. Each of the 67 selections is based on the evaluation of comparative strengths and weaknesses of teams. The expected outcome is a result of the analysis of factors required to achieve the outcome.

Summary

It is very likely that many people filling out brackets this year will pick Villanova. They are a favorite not only because they are the #1 overall seed, but also because they won the tournament last year. Picking Villanova to win it all may or may not be a wise choice, but picking Villanova without consideration for the other teams they might play on the path to the championship neglects thoughtful analysis.

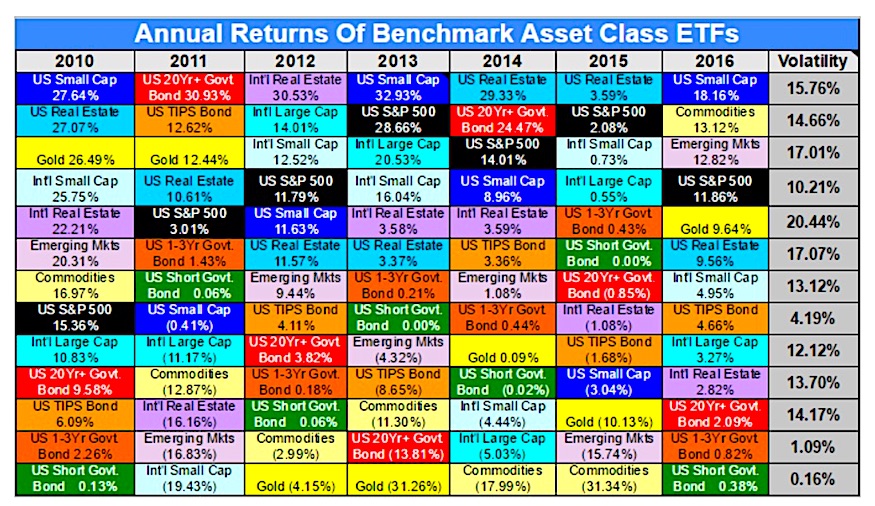

The following table (courtesy invest-assist.blogspot.com and Koch Capital) is a great reminder that building a portfolio based on yesterday’s performance is a surefire way to end up with sub-optimal returns.

Winning a basketball pool has its benefits while the costs, if any, are minimal. Managing wealth, however, can provide great rewards but is fraught with severe consequences. Accordingly, wealth management deserves considerably more thoughtfulness than filling out a bracket. Over the long run, those that follow a well-thought out, time-tested, process-oriented approach will raise the odds of success in compounding wealth by limiting damaging losses during major market set-backs and by being afforded opportunities when others fearfully sell.

Thanks for reading.

Twitter: @michaellebowitz

Any opinions expressed herein are solely those of the author, and do not in any way represent the views or opinions of any other person or entity.