Recap:In our first article we examined the ratio of the CBOE VXST Short-term Volatility Index (INDEXCBOE:VXST) to the CBOE VIX Volatility Index (INDEXCBOE:VIX) as a method to improve long entries in the S&P index. In last week’s article, we shared some preliminary numbers, using peaks in the ratio to identify opportune times to go long the SPY ETF.

This week we’ll use the ratio to identify opportunities for shorting the VIX Short-Term Futures ETN (NYSEARCA:VXX).

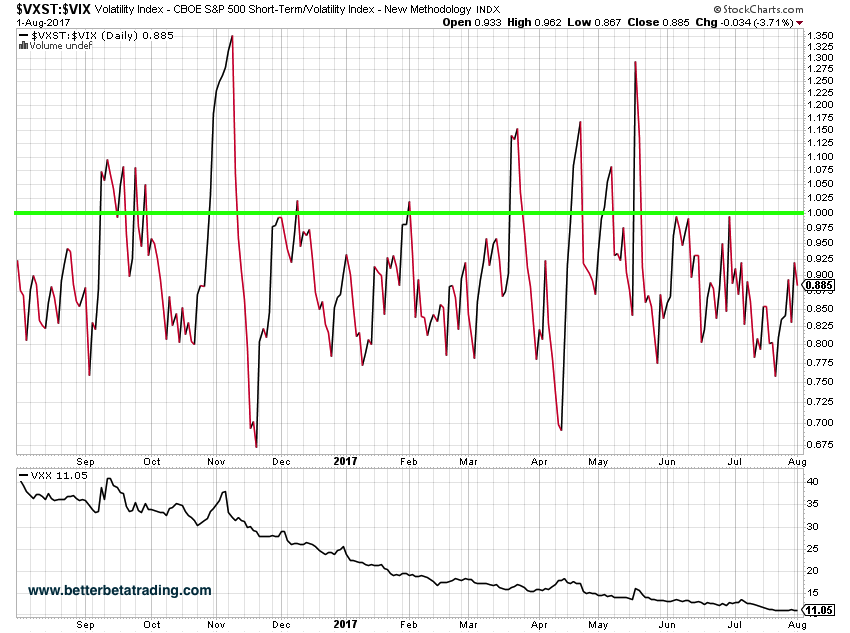

As reference, here’s a look at the ratio:

VXST:VIX Volatility Ratio Chart

Our Next Test: Using The Ratio For Shorting VXX

This week we are exploring some preliminary numbers as we test another way to capitalize on the ratio – shorting VXX. In the interest of making a direct comparison, we used the same logic to identify the peak as we did in last week’s long SPY test:

– Wait until the ratio and the ratio’s 5 day simple moving average (MA) is above 1.0.

– When the ratio moves below the 5 day MA, short the VXX ETN.

– Track the returns over 5, 10, 15 and 30 day holding periods.

– Include any concurrent trades (i.e., if the signal fires while the previous short VXX entry is still on, take the additional trade).

And like the previous articles in the series, we have to remind our readers that this is not a trading system – we are simply exploring the viability of using this ratio to build a system. Far more work would need to be done before real money put to work, particularly on the use of smarter exits. As you’ll see from the results below, the VXX is far more volatile than the SPY and requires thoughtful risk management.

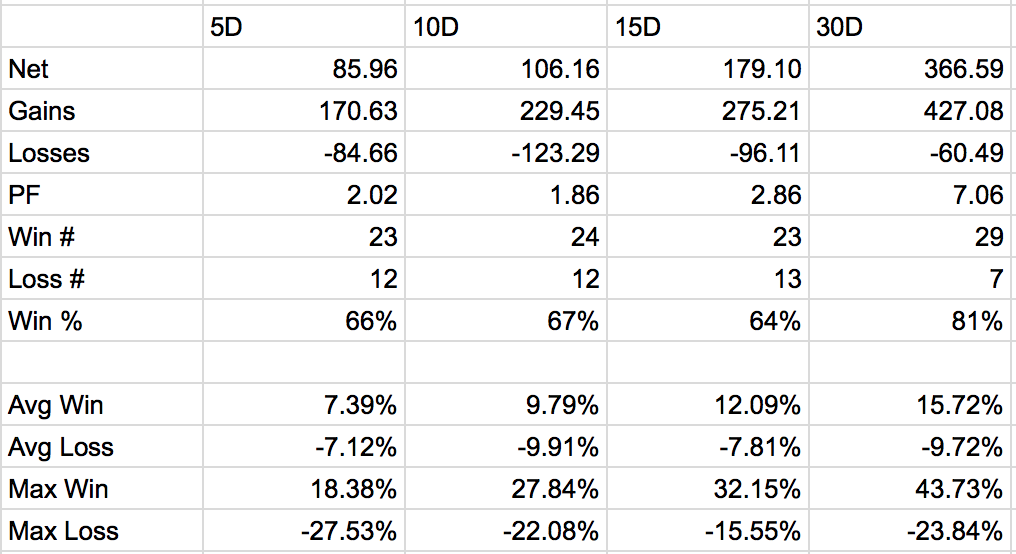

Results:

Overall, the study for shorting VXX was profitable for all holding periods. The win rates and profit factors (“PF” in the table) were similar across the long SPY and short VXX tests, with stronger results coming in the 15 and 30 day holding periods. Shorting VXX had significantly larger swings in average and maximum win and loss sizes (on a percentage basis).

Over the 15 and 30 day holding periods, the average wins and max wins were nearly double the size of the average and max losses, suggesting that longer hold times allow volatility to dissipate, making the need to pick the volatility precise peak less important. This size difference was not as pronounced in last week’s SPY long tests.

Conclusion:

While we ran our initial test on a short VXX position, a trader would want to explore other methods to short S&P index volatility. This could be accomplished by buying puts and/or selling call spreads on the VXX, depending on the desired delta exposure. A trader could go long an inverse volatility ETF like XIV or the leveraged SVXY. The use of VIX futures, options on VIX futures or SPX/SPY options offer additional ways to express a short volatility thesis, with each approach offering distinct benefits (and drawbacks).

Thanks for reading!

Any opinions expressed herein are solely those of the author, and do not in any way represent the views or opinions of any other person or entity.

: Showing Some Signs of Emerging Strength")