From all of the media outrage, Facebook posts and political theater one would think that the government shutdown in Washington is the next thing to the apocalypse.

Admittedly, it is embarrassing that our political leaders, if we can call them that, are unable to come together to keep the government open. But politics aside, what does the government shutdown really mean for the capital markets?

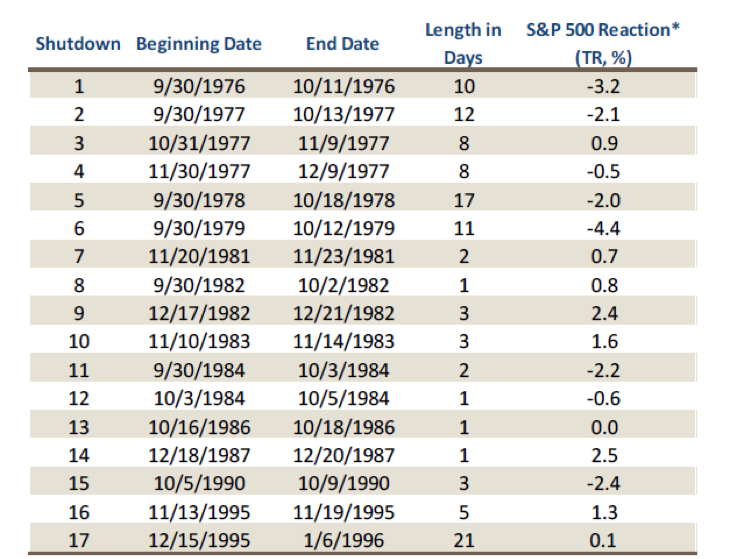

If history is any guide, not much. In fact, government shutdowns are not all that infrequent, with 17 of them occurring since 1976… with two bunched together over 1995-1996 for a total of 26 days. Judging by the Bloomberg chart below, government shutdowns may even be a positive for financial markets, as the S&P 500 has posted gains during the closure over half the time.

Source: Bloomberg – measures the S&P 500 performance from the market closing price one day prior to the shutdown until the end date of the shutdown.

But the question remains: What about a government shutdown could lead to higher equity prices?

First, the economic cost to government is relatively small at only $1.4 billion according to the Office of Management and Budget. This is a mere drop in the bucket of the $16 trillion dollar US economy. Second, shutdowns tend to end political deadlocks and allow for the re-pricing of political risk. So, while the shutdown is embarrassing it should have a modest impact if any on financial markets and potentially a positive effect if it takes a debt ceiling showdown off the table (a big “if” to watch). Be sure to also check out Andrew Kassen’s 1995-1996 government shutdown analysis.

Thanks for reading and try to enjoy the theater; there are some pretty good actors.

Additional Sources: US Trust Capital Market Outlook 9.30.2013 Twitter: @JoshuaSchroede2

Any opinions expressed herein are solely those of the author, and do not in any way represent the views or opinions of his employer or any other person or entity.

: Worrisome to Broader Market?")