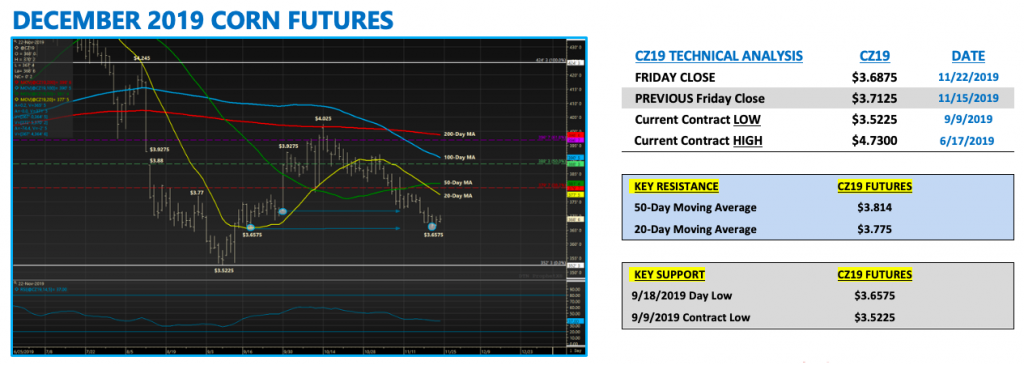

December corn futures closed Friday up a ¼-cent per bushel, finishing at $3.68 ¾.

Monday’s Weekly Crop Progress report showed the U.S. corn harvest reaching 76% complete as of November 17th, 2019, which compares to 89% a year ago and the 5-year average of 92%.

Several of the top corn producing states saw decent harvest progress with both Iowa and Minnesota hitting 77%, approximately 16% behind their 5-year averages.

Meanwhile Illinois and Indiana were reported at 80% harvested with Nebraska at 85%. The 4-states still showing considerable lags in their harvest progress were North Dakota (23%), South Dakota (53%), Wisconsin (44%), and Michigan (39%).

That said, NOAA’s latest 5 and 7-day precipitation models show the Western Corn Belt essentially dry now through November 29th, which should accelerate harvest gains specifically in the Dakota’s and Wisconsin. Comparatively the U.S. soybean harvest reached 91% on 11/17, equal to a year ago and just 4% behind the 5-year average.

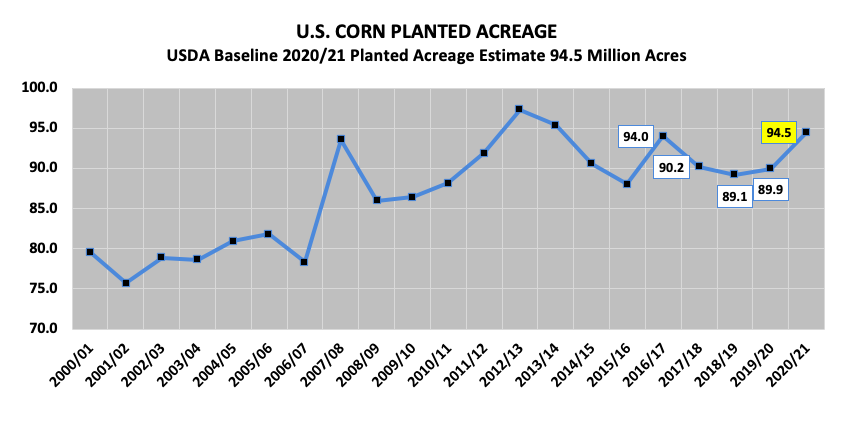

Here’s a look at overall planted acreage:

Wednesday’s EIA report showed U.S. ethanol production averaging 1.033 million barrels per day for the week ending November 15th, 2019.

This marked the 8th consecutive weekly production increase. Since establishing its lowest weekly run-rate since April 2016 back on September 20, 2019 of 943,000 barrels per day, the U.S. ethanol industry has recovered 90,000 barrels per day of production.

Clearly the availability of fresh corn supplies via the 2019 U.S. corn harvest coupled with economically advantaged corn basis levels has brought back a healthy percentage of the industry (relative to those plants that had momentarily shut-down or been running at less than full operating capacity due to an extended period of negative plant margins).

Furthermore despite the uptick in production, U.S. ethanol stocks have continued to drawdown, falling to 20.514 million barrels in this week’s report. This represented the lowest stocks figure since January 6th, 2017 (20.009 million barrels). This has resulted in ethanol prices staying firm in several markets, creating some of the best margins the industry has seen since September 2017.

The USDA’s “Baseline” U.S. corn S&D projections for 2020/21 (originally released on November 1st, 2019) have started to get more and more attention of late with the 2019/20 U.S. corn harvest now approaching 80% and the USDA’s November 2019 WASDE report somewhat of a distant memory.

That report revealed several very alarming (and concerning) trends for Corn Bulls moving forward. The first being the USDA’s Baseline 2020/21 U.S. corn planted acreage estimate of 94.5 million acres, which if realized would represent a 4.6 million acre increase from this past spring. This would also be the largest planted acreage figure since 2013/14 and the 3rd largest since 1945. The USDA then applied a U.S. corn yield of 178.5 bpa for total production of 15.545 billion bushels (both records).

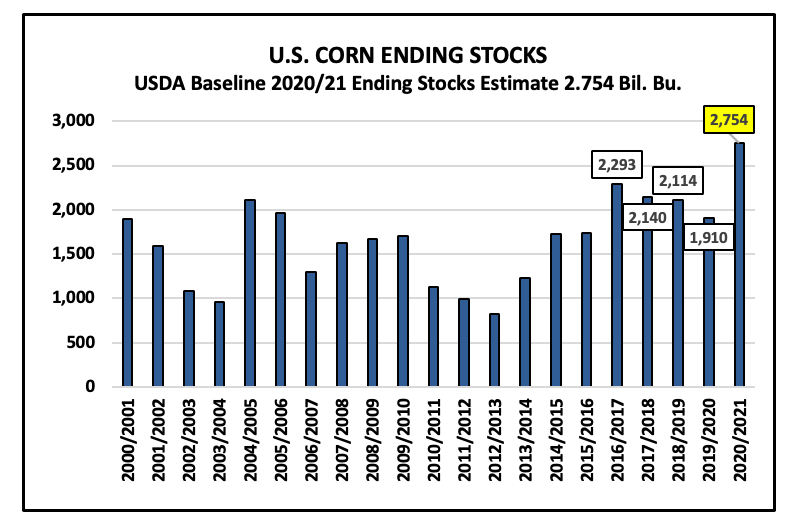

The result was that despite a projected 2020/21 U.S. corn demand increase of 830 million bushels, 2020/21 U.S. corn ending stocks would still exceed 2.7 billion bushels. This would be the largest U.S. corn carryout since 1987/88. Not surprisingly the USDA then estimated the average “farm price” for 2020/21 at just $3.40 per bushel.

Now obviously a lot can and will change regarding the narrative for the 2020/21 U.S. corn S&D as we actually get into calendar year 2020. That said what likely won’t change are the market’s current perceptions regrading 2020/21 U.S. corn acreage going up by at least 4 million acres, as well as, 2020/21 U.S. corn carryin stocks exceeding 1.85 billion bushels (even with some downward adjustment to 2019/20 U.S. corn production in the January 2020 WASDE report). Those two factors alone will make corn rallies difficult to sustain above $4.05 in December 2020 corn futures for the foreseeable future, while also providing a lower than preferred ceiling on rallies in the front-end (i.e. CH20 and CK20).

Corn futures closed slightly lower on the week with the market trying to find an intermediate bottom. The weekly day low of $3.65 ¾, a key area of price support, did hold early Wednesday morning; however there was no discernible price bounce to follow. Such is the state of the current corn market with just 3 trading days remaining prior to the Thanksgiving holiday. The Bearish storyline in corn largely remains unchanged:

- Even though Monday’s Crop Progress report indicated approximately 19.6 million corn acres were unharvested as of 11/17, traders seem largely unconcerned about potential production losses. Furthermore NOAA’s current forecast suggests substantial harvest gains should be made between now and the end of the month in the states that are lagging.

- Weekly export sales in corn of 31.0 million bushels, although an improvement from previous weeks, weren’t nearly enough to narrow the sales gap relative to a year ago. Crop year-to-date U.S. corn sales remain 45% behind 2018/19. Meanwhile, U.S. corn at the Gulf continues to trade at a premium to Brazilian offers even with CME futures substantially discounted.

- South American weather conditions remain ideal for both corn and soybeans in Brazil and Argentina. A fairly consistent pattern of precipitation is now in play through December 8th. In the USDA’s November WASDE report 2019/20 Brazil and Argentina corn production was estimated at a combined 151 MMT; down just 1 MMT from last year’s record total.

- Early 2020/21 U.S. corn planted acreage and ending stocks estimates suggest burdensome supplies await, which could dissuade Money Managers from accumulating a net long in corn futures until well into 2020. As it stands presently the Managed Money net short in corn continues to grow (recently estimated at -123,530 contracts as of the market closes on 11/19/19).

Overall, I expect more of the same in corn futures with narrow trading ranges and sideways to lower price action.

Twitter: @MarcusLudtke

Author hedges corn futures and may have a position at the time of publication. Any opinions expressed herein are solely those of the author, and do not in any way represent the views or opinions of any other person or entity.

")

Testing Important Price Support")