- Banks kicked off Q1 2026 earnings season yesterday with a rare Goldman Sachs front-run, with JPMorgan, Citigroup and Wells Fargo on deck for today.

- The S&P 500 is projected to deliver its sixth consecutive quarter of double-digit earnings growth at 12.6%, fueled largely by a powerhouse 45% expansion in the Information Technology sector.

- Following Constellation Brands’ lead, investors are bracing for more guidance withdrawals as corporations navigate a murky second-half outlook clouded by geopolitical tensions and volatile energy costs.

Financials in Focus: Big Banks Kick Off Q1 Earnings Season

In a rare plot twist, Goldman Sachs front-run the banking pack yesterday, marking the first time the firm has kicked off the earnings season ahead of JPMorgan Chase since 2018. The storied investment bank delivered notable results, comfortably surpassing analyst’s estimates on both the top and bottom-line.

While the firm achieved record revenues in its equities division, which surged 27% to $5.33 billion due to strong prime financing, FICC (fixed income, currencies & commodities) trading proved to be a relative weak point, falling 10% year-over-year as softer market-making conditions in interest rates and mortgages weighed on results.

Offsetting the trading volatility was a powerful rebound in investment banking, where fees jumped 48% to $2.84 billion on the back of a significant increase in completed M&A and debt underwriting activity. To account for wholesale loan impairments, the bank marginally increased its provision for credit losses to $315 million, reflecting a more cautious stance on the broader lending environment.

Looking ahead, CEO David Solomon emphasized the resilience of the firm’s “Capital Markets Flywheel,” noting that despite geopolitical headwinds, the bank is well-positioned to serve clients as the bull market matures and broadens into more cyclical sectors.1

Attention now shifts to the core banks to provide a broader look at the economy, with JPMorgan Chase, Wells Fargo, and Citigroup all reporting tomorrow before the bell. Similar to results seen from GS, analysts expect trading desks will likely see equities outperform FICC, as fixed-income volumes dampened following the recent ceasefire. Investors will also be eager to hear about consumer resilience, with particular interest in credit card delinquencies and increased loan loss provisions as a gauge of consumer health.

We will also be listening closely for commentary on the private credit market to see how these traditional giants are defending their territory against direct lenders in a newly competitive cycle. Ultimately, these results will tell us exactly what households and corporations are doing with their cash, regardless of what they say in sentiment surveys.

Source: Wall Street Horizon. Data as of April 10, 2026. Any equity marked with an asterisk is unconfirmed.

S&P 500 Eyes Sixth Quarter of Double-Digit EPS Growth

Currently, the S&P 500 is expected to show an EPS increase of 12.6% YoY, which would mark the sixth-straight quarter of double-digit (year-over-year) earnings growth reported by the index. Revenues are expected to have grown 9.8% YoY, which would mark the highest top-line growth rate since Q3 2022.

According to FactSet, nine of the 11 S&P sectors are anticipated to post YoY EPS gains, with Information Technology (45.0%), Materials (24.2%) and Financials (15.1%) leading the pack. Only Energy (-0.1%), Communication Services (-3.3%), and Health Care (-9.8%) are expected to post negative growth.2

Overall, 2026 EPS growth is expected to come in at 17.6%, and 9.0% for revenues.3

The “Wait-and-See” Playbook: Constellation Brands Withdraw Guidance, Will Others?

While the banking giants are busy preparing to report, a different trend could be emerging among consumer bellwethers: the sudden withdrawal of forward-looking guidance. Beverage giant Constellation Brands (STZ) set the tone last week by pulling its long-term outlook, a move that signals a growing “wait-and-see” approach to the K-shaped recovery.4

As more companies report, we will see if STZ is alone in this strategic silence. Recall during the Q1 2025 reporting season several companies across industries from airlines (Delta, Frontier) to autos (GM, Stellantis) chose to withdraw forward-looking guidance due to tariff uncertainty in the wake of Liberation Day.5 While reporting a Q1 2026 revenue record on April 8, Delta did not withdraw guidance but did issue a cautious Q2 outlook while it navigates fuel headwinds.6 As earnings season picks up we will be on the lookout for more guidance ghosting as the visibility for the second half of the year remains clouded in geopolitical fog.

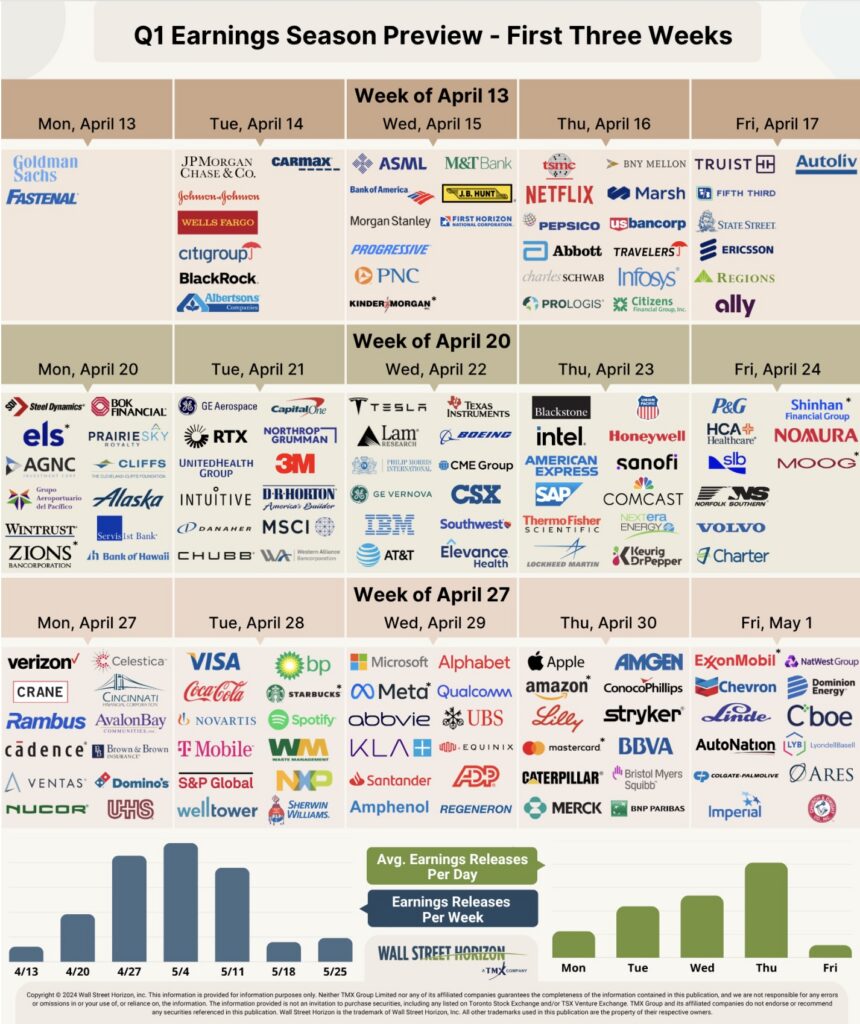

Q1 2026 Earnings Wave

The peak weeks of the Q1 earnings season are expected to fall between April 27 – May 15, with each week expected to see over 2,500 reports. Currently, May 7 is predicted to be the most active day with 1,167 companies anticipated to report. Thus far, only 48% of companies have confirmed their earnings date (out of our universe of 11,000+ global names). The remaining dates are estimated based on historical reporting data.

Sources:

1 Goldman Sachs First Quarter 2026 Earnings Results, April 13, 2026, https://www.goldmansachs.com

2 FactSet Earnings Insight, John Butters, April 10, 2026, https://advantage.factset.com

3 FactSet Earnings Insight, John Butters, April 10, 2026, https://advantage.factset.com

4 “Constellation Brands, U.S. maker of Modelo and Corona, withdraws 2028 guidance due to uncertainty,” CNBC, Laya Neelakandan, April 8, 2026, https://www.cnbc.com

5 “Companies withdraw guidance amid Trump’s tariffs,” Reuters, April 14, 2025, https://www.reuters.com

6 Delta Air Lines Announces March Quarter 2026 Financial Results, April 8, 2026, https://ir.delta.com

Twitter: @ChristineLShort

The author may hold positions in mentioned securities. Any opinions expressed herein are solely those of the author, and do not in any way represent the views or opinions of any other person or entity.

Testing Important Price Support")

: Cup (and Maybe Handle) Watch")