- The Q1 reporting season is off to a solid start, but investors must also eye macro data points ahead

- Record-high stock prices come as consumers have never felt worse—which trend will break first?

- In this week’s macro roundup, we profile the major economic releases that will buttress the slew of crucial earnings updates in the next three weeks

Stocks pace for one of their best April performances on record. The 9% S&P 500 Index (INDEXSP: .INX) pullback from January through the March 30 intraday low may feel like a distant memory for investors. Still, geopolitical risks remain, and macro unease leaves many pundits doubting the rally’s durability. Is a pause in order? Or are we off to the races like we were a year ago?

Earnings Beat Rates Signal Underlying Corporate Strength

The answer may lie in key earnings reports over the next few weeks, along with a trove of macro data points that will set the stage for the summer. On the former front, BofA noted that a solid 76% of S&P 500 companies that have already reported topped Wall Street earnings estimates. That’s above the typical 68% Week 1 beat rate. Heavy hitters from the Mag 7 kick off the heart of the reporting period—Tesla (TSLA) is on for tonight.

We’ll be all over the revenue and income data, as well as crucial guidance numbers as they roll in. It’s also important to keep an eye on the macro situation at home and abroad. Of course, the conflict in Iran is A-1 material, but incoming March and April economic updates may soon garner increasing attention. Let’s double-click on that situation to help frame both the earnings backdrop and a busy corporate event season already in full swing.

Data on Tap, And Why They Matter

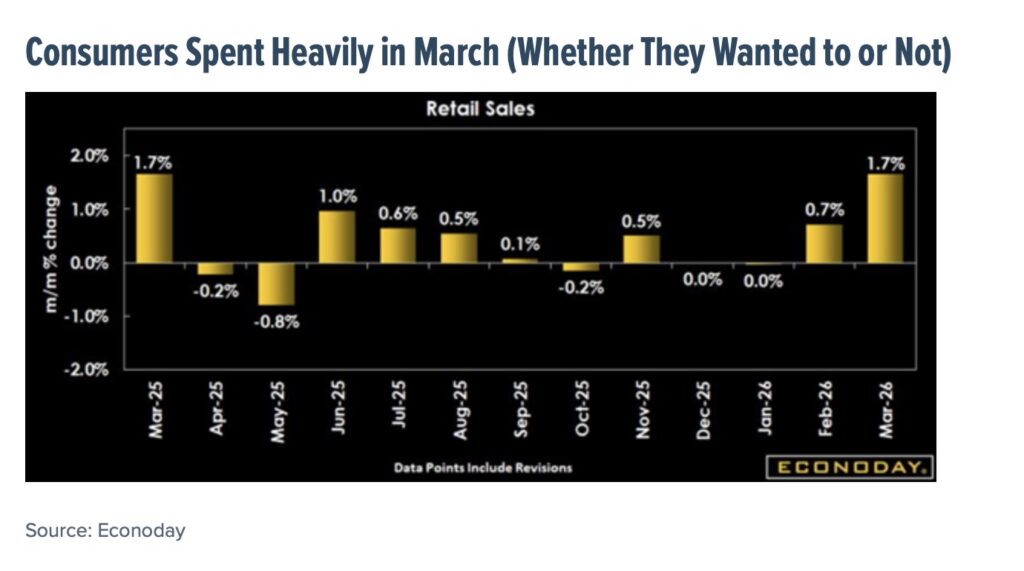

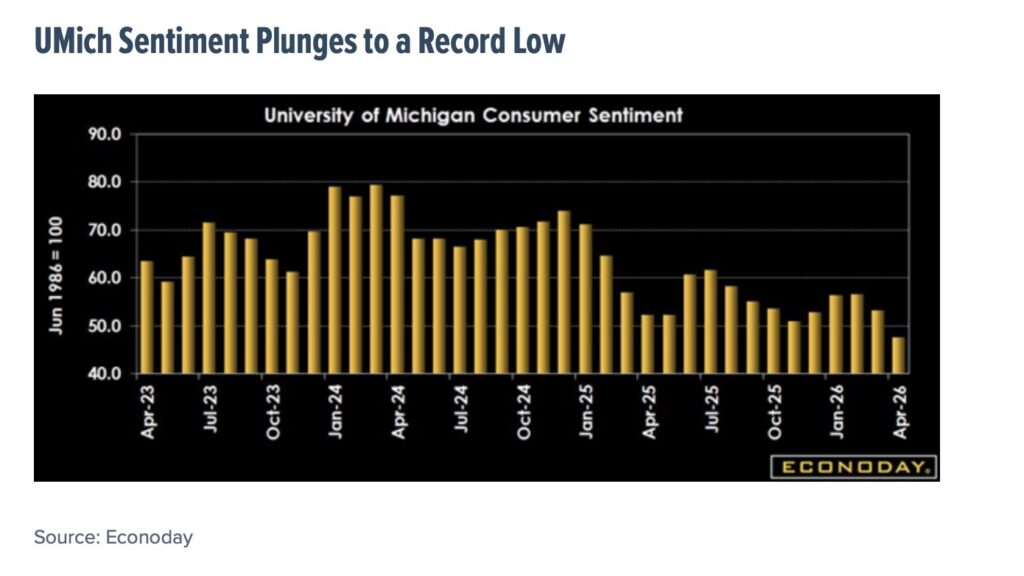

Following Tuesday’s March Retail Sales report, Thursday’s set of S&P Global Flash PMIs will be the timeliest vibe check yet. These Purchasing Manager Index readings are for this month and follow a record-setting (in a bad way) April preliminary reading from the University of Michigan Surveys of Consumers. Its sentiment gauge was the worst on record.

That’s saying something, as “UMich” dates back to the middle of the last century. The eye-popping report made for the most K-shaped of all macro stats: the S&P 500 hit a record high as consumer sentiment sat at a record low (but at least they are still going to the movies!).

Consumers Spent Heavily in March (Whether They Wanted to or Not)

UMich Sentiment Plunges to a Record Low

For it to be official, Friday’s UMich survey reading must confirm the preliminary poll from April 10. Given some optimism about a ceasefire deal between the U.S. and Iran (and the potential reopening of the Strait of Hormuz), households’ financial angst could ease.

April Data Offer Post-War Clues

To be clear, PMIs and consumer sentiment are “soft” data. They are not “hard” data, such as Retail Sales. Additional hard data hits next Tuesday morning, right before major tech companies post Q1 earnings.

Two timely data points that point to a still-decent macro backdrop are the ADP Employment Change Weekly and the Johnson Redbook Retail Sales. ADP’s weekly job change gauge tallied its best level over its brief history (since September 2025) earlier this month, while the weekly consumer spending pulse suggests a steady 7% YoY consumption trend. Not bad.

Marrying the Macro & Micro

Those are unofficial barometers, but along with updates from management teams at industry conferences and Annual General Meetings, they may help portfolio managers piece together a macro and micro mosaic. Later in the session on Tuesday, April 28, comes The Conference Board’s Consumer Confidence survey.

For background, UMich tends to reflect inflation perceptions, while The Conference Board’s questionnaire leans more on the labor market outlook. With a generally steady jobless rate and real wage growth now near the flat line, it’s difficult to be all that rosy about the April report’s possible findings.

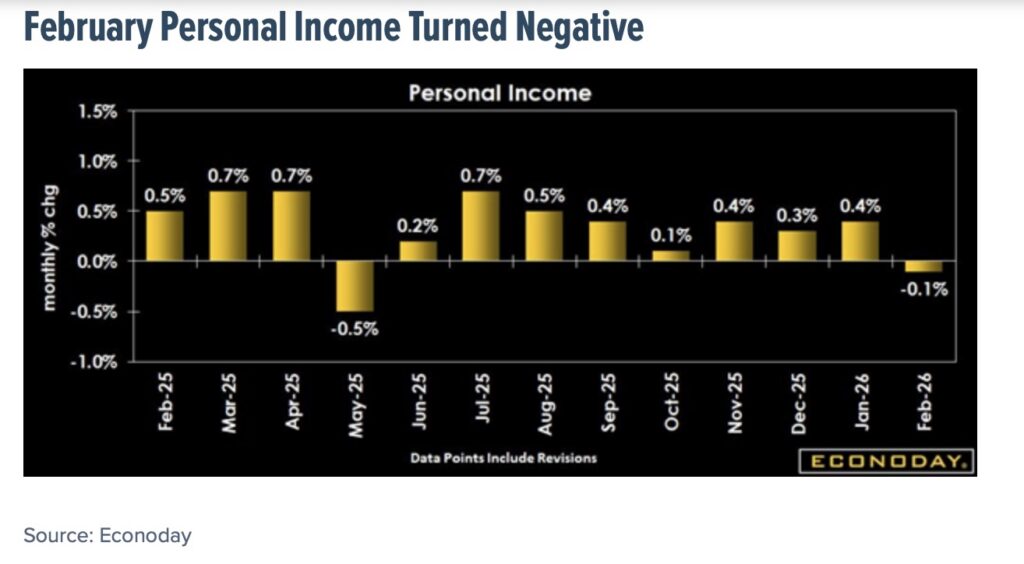

February Personal Income Turned Negative

The Fed Meets Again. Powell’s Last Stand? Warsh Warming Up.

From there, the Fed meets mid-week and announces its April policy decision next Wednesday afternoon. No rate change is expected. What’s more, this is not a “dot plot” meeting, so fireworks should be few.

FOMC drama centers not so much on Chair Powell right now as on his presumptive successor, Kevin Warsh. The former voting member began his confirmation hearing before the Senate Banking Committee yesterday. While confirmation hearings for Federal Reserve chairs are usually staid events, this one has been a bit more lively, shall we say.

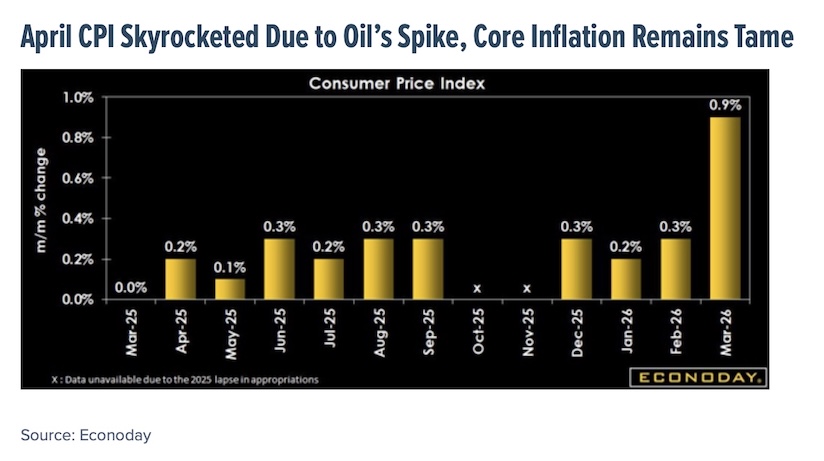

Next Thursday brings another inflation update, this time the PCE Price Index for March. If it feels like we are getting one major macro data point after another, you’re not crazy. Data from last year’s government shutdown is just now getting back on a regular schedule. A soft March PCE print may help tee up a possible Fed rate cut later this year.

Recall that the market-implied odds of an ease were nixed as oil soared above $100 per barrel last month. But as energy prices ebb, rate-cut probabilities have ticked back up.

April CPI Skyrocketed Due to Oil’s Spike, Core Inflation Remains Tame

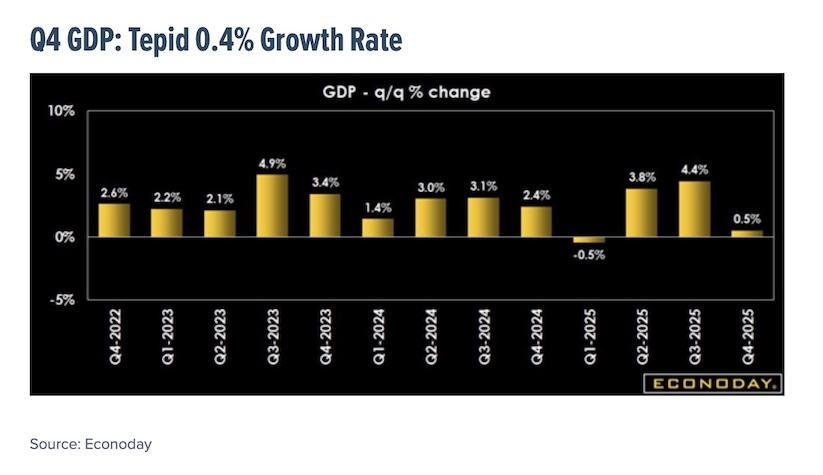

From there, the first Friday of May brings a first look at Q1 GDP. This will follow a weak third update to the Q4 economic growth report, so it may carry added market influence.

Q4 GDP: Tepid 0.4% Growth Rate

April Employment & Berkshire Without Buffett In Charge

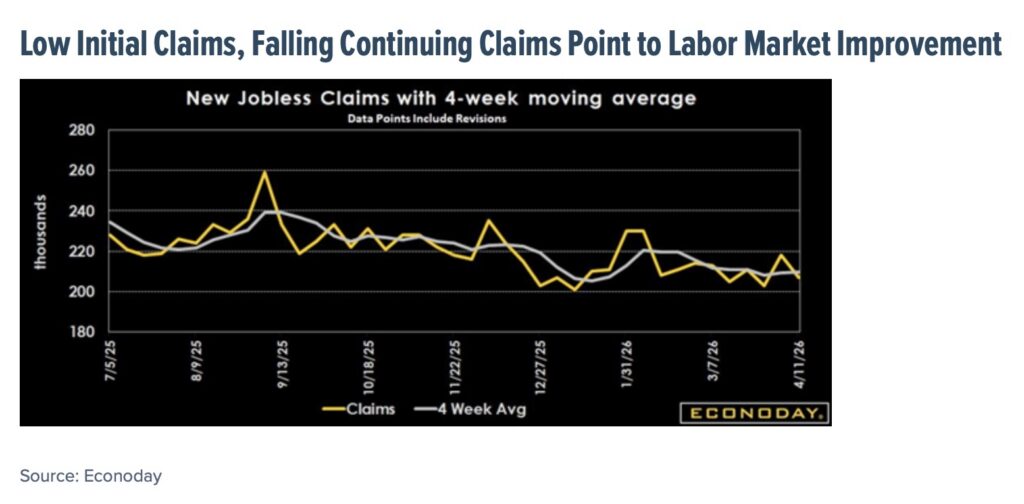

After that, it’ll be all about the labor market. The official April jobs report arrives on May 8, which follows “Woodstock for Capitalists” on May 2 (Berkshire Hathaway’s (BRK.A) annual shareholder meeting in Omaha, Nebraska).

Low Initial Claims, Falling Continuing Claims Point to Labor Market Improvement

The Bottom Line

It’s a busy macro stretch as company earnings reports come in fast and furious. A focus on real data and earnings may be a welcome development for investors wary of geopolitical headlines. The team at Wall Street Horizon will keep you up to speed with the latest trends, and you can access our industry-leading forward-looking corporate event data to stay ahead of markets.

Twitter: @ChristineLShort

The author may hold positions in mentioned securities. Any opinions expressed herein are solely those of the author, and do not in any way represent the views or opinions of any other person or entity.

")

Trading Near Top Of Price Range")