I want to take a few minutes to update you on my thoughts regarding the domestic and global economy, the Federal Reserve, and the current state of U.S. treasury bonds as an investment.

After several additional hours of research and analysis, I believe the difficulties in our global economy are the direct result of the world’s Central Bankers following a misguided philosophy that threatens even worse pain ahead. Their actions may have saved the global economy back in 2008, but the remedy has only kept the patient on life support.

The global economy continues to slow down and there is little hope on the horizon of reversing what’s already in motion.

The Federal Reserve ‘surprised’ the markets at the end of October when they said that an increase in interest rates at the December meeting was a ‘live’ possibility. And interest rates futures show traders believe there is a 72% probability of that occurring. Keep in mind that this is the same scenario that has played out over the last year where the Fed continues to talk up a rate increase at the next meeting while saying they are data dependent. Then when it comes time to pull the trigger on the rate increase they don’t. Will this time be different?

There isn’t any way to know.

I have been very vocal about global growth slowing and the likelihood that the United States will enter a recession some time in 2016. If the Federal Reserve does raise interest rates at the December meeting, my viewpoint is that it will pull forward the beginning of a recession. Keep in mind that the main problem with the US economy is that the Federal Reserve has ALREADY been raising interest rates. Every time they talk about raising rates at the next meeting, the markets go ahead and adjust.

The whole purpose of raising interest rates is to ‘put the brakes on the US economy’ and slow it down so that it doesn’t over heat. On the other hand, they lower interest rates in order to ‘give the economy some gas’ to cause it to grow. So the GDP shows that the US economy continues to slow year over year. Does it feel to you like we need the Fed to put on the brakes?

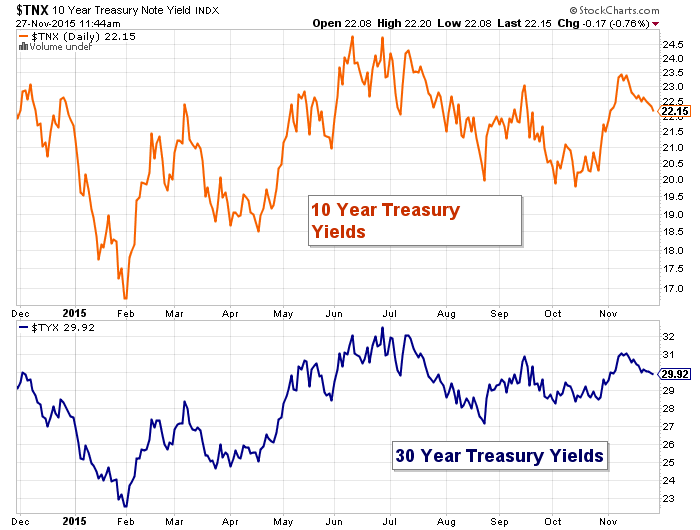

In the end, it doesn’t matter what I think should be done, it matters how I manage the risk of what is done. And the risk (in the short-term) is that the Federal Reserve raises interest rates at the December meeting. If they raise rates in December that could result in the value of various US Treasury bonds positions going down. As we saw last month, the value of the bonds immediately went down when the Fed announced the ‘live’ possibility of a December rate increase.

Since then the yields on longer bonds have been drifting back down while the yields on shorter-term US treasury bonds have been rising.

In other words, the slope of the yield curve has been flattening. My analysis of that is that traders think that even if they raise interest rates at the December meeting that it will result in lower longer-term yields down the road because of slowing global growth and a slower global economy.

That’s why we haven’t seen treasury yields spike as high as they did back in June when there was the ‘likelihood’ of them raising rates then.

So here are the options the Federal Reserve has and how I see them playing out:

- The Fed decides not to raise rates again. This should cause longer term yields on US treasury bonds to drop, helping bond positions.

- The Federal Reserve raises rates but signals that it will be (patient or some other word that means they don’t expect to raise at the next meeting). This could cause short-term treasury yields to go up while longer-term treasury yields could stay the same or drift down. That would hurt our shorter-term bond positions and be neutral or good for our longer-term bond positions.

- The Fed raises rates and hints that they may raise rates again at the next meeting. This would be bad for both short and long-term US treasury bonds.

(Regarding stocks: I don’t see how an interest rate rise is positive for stocks. There may be an initial rally but I don’t expect it to last.)

Lastly, I believe that we may see a significant stock market correction in the next 6 to 12 months. So I am avoiding stocks at this time. And US treasury bonds are one of the few places that I believe provide protection (and possible growth) in a deflationary environment; and they should increase in value if stocks stagnate or head lower again. My intermediate-term view has not changed, but in the short-term I may be reducing exposure to US treasury bonds to minimize the event risk associated with the Fed’s decision. By taking some money off the table and selling some bonds now, it provides me the opportunity to buy them back should yields initially spike around the Fed decision.

Thanks for reading and have a great weekend.

Further reading from Jeff: Is It Time To Reduce Your Stock Market Exposure?

Twitter: @JeffVoudrie

Author holds various long positions in US treasury bonds at the time of publication. Any opinions expressed herein are solely those of the author, and do not in any way represent the views or opinions of any other person or entity.