Many political pundits will tell you that President Trump won the election, in part, on the promise of a rebirth in the manufacturing sector. His initial strategy to reduce the trade deficit centers on negotiating new tariffs and renegotiating existing trade agreements.

These volatile discussions with other nations, often accompanied by threats, will likely continue and the outcomes are far from certain.

If the President is unable to satisfactorily adjust the trade terms with our partners, he could resort to a weak U.S. Dollar policy that has frequently been employed throughout modern history. As a current point of reference, the Chinese Yuan has weakened by about 5% over the last two months. This is likely an effort to reduce the effect of new tariffs.

The U.S. Dollar is the world’s reserve currency and is used in a majority of global trade. The value of the dollar versus the currency of other nations is a primary variable that drives the prices of goods traded amongst nations. When oil, copper, corn and most other commodities are traded between nations they are typically quoted in units per dollar. In addition to analyzing the supply and demand dynamics for a specific commodity, investors in the commodity sector should also assess the value of the dollar.

In this article, we focus on the correlations of numerous commodities to the dollar. Understanding these relationships will prove helpful if a weak dollar policy is utilized by the administration.

For a more thorough perspective on the dollar and the forces that help drive its direction, please read Our Two Cents on the Dollar.

Dollar/Commodity Correlations

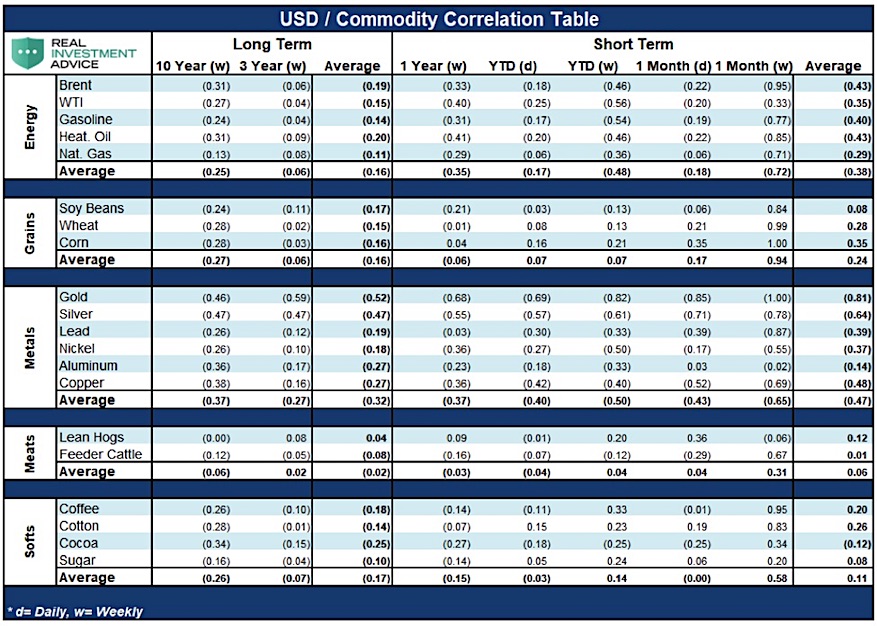

The table below depicts the correlation between various commodities and the U.S. dollar.

Data Courtesy Bloomberg

In the table above, the correlation between each commodity and the U.S. dollar index is aggregated by commodity sector and time frame. In organizing the table this way, we can ascertain which specific commodities and/or sectors have strong or weak correlations to the dollar. This may present useful investment or hedging strategies in the event the U.S. dollar weakens in the future.

A correlation of +/- 1.00 implies a perfect relationship between changes in the price of the commodity and the value of the dollar. As shown above, almost all of the short and long-term correlations have a negative sign indicating an inverse relationship. For most commodities, the price falls when the dollar is strengthening and rises when the dollar is weakening. Statisticians consider a correlation of +/-0.70 to be significant, but anything over +/-0.35 denotes a statistically meaningful relationship. While none of the commodities have a longer-term correlation above +/- 0.70, here are some important observations:

- Precious metals (gold and silver) have shown a durable negative correlation (-0.52 and -0.47 respectively) to the dollar over the long term. In the short run, the correlation for gold has been statistically significant. As John Pierpont Morgan once said, “gold is money,” and somewhat true to his wisdom that gold is in itself a currency, it is not surprising that gold has the strongest correlation to the dollar of all the commodities shown.

- While the industrial metals tend to have a low correlation with the dollar over the long run, nickel and copper, in particular, have recently demonstrated a higher negative correlation to the dollar than their long-term trends. The price of these metals typically correlates well with global economic activity. As we have seen for the last month, a strong dollar tends to dampen foreign economic activity.

- The energy sector also has a strong negative correlation over the last year to the dollar. The relationship is even more pronounced over the last month. Interestingly, the price of Brent and Crude oil (WTI) have diverged from their typical correlation to each other. We suspect this short-term divergence will revert to the normal relationship over the coming year.

- Grains and soft commodities tend to have a slight negative correlation over longer periods but have bucked that trend recently with slightly positive correlations to the dollar.

- Lean hogs and feeder cattle appear to have little correlation to the dollar over the short and long-term.

Summary

Trump’s campaign promised fair trade and a resurgence in U.S. manufacturing. While there are many ways he may accomplish this task, the most expeditious would be a weak dollar policy. As we have seen, negotiations can be tricky, complex and time-consuming. With a mid-term election in a few months and the 2020 presidential campaign commencing shortly thereafter, the President’s patience may wear thin. If Trump were to effectively implement a weak dollar policy, the benefits he promised voters are more likely to be apparent, even if they are only cosmetic. Investors can prepare for currency depreciation, which is frequently the expedient and often the preferred tactic of politicians.

As anticipated, gold is the best hedge against a weaker dollar. The negative correlation between gold and the dollar should not be surprising given gold’s history as a currency itself. Pronounced dollar weakness, especially weakness prompted by an acknowledged policy targeting it, would most likely result in rising gold prices. Silver also plays a role as a store of value, but silver, unlike gold, has many industrial uses which tend to reduce its correlation to the dollar. The energy sector may also provide a good hedge to dollar weakness, but if that weakness is accompanied by declining economic activity, the reduced demand for energy could overwhelm the benefits it provides as a dollar hedge. Grains, meats, and other soft commodities tend to be even less of a dollar hedge. Supply and demand dynamics, frequently including hard to predict weather patterns, play a larger role in their pricing than other commodities.

Investors may be tempted to buy ETF’s that focus on a broad grouping of commodities as a dollar hedge. Although important in its influence over commodities, the U.S. dollar is but one of many factors that drive prices. The multitude of dynamics that determine commodity prices means there are no quick and easy answers to determining an effective hedge in the event of a weakening dollar. Awareness of these relationships and the extent to which they are aligned with or diverging from long-term trends is, however, a powerful analytical tool in the rigor of determining an optimal strategy.

Twitter: @michaellebowitz

Any opinions expressed herein are solely those of the author, and do not in any way represent the views or opinions of any other person or entity.

Testing Important Price Support")

: Cup (and Maybe Handle) Watch")