From a 2013 Bloomberg article:

It’s been 22 years since annual inflation in Japan exceeded 2 percent, according to data compiled by Bloomberg. In the last five years of the 1980s, when Japan’s gross domestic product climbed from $1.3 trillion to $3 trillion and the Nikkei 225 Stock Average peaked at almost 39,000, the monthly readings for consumer price gains averaged 1.2 percent, the data show. The Nikkei 225 closed today at 15,407.94. “It’s difficult to say whether we are really exiting deflation,” Mitani said. “Consumer prices are starting to rise, but a large reason for that is based on the weakening yen and rising energy prices. We can’t say that looking at recent results, we have really exited deflation.”

Investment Implications: Artificially High Prices Until Inflation Picks Up

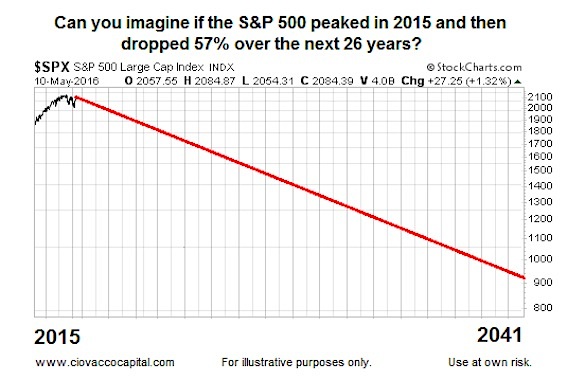

To put some human context around the problems associated with a deflationary spiral, assume you retired in 2015 at age 55. Hypothetically, if the S&P 500 peaked in 2015, similar to the Japanese stock market in 1989, 26 years later you would be 81 years old and the year would be 2041. If you invested $500,000 of your retirement portfolio in the S&P 500 in 2015, it would be worth about $215,000 when you celebrate your 81st birthday in 2041.

The human, social, and political ramifications of such a prolonged deflationary spiral are difficult to imagine. Therefore, given that global central banks may be nearing the end eof the traditional “inflate to create the wealth effect” road, it would not be surprising to see even more radical policies in the future, including additional forms of asset purchases (QE) in the United States.

As noted in a May 2016 video, the Fed’s dual mandate, and more importantly basic economic principles, tell us central banks will try to inflate as long as they possibly can. When inflation starts to become a problem on the high end of the price stability spectrum, it will be much harder for central banks to keep things propped up. Therefore, investors must be open to:

- A continuation of extremely dovish and radical policies from global central banks (see article on possible expansion of stock purchases).

- The possibility of asset prices remaining artificially elevated, including the possibility of U.S. markets pushing to new all-time highs.

In his May investment outlook, Bill Gross of Janus Funds summarized the situation this way:

Private banks can fail but a central bank that can print money acceptable to global commerce cannot. I have long argued that this is a Ponzi scheme and it is, yet we are approaching a point of no return with negative interest rates and QE purchases of corporate bonds and stock. Still, I believe that for now central banks will print more helicopter money via QE (perhaps even the U.S. in a year or so) and reluctantly accept their increasingly dependent role in fiscal policy. Investment implications: Prepare for renewed QE from the Fed. Interest rates will stay low for longer, asset prices will continue to be artificially high. At some point, monetary policy will create inflation and markets will be at risk. Not yet, but be careful in the interim.

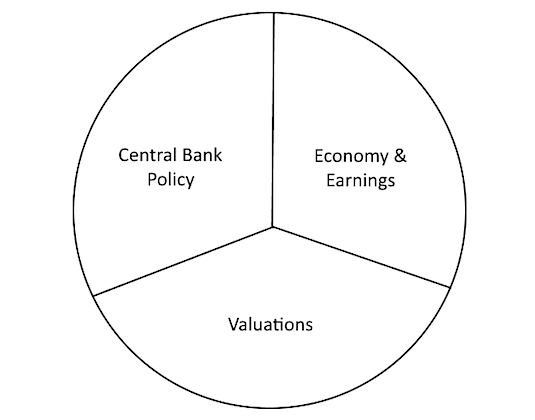

Tactical Approach Until Fundamentals Overtake Central Banks

There are two main issues that could overtake central bank policies; one we have mentioned, inflation; the other is economic fundamentals. As noted in this video clip, easy-money policies were being implemented by the Fed during both the dot-com bust recession/bear market and 2007-2009 financial crisis, and yet asset prices continued to fall due to overwhelming fundamental issues. The role of inflation in terms of limiting central bank easy-money actions was outlined on May 2.

Data And Charts Can Assist With Bull/Bear Tipping Point

When financial markets determine that rising inflation/weak fundamentals are more important than central bank policies, it will be reflected in all the hard data tracked by our market model. Conversely, if asset-price friendly policies from central banks take precedence over fundamental concerns, it will show up in numerous ways in the hard data, including the possibility of seeing U.S. stocks push to new all-time highs. The data and charts can help us stay more tactical until a clearer long-term trend begins to emerge, as we described on May 6.

Fed Will Take Whatever Means Necessary

If you have trouble with the concept of asset prices pushing higher given numerous fundamental concerns (earnings, margins, productivity, valuations, etc.), keep in mind that in a 2002 speech Deflation: Making Sure “It” Doesn’t Happen Here Ben Bernanke reminded us that the Fed would take whatever means necessary to prevent significant deflation in the United States. The Bank Of Japan and European Central Bank have already moved into “whatever means necessary” territory; the Federal Reserve may not be far behind. The relevant blurb from Bernanke’s speech:

The second bulwark against deflation in the United States, and the one that will be the focus of my remarks today, is the Federal Reserve System itself. The Congress has given the Fed the responsibility of preserving price stability (among other objectives), which most definitely implies avoiding deflation as well as inflation. I am confident that the Fed would take whatever means necessary to prevent significant deflation in the United States and, moreover, that the U.S. central bank, in cooperation with other parts of the government as needed, has sufficient policy instruments to ensure that any deflation that might occur would be both mild and brief.

Thanks for reading.

Twitter: @CiovaccoCapital

Author or his funds have long positions in related securities. Any opinions expressed herein are solely those of the author, and do not in any way represent the views or opinions of any other person or entity.