After months of jawboning and telegraphing the pending move, the world’s largest central bank finally raised rates.

On March 16, the Federal Reserve raised the Fed Funds Rate from the emergency low of 0.25% to 0.50%, marking the first change in rates since cutting rates to rock-bottom levels in response to the pandemic’s onset in March 2020. This rate hike follows moves by other central banks, including the Bank of Canada and Bank of England, to tighten monetary policy.

One could argue (and many do) that the Fed and other central banks are already behind the curve, given the global economy is growing at about 4%, unemployment is back down to near pre-pandemic levels, and inflation is, well, inflating. Some argue the opposite as well. But knowing whether the banks are behind, just in time or ahead of the curve requires the passage of time. Monetary policy has a broad-based effect on the economy and asset prices, and knowing the effects of changes takes time, making policy decisions very challenging.

How bond markets might react to the rate hike

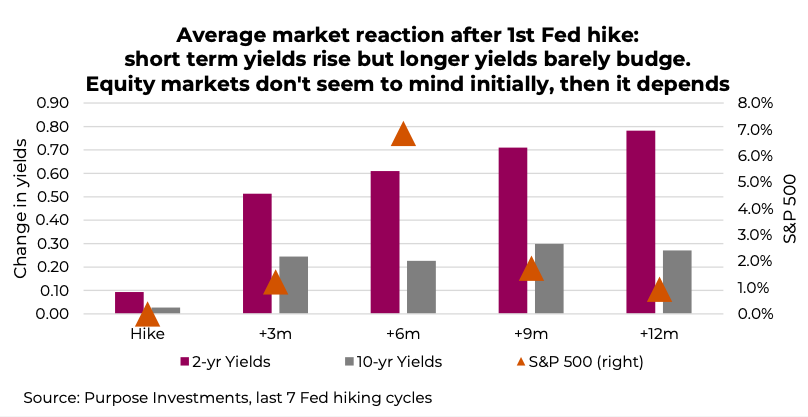

If history is any indication, the onset of rate hikes is largely a non-event. Looking back at the last seven Fed rate tightening periods, markets don’t seem to care all that much. Short yields, measured by the two-year Treasury, anticipate and rise in the early months. That is not surprising given the two-year is more influenced by the overnight rate.

More interesting, is that longer yields such, as the 10-year, rise a little after the first-rate hike, but not by much. Intuitively, this makes sense. The bond market has lots of smart participants and reacts much more quickly to economic data than the Fed’s official policy changes. Or more simply, the bond market usually knows rate hikes are coming and moves up (yield up, price down) in anticipation. Given that 10-year yields in the U.S. and Canada have risen from 0.7% in mid-2020 to 2.2% today, it’s pretty clear bonds knew this was coming.

The impact of rate hikes on equity markets

Using the S&P 500 as proxy, equity markets don’t seem to mind the Fed embarking on a rate hiking cycle. On average, markets tend to be a bit more volatile for the first few months or so, but then move higher. One reason for this is that the Fed raises rates because the economy is doing well enough to stand on its own. Given that backdrop, the equity market tends to enjoy the lift from a good economy more than the drag effect from higher short-term rates. Looking out nine or 12 months, the picture is more clouded. If the risk of a recession mounts, the equity market does not fare as well.

Admittedly, these are averages over seven occurrences during the past 40 years, so far from a hard rule. We should also consider the market’s behavior heading into the onset of a rate hiking period. This tightening cycle has already seen bond yields rise over the past 18 months. We have also seen equity markets enjoy strong gains since Q1 2020, followed by a corrective phase so far in 2022.

Rate hikes in an era of inflation

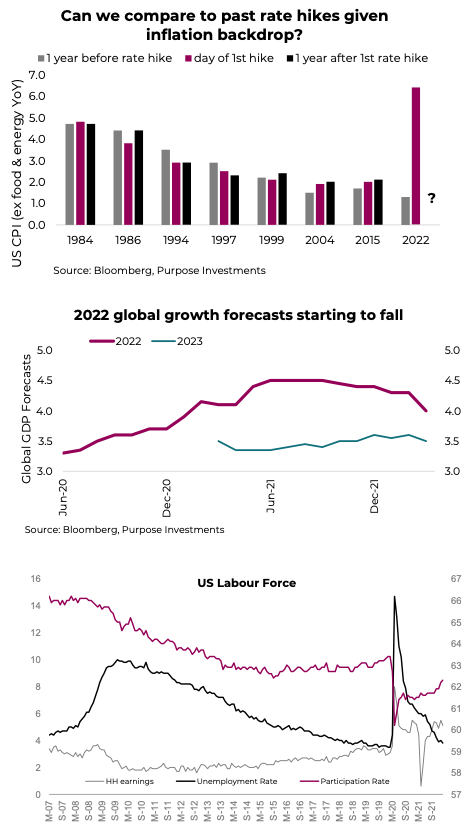

The biggest unique variable for this rate hiking cycle is inflation. The last three hiking cycles were during periods of low and benign inflation — a considerable contrast with today. Rate hikes won’t address the supply chain issues still resonating from the pandemic nor the commodity spikes from the invasion of the Ukraine. Still, the inflation picture would become better if economic growth cooled faster, which rate hikes can help. Furthermore, given the inflation environment, we could be in for a more aggressive tightening cycle than recent experiences. The lone dissenter among the Fed Open Market Committee wanted to double this week’s hike, and sees as many as 12 hikes this year, as opposed to previous cycles where the dissenters tended to be dovish (i.e., they were opposed to raising rates).

Given the spike in commodity prices at the end of February and into March, inflation may well remain elevated longer than most expect. What will become just as topical in the coming months is the pace of economic growth deceleration. Slowing growth is pretty much ordained after the global economy rebounded by about 5.8% in 2021. Currently, consensus has this normalizing down to 4.0% in 2022 and the big question will be “does 14 this come down faster?” We have already seen forecasts for 2022 cut to 4.0% from 4.5, and safe to say not all forecasts have been adjusted following the onset of war and sanctions.

Since the Fed’s mandate is growth, inflation and employment, the last factor to mention is jobs. Unemployment rates have come back down to pre-pandemic levels, but with many dropping out, the labor force participation has only partially recovered. Wages have been rising at their fastest pace in decades, which will likely perpetuate some of the inflation we are seeing. People with rising incomes can afford higher prices, making inflation self-perpetuating. Will this draw more people into the labor force and tame wage inflation? Absolutely. Will it factor into the Fed rate path? Assuredly it will.

Investment implications

The global monetary tightening cycle has begun and will likely be with us for a while. It is about time. The current economic environment does not beget a zero-rate policy and leaving it this low for so long has at least partially contributed to the inflationary problem we are in today.

Trying to draw similarities with this hiking cycle and previous episodes is challenging given the high inflation environment and low labour force participation today. Furthermore, most past hiking cycles occurred during periods of accelerating economic growth, while we are currently experiencing decelerating economic growth.

The good news is the economy is decelerating from a high level, which means a few rate hikes are likely not going to move the needle very much. Still the pace of decelerating growth is key, and we are already starting to hear some banter about the ’R’ word. We think this is premature given the current economic growth pace; instead, we are likely entering a few quarters of debate about a ‘hard’ or ‘soft’ landing. You will start hearing “recession” thrown about the financial media this year though.

This has us continuing to favor value over growth. Along the same lines, we still favour a shorter duration stance. However, given drawdowns in some growth names, we are curious if any have jumped into the value camp, and similarly, we are seeing some opportunities on the beaten down credit sector.

Short-term thought

Markets have been rebounding this week and the correction may have run its course. We don’t have a scientific reason to say this other than the news continues to be negative. Ukraine conflict continues to devolve, the Fed hiked and based on comments plans to keep hiking for a long time, inflation prints were elevated, etc. The news has not been good. When bad news fails to move markets lower, the path of least resistance is likely up.

Source: Charts are sourced to Bloomberg L.P., Purpose Investments Inc., and Richardson Wealth unless otherwise noted.

Twitter: @ConnectedWealth

Any opinions expressed herein are solely those of the authors, and do not in any way represent the views or opinions of any other person or entity.