The New England Patriots are the winningest professional football team of the new millennia. While we could post a long list of reasons for their success, there is one that stands above the rest. In a recent interview, Patriots quarterback Tom Brady stated that they start each year with one goal; win the Super Bowl.

Unlike many other teams, the Patriots do not settle for a better record than last year or improved statistics. Their single-minded goal is absolute and crystal clear to everyone on the team. It provides a framework and benchmark to help them coach, manage and play for success.

Interestingly, when most individuals, and many institutions for that matter, think about their investment goals, they have hopes of achieving Super Bowl like returns. Despite their well-intentioned ambitions, they manage their portfolios based on investment benchmarks that are not relevant to their goals. In this paper, we introduce a simple investment benchmark that simplifies the tracking process toward goals which if achieved, provide certitude that one’s long-term objectives will be met.

The S&P 500

Almost all investors benchmark their returns, manage their assets and ultimately measure their success based on the value of a stock, bond or blended index(s). The most common investor benchmark is the S&P 500, a measure of the return of 500 large-cap domestic stocks.

Our belief is that the performance of the S&P 500 and your retirement goals are unrelated. The typical counter-argument claims that the S&P 500 tends to be well correlated with economic growth and is a valid investment benchmark for individual portfolio performance and wealth. While that theory can be easily challenged over the past decade the question remains: Is economic growth a more valid benchmark than achieving a desired retirement goal? Additionally, there are long periods like today where the divergence between stock prices and underlying economic fundamentals are grossly askew. These variances result in long periods when stock market performance can vary greatly from economic activity.

Even if we have a very long investment time frame and are willing to ignore the large variances between price and valuation, there is a much bigger problem to examine. Consider the following question: If you are promised a consistent annualized return of 10% from today until your retirement, will that allow you to meet your retirement goals?

Inflation and Purchasing Power

Regardless of your answer, we are willing to bet that most people perform a similar analysis. Compound current wealth by 10% annually to arrive at a future portfolio value and then determine if that is enough for the retirement need in mind. Simple enough, but this calculus fails to consider an issue of vital importance. What if inflation were to run at an 11% annual rate from today until your retirement date? Your portfolio value will have increased nicely by retirement, but your wealth in real terms, measured by your purchasing power, will be less than it is today. Now, suppose you were offered annual returns equal to the annual rate of inflation (the consumer price index or CPI) plus 3%.

Based on 2017 CPI of approximately 2% for a total return of approximately 5% compared to almost 20% for the S&P 500, we venture to say that many readers would be reluctant to accept such an “unsexy” proposition. Whether a premium of 3% is the right number for you is up for debate, but what is not debatable is that a return based on inflation, regardless of the performance of popular indexes, is a much more effective determinant of future wealth and purchasing power.

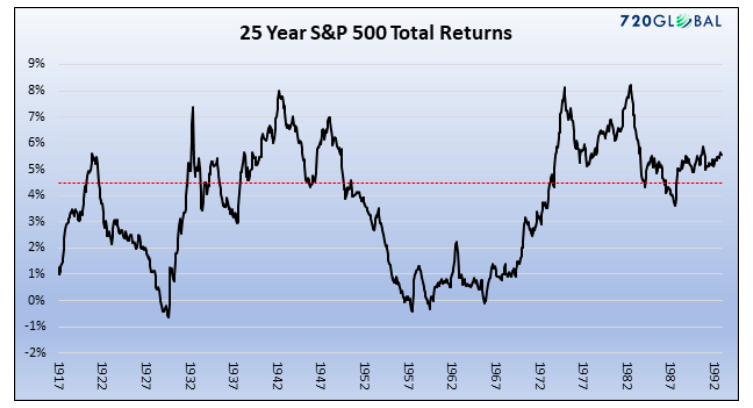

To show why this concept is so important, consider the situation of an investor with plans to retire in 25 years. Our investor has $600,000 to invest and believes that he will need $1,500,000 based on today’s purchasing power, to allow him to live comfortably for the remainder of his life. To achieve this goal, he must seek an annualized return of at least 4.50%. As a point of reference, the total return of the S&P 500 is 6.60% over the past 100 years. At first blush our investor, given his relatively long time frame until retirement, might think the odds are good that the S&P 500 will allow him to achieve his retirement goal. However, his failure to factor in inflation causes his calculations to be incorrect. Since 1917, inflation has averaged 3.09%. The S&P 500 total return since 1917 including the effect of inflation is only 3.51%. The odds are not in his favor, and his oversight may ultimately leave him in a difficult situation.

The graph below shows the resulting 25 year total returns based on each monthly starting point since 1917. The red line shows our investor’s goal of 4.50%. Keep in mind that since the graph requires 25 years of data, the last data point on the graph is December 1992.

Over the time frame illustrated, the investor is subjected to anxiety-inducing random high and lows relative to his target return. His portfolio performance is a flag in the wind at the mercy of the volatility of the equity markets.

Instead of rolling the dice like an investor managing and benchmarking towards the S&P 500, why not manage your portfolio based on an index that will properly target a dollar amount of purchasing power in the future? In our prior example, achieving an investment benchmark of the annual rate of CPI plus 4.50% would allow our investor to retire with at least $1,500,000 in today’s purchasing power.

Inflation based indexing

Unlike benchmarking to a popularly traded equity or bond index using ETFs and mutual funds, managing to an inflation-linked benchmark is more difficult. It requires an outcome-oriented approach that considers fundamentals and technical analysis across a wide range of asset classes. At times, alternative strategies might be necessary or prudent. Further, and maybe most importantly, one must check one’s ego at the door, as returns can vary widely from those of one’s neighbors. The challenge of this approach explains why most individuals and investment professionals do not subscribe to it. It is far easier to succeed or fail with the crowd than to take an unconventional path that demands rigor.

The reward for using the proper index and successfully matching or exceeding it is certitude. The CPI-plus benchmark approach described here is far more honest and durable in its ability to compound wealth and show definitive progress. It is deliberate and does not hand over control of the outcome to the whim of the market. It also requires an investor to avoid the hype and distractions that continually surround the day-to-day movements of the stock market.

Summary

We understand the difficulty in achieving one’s financial goals, especially in today’s unique environment of low-interest rates and high stock market valuations. Why compound the difficulty by managing your wealth to the random volatility of an index or benchmark that is different from your goals? Matching the performance of the S&P 500 is cheap and easy for a reason. It is also irrelevant to compounding wealth as it ignores important aspects of the wealth management process such as avoiding large and wealth-debilitating drawdowns.

Meeting your goals requires a logical and deliberate strategy guided by a set of rules that few investors understand. There is a reason many investors and retirees are failing to meet their goals. Using a reliable but different approach will help ensure that you don’t end up as one of them.

Twitter: @michaellebowitz

Any opinions expressed herein are solely those of the author, and do not in any way represent the views or opinions of any other person or entity.

: Showing Some Signs of Emerging Strength")