The media once again presumes that America’s financial negligence will result in a new global reserve currency. As we wrote in The Dollars Death, Not So Fast Part I, “Don’t hold your breath. Headlines forecasting the dollar’s death as the world’s reserve currency have been around for a long time.” While the case for a new global reserve currency is strong, the replacement options pale in comparison. There are four important reasons why finding a replacement will prove difficult.

The four reasons, the rule of law, liquid financial markets, and economic and military might, all but guarantee the death of the dollar will not occur anytime soon.

The Dollars Death, Not So Fast Part I provides background for the dollar’s role as the global reserve currency and the inherent flaws in serving that role. The construct of the dollar and the reasons for its birth as the world’s currency is an essential foundation for understanding its current position.

Key Takeaways

- The dollar will be extremely hard to replace for four reasons: The rule of law, liquid financial markets, and economic and military might.

- 60% of global currency reserves are in dollars, and about 90% of trade occurs in dollars.

- No other currency or block of nation’s currencies, gold-backed currency, or bitcoin is currently a viable candidate to replace the dollar as the global reserve currency.

The Rule of Law

The rule of law helps ensure that U.S. citizens and institutions are provided human rights, property, contracts, and procedural rights. While many other nations may claim to have similar legal processes, few live up to U.S. standards. The legal system equally protects foreigners with dollar and other financial and legal interests in the U.S.

From a currency perspective, the court system, not a government decree, rules on financial disputes. It is undoubtedly flawed and biased. As Russia, Iran, and other countries have found, the U.S. government will seize their dollars if they deem it in its best interest. While such acts bend the value of the rule of law, almost all foreign nations are confident that the U.S. system of law and governance ensures their ability to hold and transact in U.S. dollars. Further, laws and regulations provide confidence in the proper functioning of U.S. markets they rely heavily on to meet their borrowing and investment needs.

Hedge fund mogul Mark Mobius is discovering why investing in countries less judicious than the U.S. can be dangerous. Per CNN:

“I have an account with HSBC in Shanghai. I can’t take my money out. The government is restricting the flow of money out of the country,” Mobius, founder of Mobius Capital Partners, told FOX Business on March 2, 2023.

For those thinking that China, Russia, and Saudi Arabia can cobble together a reserve currency, ask yourself a question. If you were the leader of a nation, would you leave funds in their banking system or trust their government with said funds? More importantly, do you even think those countries trust each other?

Liquid Markets

From an operational perspective, the size and liquidity of U.S. financial markets and the ease with which foreigners can borrow and invest U.S. dollars are of utmost importance.

Foreigners enacting global trade need dollars to facilitate exchange. Therefore, they hold dollars and maintain the ability to borrow dollars. International trade requires a financial system with immense liquidity. Further, the more liquid a market, the lower the borrowing, investing, and hedging costs.

In this respect, the U.S. is second to none. The U.S. bond markets are considered the world’s deepest and most liquid markets. As we quote below, the U.S. bond market accounts for almost 40% of all bonds outstanding globally.

Per the Securities Industry and Financial Markets Association (SIFMA): “As of 2021, the size of the bond market (total debt outstanding) is estimated to be at $119 trillion worldwide and $46 trillionfor the U.S. market.”

Military Might

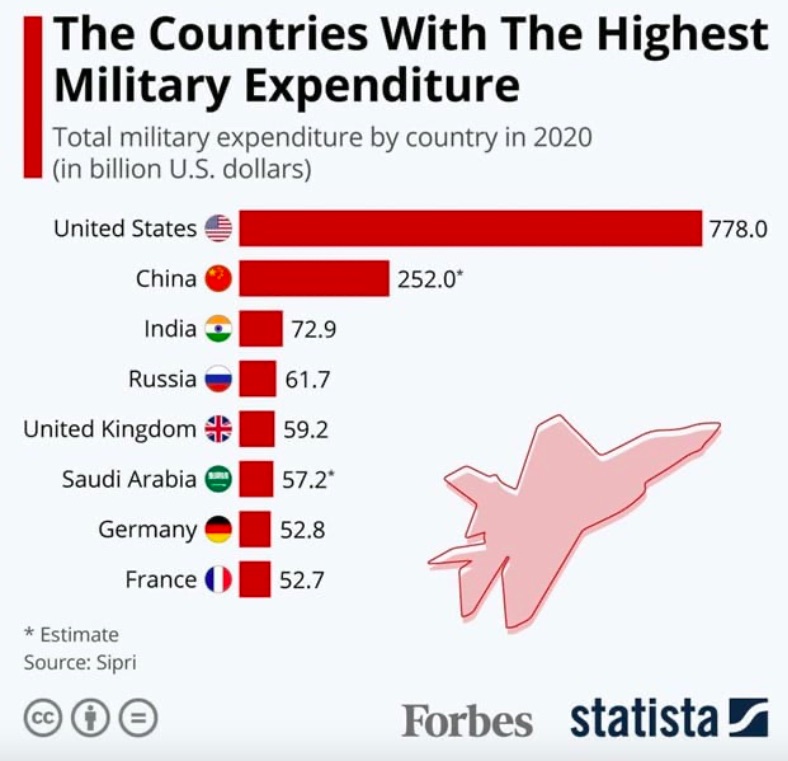

A key factor allowing Europe and Japan to recover quickly from World War II was the ability to borrow U.S. dollars and use the money to focus on rebuilding. Equally important, they did not have to refortify their military for another war. America had its back if another country were to invade. As a result, over 750 US military bases currently exist in more than 80 countries.

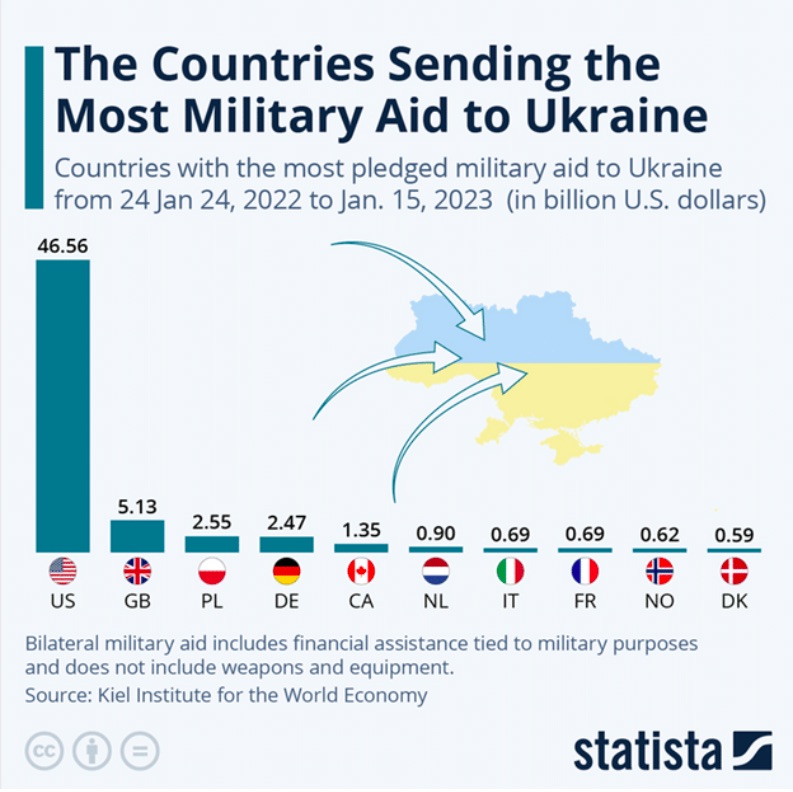

Let’s consider Ukraine’s situation. Its defense against Russia is being heavily funded and supported by the U.S. What might happen if Ukraine starts trading with Chinese Yuan or Euros? Do you think America would still give them the support they desperately need? Does Ukraine have the ability to forgo using the dollar in trade? The answer to both questions is a definitive no.

The graph below shows the U.S. Accounts for about 80% of military aid to Ukraine.

With China and Russia flexing their military muscles, other countries are watching the situation and recognizing that the dollar and America’s military are a package deal.

Given America’s superpower status, for another currency to become the global reserve currency, accepted by an overwhelmingly large percentage of countries, that replacement government will have to defeat the U.S.

Economic Power

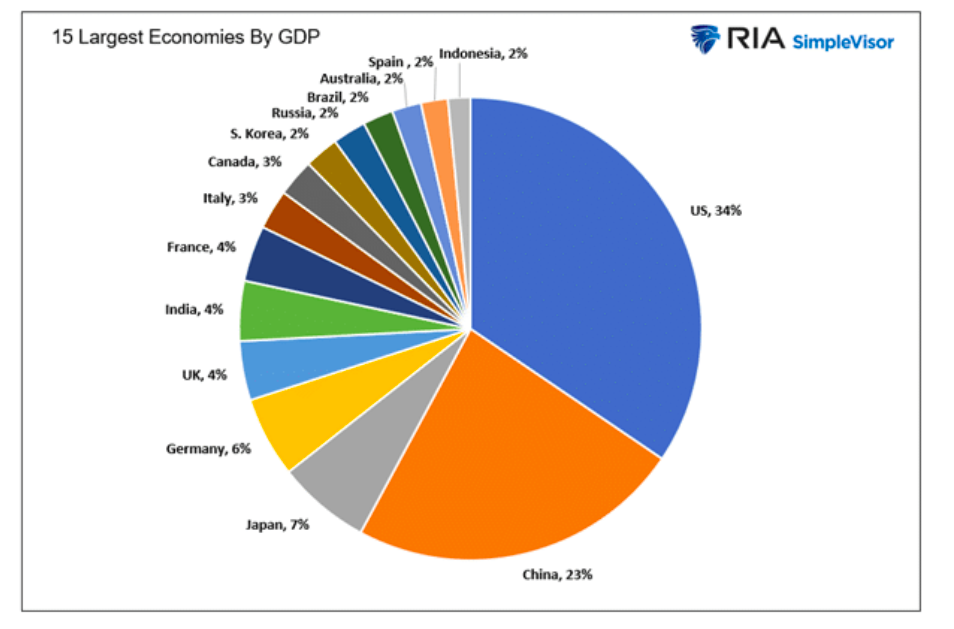

As shown below, the United States economy is roughly the same size as the next three largest economies combined. Given U.S. economic activity dwarfs every nation but China, a large percentage of global trade involves U.S.-based buyers and sellers. The dollar is the preferred currency to facilitate exchange with these entities.

Current Dollar Status

According to the IMF, the dollar makes up almost 60% of global foreign exchange reserves. While the percentage has declined by about 10% over the last decade, it is still three times the next leading reserve, the Euro, which accounts for about 20% of global reserves. For those concerned about China, their currency, the renminbi (yuan), accounts for 2.5% of all reserves. That is reason enough to count China out.

Per the BIS, foreign dollar-denominated debt totals approximately $16 trillion. That is up from $10 trillion in 2008. Next in line is foreign Euro-denominated debt at roughly $4 trillion. That amount has not changed since 2008.

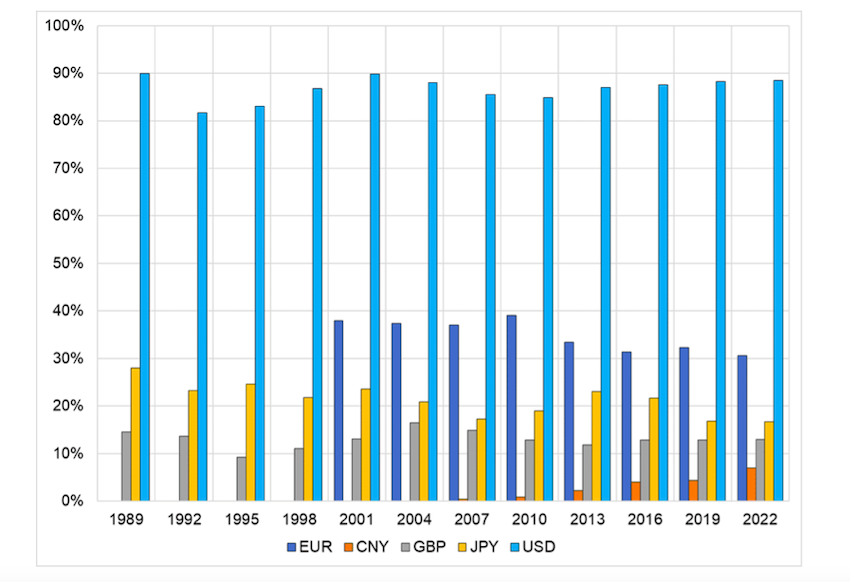

Data from the BIS and the graph below from @donnelly_brent show the dollar accounts for almost 90% of global transactions. That percentage has been steady over the last thirty years.

Summary

The pundits will be right someday. The dollar’s death as the reserve currency will come, and some other nation’s currency, cryptocurrency, gold, shells, or something else will take its place. However, that day is not coming anytime soon. The four reasons we describe in the article leave the world with no alternative.

While China is rapidly growing its economy and global trade footprint, it lacks the rule of law and liquid capital markets to sustain a global currency. It’s difficult to see how a communist country can overcome those challenges.

The Euro is the most viable competitor. They have the rule of law, but their capital markets are not nearly liquid enough to facilitate global trade. They also lack the military might to force the usage of the Euro. Let us also remember its finances are in equally bad or even worse shape than the U.S. There is no reason to suspect the euro could overtake the dollar.

Bitcoin? Forget about it! The government will never relinquish its control over the currency because, with that, they lose control of the nation.

Gold-backed dollars were a mainstay until 1971. However, as we have learned for the last fifty years, gold restricts the ability of the central bank to run monetary policy as they see fit. A rules-based system, like gold-backed dollars, might benefit the economy. However, regardless of your thoughts, the Fed and government are not ones to give up power.

Twitter: @michaellebowitz

The author or his firm may have positions in mentioned securities at the time of publication. Any opinions expressed herein are solely those of the author, and do not in any way represent the views or opinions of any other person or entity.

: Worrisome to Broader Market?")