Corn news and market analysis for the week of September 23, 2019.

Here’s a look at Corn data and news highlights, along with my analysis and outlook for Corn futures prices.

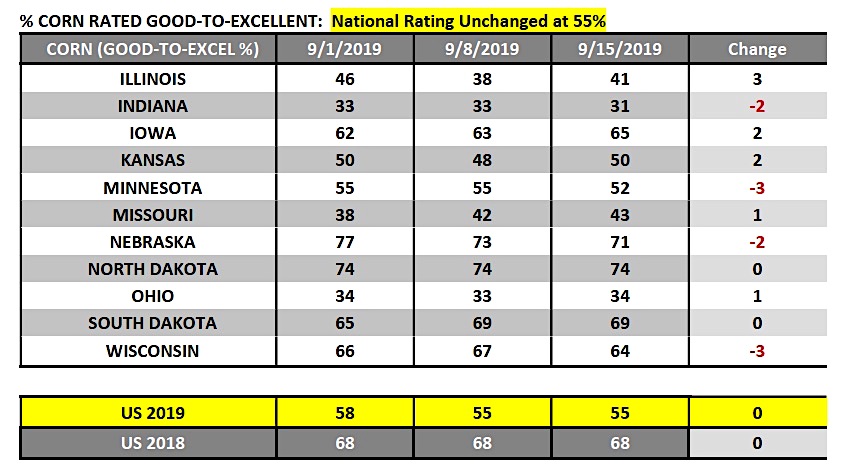

Last Monday’s Crop Progress report offered no changes to the national good-to-excellent rating in corn, which held steady at 55% versus 68% a year ago for the week ending September 15, 2019.

That said, within the top 5 state corn producers there was some movement in their good-to-excellent ratings. Iowa and Illinois enjoyed 2% and 3% increases respectively. Meanwhile Nebraska and Indiana saw their corn ratings dip 2% with Minnesota’s rating down 3% to 52% good-to-excellent.

The report also showed 68% of the U.S. corn crop “dented” versus 92% in 2018 and the 5-year average of 87%. Of note, North Dakota’s corn crop was just 38% dented versus 91% in 2018.

In the September Crop Production report, the USDA forecasted 2019 North Dakota corn production at 474.15 million bushels via a 145 bpa yield on 3.27 million harvested acres (8th largest harvested acreage base in the U.S.). It will be very interesting to see how North Dakota’s corn crop finishes given the lack of crop maturity at this late date in the growing season. And finally, 18% of the U.S. corn crop was estimated as “mature” versus 51% a year ago and the 5-year average of 39%.

Last week’s report underscored once again that the 2019 U.S. corn crop will need a frost-free, early to mid-October to avoid potentially significant corn yield reductions in the Upper Midwest.

Last Wednesday’s EIA report showed weekly U.S. ethanol production falling to 1.003 million barrels per day. This was the lowest weekly run-rate since April 5th, 2019 (1.002 million barrels per day).

Despite the lower production figure, U.S. ethanol stocks climbed back up to 23.238 million barrels, an increase of 739,000 barrels versus a week ago.

Last Thursday’s weekly Export Sales report showed U.S. corn export sales totaling 57.5 million bushels for the week ending September 12th.

2019/20 crop year-to-date U.S. corn export commitments improved to 340.7 million bushels, however this was down 311 million bushels from last year (or -48%). It’s important to note that in the September 2019 WASDE report the USDA forecasted 2019/20 U.S. corn exports of 2.050 billion bushels, just 10 million bushels below 2018/19.

That said, it’s going to be critical the corn export sales pace improves considerably over the next 4 to 8-weeks or I believe the USDA will have to start lowering their 2019/20 export forecast as early as the November 2019 WASDE report. In general, the U.S. continues to face stiff export competition from Argentina, Brazil, and Ukraine which collectively exported a record high 103.5 MMT of corn in 2018/19.

The previous high for those 3 countries was 78.9 MMT in 2016/17 (a difference of 24.6 MMT or 968 million bushels). I also learned this week that the average selling price for corn during the month of August in Mato Grosso, Brazil was less than $2.40 per bushel. Therefore corn supplies from the non-U.S. major world exporters are both ample and economical.

Lastly… early in the week reports surfaced that President Trump had tentatively agreed to a plan to increase the amount of biofuels blended into gasoline in 2020. These increases would in part take into account the total amount of biofuel gallons currently exempted from mandates due to the EPA’s recent approval of 31 Small Refinery Exemptions.

However, on Thursday President Trump then met with state senators from U.S. oil states who were obviously opposed to any such increases in mandated biofuel use. The EPA has until the end of November to finalize its 2020 biofuel mandates. That said this debate is likely far from over; however the U.S. ethanol industry has a lot riding on the outcome. Industry “Average” Net Ethanol Margins remain negative have been negative since August 2018.

U.S. CORN FUTURES TRADING OUTLOOK

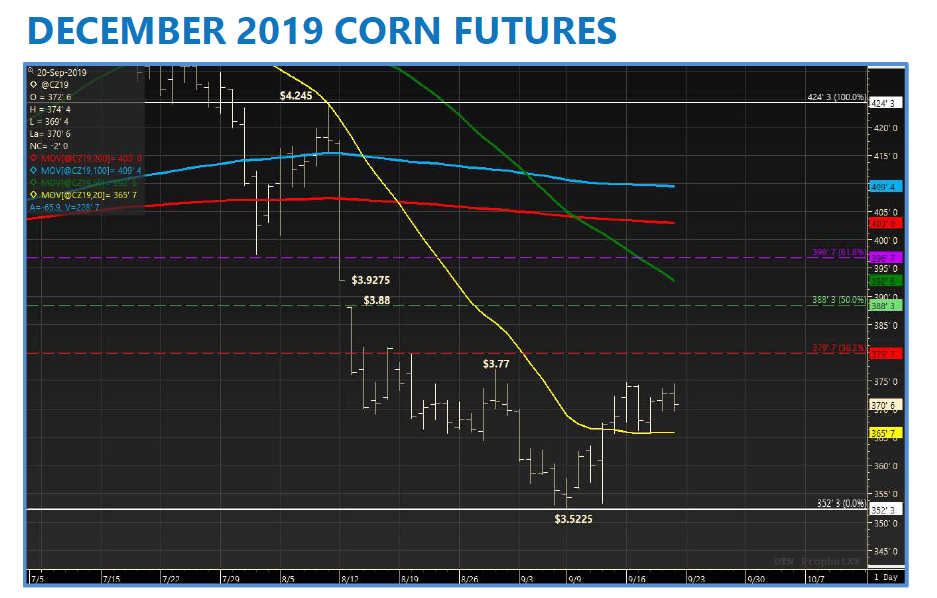

Corn futures showed signs last week of wanting to rally; however every attempted “up move” stalled just prior to $3.75 per bushel.

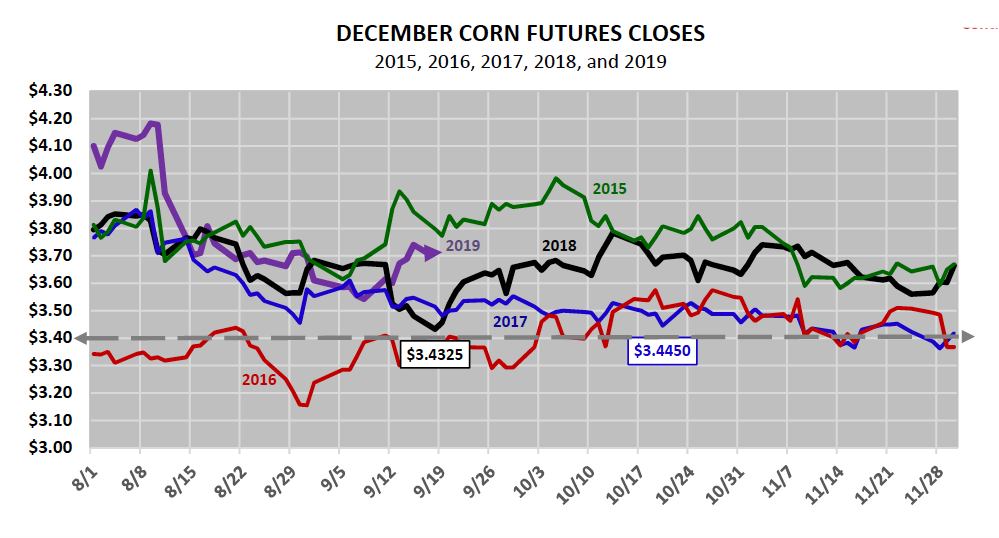

That said, despite strong topside resistance above $3.75, the market was able to fend off a push back down to the recent contract low of $3.52 ¼ (established on 9/9) finding good price support at the 20-day moving average of $3.657. Overall, December corn futures traded in just a 9-cent range for the week from $3.65 ¾ to $3.74 ¾.

Where does CZ19 go from here?

Friday’s Commitment of Traders report might offer some indication. That report showed Money Managers expanding their net corn short to -170,626 contracts as of the market closes on 9/17. Since 2015 the largest Managed Money net corn short accumulated during the month of September has been -180,893 contracts. This coming in September 2016. Therefore considering the current 2019/20 U.S. corn S&D offers many parallels to the last 4-crop years; it would seem Money Managers are close to maxing out their downside position exposures.

Will Managed Money short covering generate a significant rally?

The challenge to sustainable rallies above $3.80 in December corn futures will be that even with Money Managers potentially buying back a sizable percentage of their current short corn position, as the U.S. corn harvest accelerates in October, Commercial hedge/sell paper will more than offset Managed Money buy-backs.

I still believe CZ19 eventually trades back over $3.80 in October; however rallies back to $3.95 to $4.00 will likely have to come from a Bullish yield surprise in the October 2019 WASDE report (released on 10/10/2019). Corn Bulls need a story and hopefully that story will be written as actual 2019 corn harvest results start to filter back in showing the real effects of this year’s record corn planting delays on U.S. corn yields (lower plant populations, lower test weights, lower harvested acreage).

Twitter: @MarcusLudtke

Author hedges corn futures and may have a position at the time of publication. Any opinions expressed herein are solely those of the author, and do not in any way represent the views or opinions of any other person or entity.

")

Testing Important Price Support")