Key Takeaway: Federal Reserve studies suggest expansions are lasting longer and do not die just from old age. No one knows what the future will hold, but current evidence suggests recession risk remains minimal and even some of the weaker areas of the United States economy are seeing signs of life.

The San Francisco and St. Louis Federal Reserve Banks have published brief articles over the past month addressing the question of whether the U.S. is due, strictly from a calendar perspective, for another recession.

Given the turmoil in the energy sector over the past year, a well-publicized statement from a CEO that the “industrial environment is in recession”, and the uncertain global outlook, the potential timing of the next recession in the United States seems to have taken on more urgency.

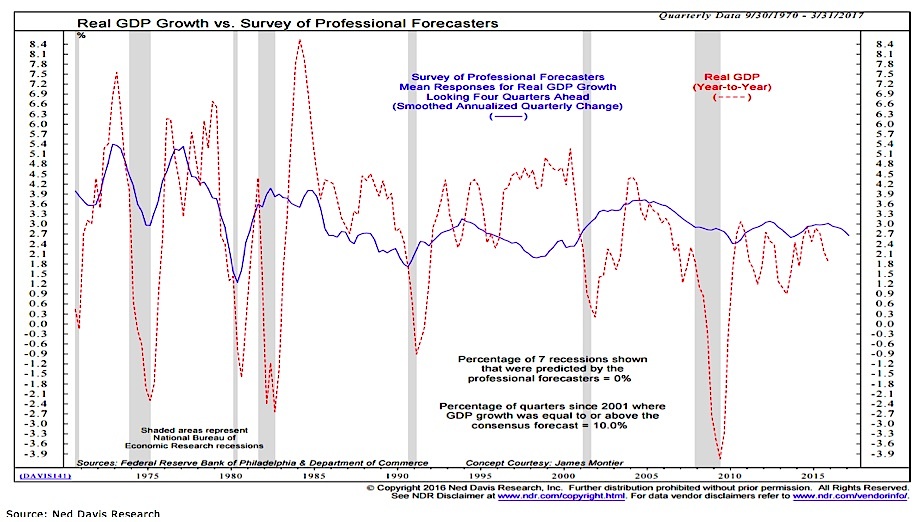

The conclusion of the article from the St. Louis Fed (available here) is business cycle expansions have gotten longer over time. The last three completed economic expansions were all longer than the historical average. The economy has currently been in expansion for 80 months – longer than the historical average of just under 60 months, but still shy of the average of the last three economic expansions (95 months). The authors of this article also make the following point: “Unfortunately, there is no reliable way to predict the economic growth rate, making it difficult to forecast when the next recession will hit.” We would heartily endorse that view. While recent experience has been that forecasters have been too optimistic, there was a period in the not-too-distant past when forecasters were consistently too pessimistic.

The San Francisco Fed article (available here) asked whether recoveries die of old age. In other words, do economic expansions become more fragile and susceptible to recession simply due to the passage of time? The conclusion is that there is no evidence of this. So even as the current expansion lengthens, we are not living on borrowed time from the perspective of the calendar.

Rather than watching the calendar, or relying on forecasts, we focus on observed data. The quote by the CEO mentioned at the outset resonated with many people for a variety of reasons, but mostly it seems, because the comments confirmed what many were feeling already.

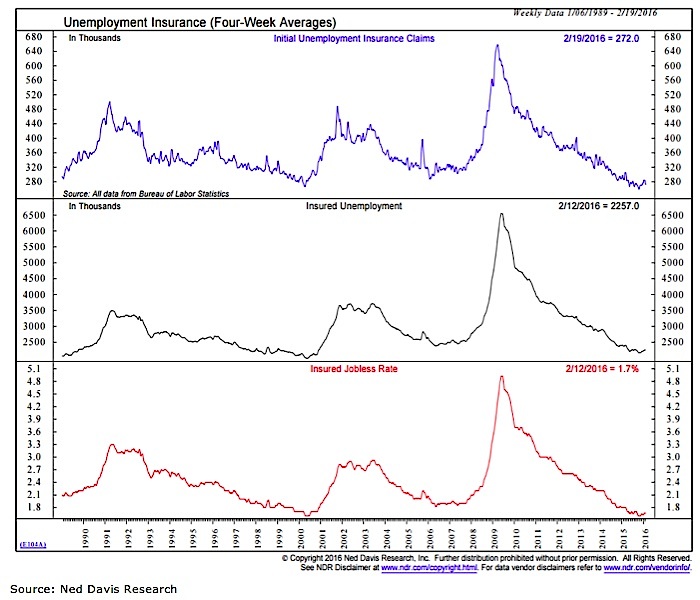

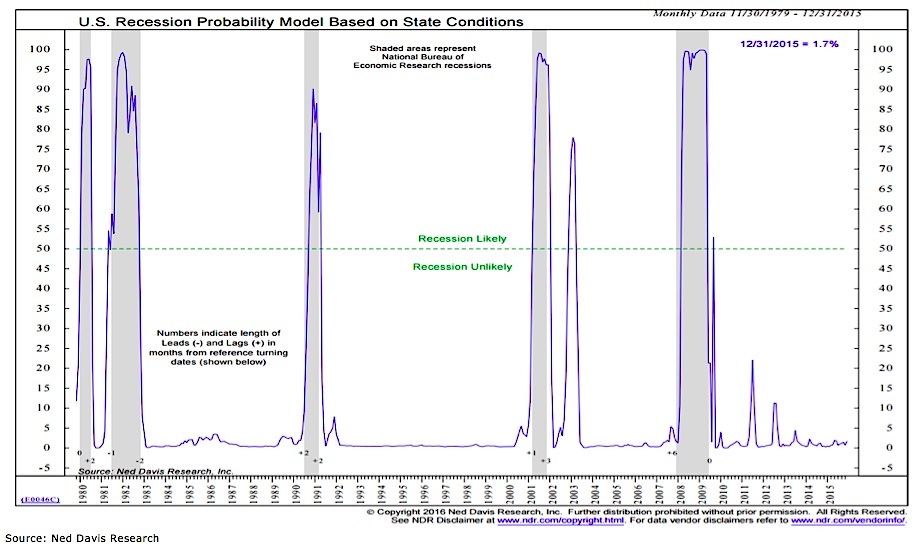

To be sure, some areas of the economy have been quite weak over the past year and the benefits of the expansion have been unevenly distributed. But initial jobless claims (the single-best real-time measure of economic health in our view) have remained low, suggesting labor market conditions are still relatively health. Real-time recession risk models for the United States have not shown a meaningful uptick.

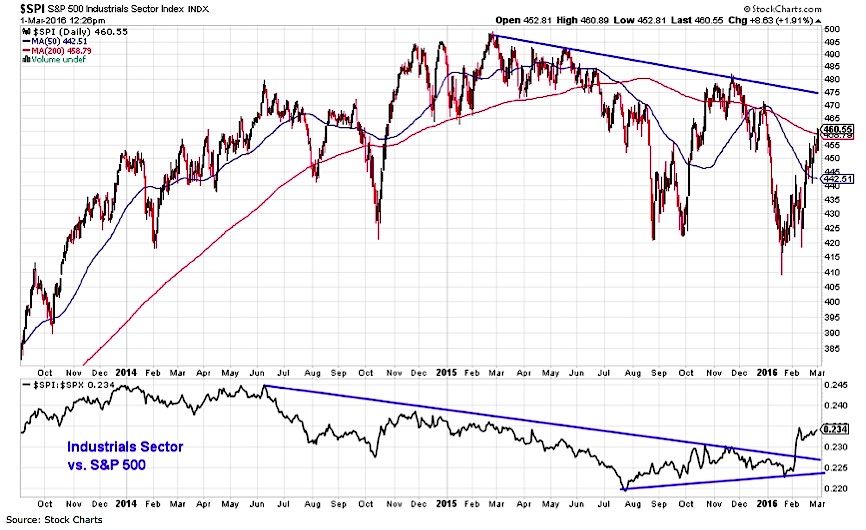

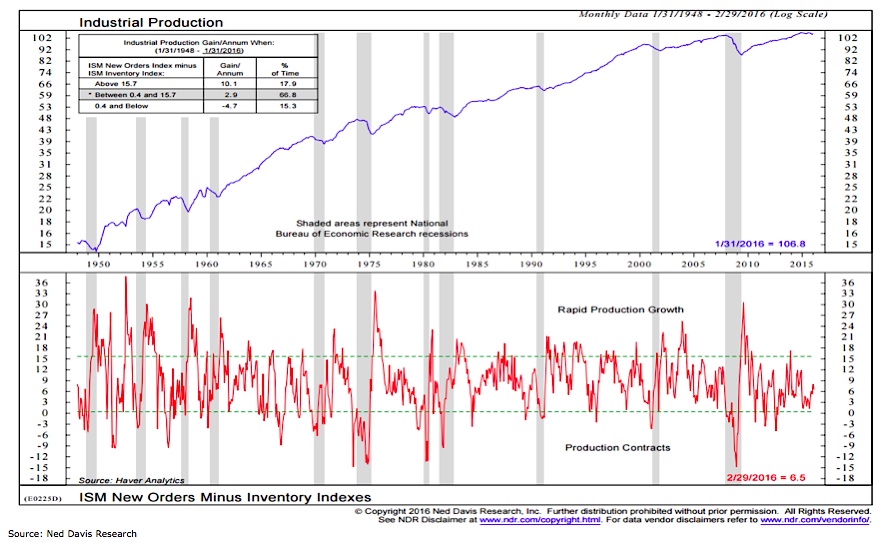

There is even some evidence that the worst of industrial-related weakness is in the past. Industrial stocks have gained strength relative to the rest of the stock market since August and the spread between the New Orders and Inventories components within the ISM Report on Business has improved markedly in recent months.

Thank you for reading.

Further reading from Willie: “Stock Market Rally Update: Investors Remain Skeptical“

Twitter: @WillieDelwiche

Any opinions expressed herein are solely those of the author, and do not in any way represent the views or opinions of any other person or entity.

Trading Near Top Of Price Range")