On March 7, we asked Will the Market Internals Turn More Bearish?

While we focused mainly on Jerome Powell’s testimony, “If the totality of the data were to indicate that faster tightening is warranted, we would be prepared to increase the pace of rate hikes.”

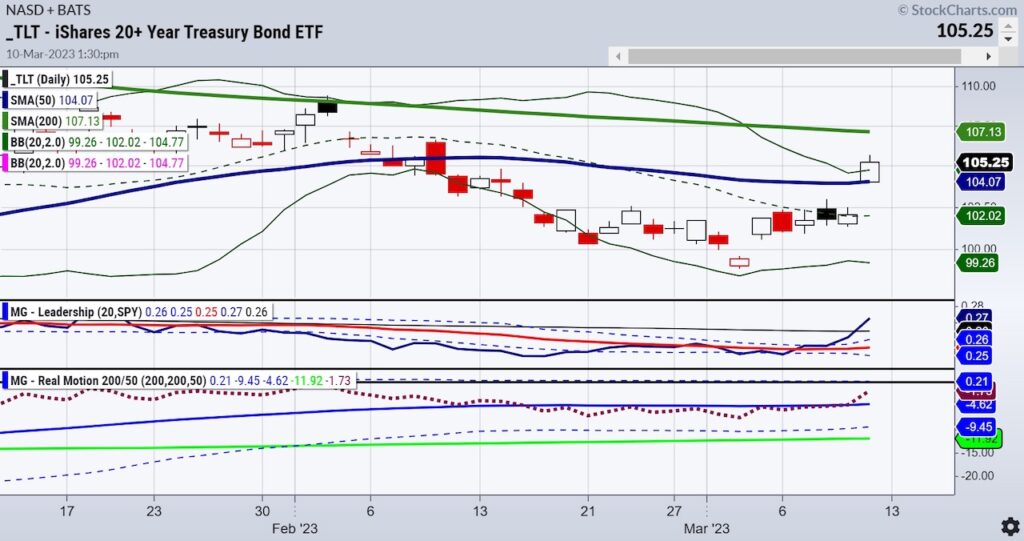

In the same Daily, we featured the long bonds (TLT) and that the chart had a constructive exhaustion gap bottom in play.

We went on to write,” the Real Motion indicator shows a positive divergence as momentum is just under the 50-DMA while price is considerably below its 50-DMA.”

The question asked was, why would the long bonds bottom? Our answer,

“It could mean that while the short-term yields invert, the market is expecting a recession, hence a flight to safety in long bonds.

We imagine that should 20+ year bonds continue to go north, that too can be inflationary.”

We started the year introducing our report, How to Grow Your Wealth in 2023. In this Year of the Yin Water Rabbit, we began with:

You Can’t Run with the Hare and Hunt with the Hounds.

Little did we know then, how well this describes the Federal Reserve, the reversal in TLTs and the catalyst of 2023’s biggest dilemma of all-

Recession or Stagflation-What will it be?

More from the Report:

“For 2023 one word and two expressions keep coming up:

Chaos

Trying to fit a square peg into a round hole.

Looking for Inflation in All the Wrong Places”

Of course, the biggest headline this week in finance is the collapse of SVB and Silvergate.

That sounds a lot like Chaos.

The full fallout is unknown, but if the market has anything to say about it, both long bonds and gold rallied.

Folks calling for deflation are using Money Supply decline as an example. They are citing “higher for longer” concerning rates.

They are talking about the strong labor market.

BUT

That is more of Trying to fit a square peg into a round hole.

Five reasons why folks are looking are for inflation in all the wrong places:

1. Climate-Natural Disasters

2. Food shortages could prevail-hoarding-sugar prices flying

3. Social unrest from high inflation, higher yields, losing credibility (banks, government)CLASSIC example this week.

4. Geopolitics-rising tides of issues-we hope not but be prepared.

5. Government spending/Federal Reserve-what are they going to do now? Print? Save the banks? Keep raising rates creating more liquidity crises?

The chart of the TLT shows price clearing the 50-DMA. That is an unconfirmed phase change to Recuperation. A second consecutive close above will confirm the phase change.

Clearly the Leadership indicator tells a story as bonds well outperform the SPY.

And the Real Motion of momentum indicator, already with a positive diversion as mentioned on March 7th, now could stay in gear.

Could the picture reverse next week?

Yes. However, to quote the Report:

“The lesson we should take from this is not that inflation is destined to move to new highs in the months ahead (after all, nearly 30% of the time, it is, in fact, cresting!), but that we dismiss that possibility at our peril. “

Our Global Macro Quant Model bought gold. Even the algos know what’s up!

ETFs Trading Analysis & Summary:

S&P 500 (SPY) Our trading range theory was 4200-3200-maybe

Russell 2000 (IWM) 170 next major support 182 resistance

Dow (DIA) 310 support 324 resistance

Nasdaq (QQQ) Unconfirmed bearish phase-confirms if second close under 290

Regional banks (KRE) Maybe overdone for now-but not necessarily done. 40 target 55 resistance

Semiconductors (SMH) Still in a bullish phase-over 240-maybe a pop for everything

Transportation (IYT) 223 the 200-DMA major support-2nd in strength to SMH

Biotechnology (IBB) Teetering on the 80-month MA at 121.

Retail (XRT) Under 64 remains weak-next big support at 56.00

Twitter: @marketminute

The author may have a position in mentioned securities at the time of publication. Any opinions expressed herein are solely those of the author and do not represent the views or opinions of any other person or entity.

: Creating Bullish Divergence?")

and Semiconductors (SMH): Concerning Price Pattern?")

and Semiconductors (SMH): Concerning Price Pattern?")