THE BIG PICTURE

Investors are operating in a volatile stock market climate so it pays to be nimble and in trend (with your trading timeframe).

Stocks are rallying higher once more but there is plenty of “noise” due to market crosscurrents and disappointed bears. Traders need to follow the price action (and indicators) and steer clear of noise and opinions. If the market correction continues, your process (and stops and limits) should offer you new looks on both the long & short side of trades.

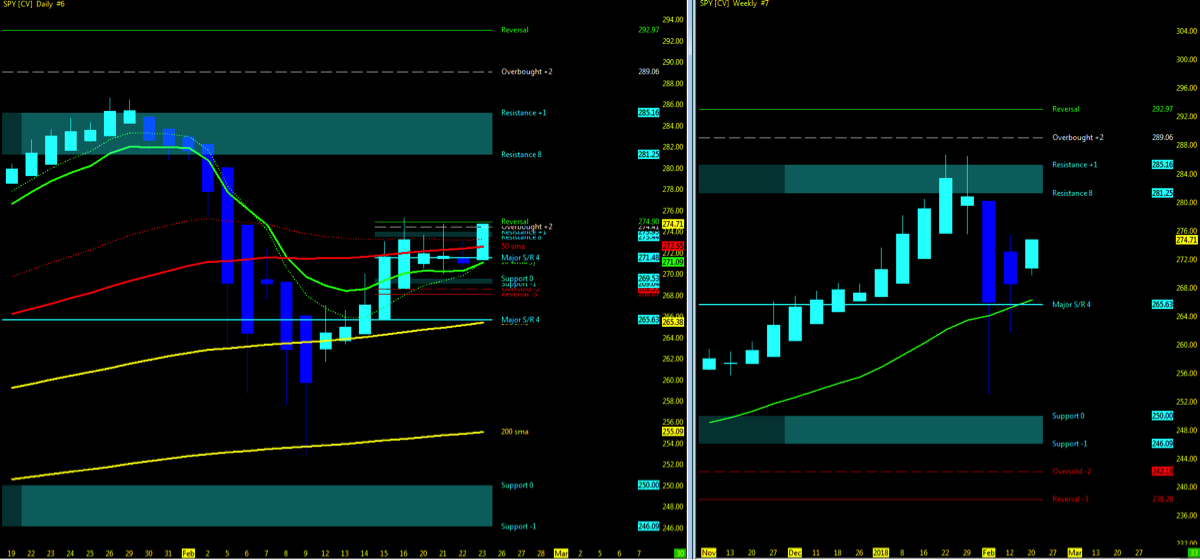

Below is my weekly stock market futures trading update and trend outlook. Let’s start by looking at a chart of the S&P 500 ETF (SPY).

S&P 500 Chart – Week 9 (week of February 26)

Using the Murray Math Level (MML) charts on higher time frames can be a useful market internal tool as price action moves among fractal levels from hourly to weekly charts. Confluence of levels may be levels of support/resistance or opportunities for a breakout move. Optimal setups will pass through Resistance or Support prior to moving in the opposite trend.

Technical Trends

- Week 08 recap and trend charts

- Stock market indices hold at 50ma; the Nasdaq is pushing higher.

- Open Gaps above and below; but none formed in week 8

- VIX Volatility Index levels decrease to mid teen’s

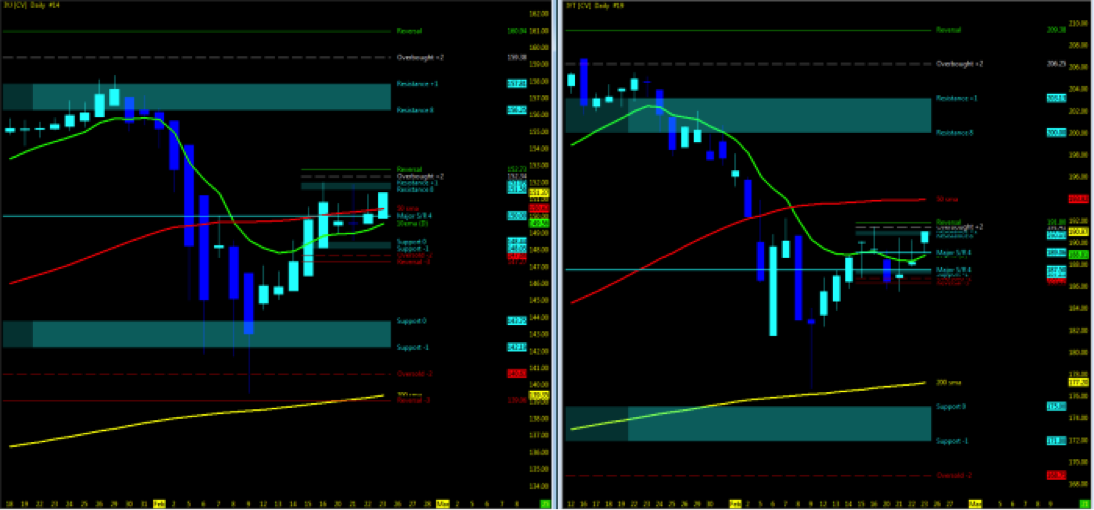

- Dow Jones Industrials / Transports

- Industrials UPTREND: PRICE>50>10>200; Transports UPTREND: 50>PRICE>10>200

- Monitor for the two ETF indices to remain in sync as supporting indicator of momentum

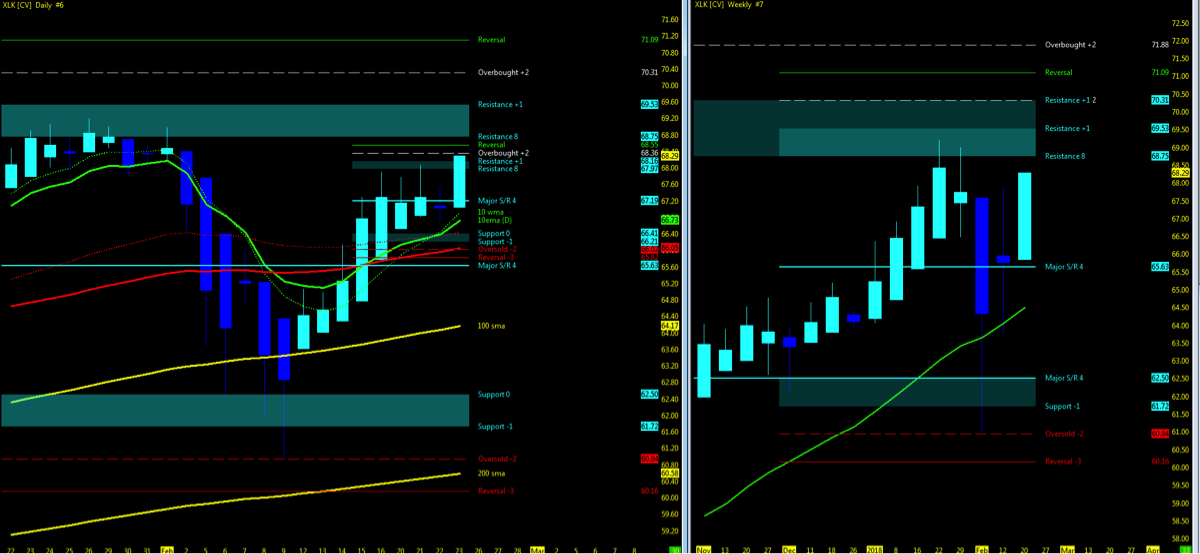

- The Tech Sector remains in an UPTREND

- NYAD (NYSE Advance – Decliners)/INDU in sync upside

Key Events in the Market This Week

- USA: Home Sales, Durable Goods, Consumer Confidence/Sentiment, GDP, Motor Vehicle Sales, Personal Inco

- Q4 earnings:

- Salesforce

- Payment companies

- Oil and Gas

- Departments stores

- Shoemakers

- Fed Chief yearly report

The Bottom Line

Momentum on the indices may have given lift at the end of week 07 to only consolidate in week 08 on average daily volume. It appears while the market is content to not sell under the 200ma, which in this humble traders opinion will be the floodgates opening is not ready to return to all time highs.

Breakout of the 50ma is the moving average surely to watch and monitor for the short term 10ma to cross back above the 50ma to correlate a positive trend upside in addition to trending Heiken Ashi bars. Otherwise, if unable to break upside, watch for a return back down to 200 if price closes under the 10ma on the daily.

Momentum surely not supporting the return to the lows and while the wish may be for lower prices to end out Q2, positive earnings, strong XLK/FDN and overall Big Pic may keep week 09 pushing higher as long as we can fill the bill of above and breakout of the 50.

Watch for MML setups on price action break above resistance high and back under resistance low for first signs of a pullback. Downside, watch for open gaps to be closed and 50% pullback as 1st level of support.

Attempting to determine which way a market will go on any given day is merely a guess in which some will get it right and some will get it wrong. Being prepared in either direction intraday for the strongest probable trend is by plotting your longer term charts and utilizing an indicator of choice on the lower time frame to identify the setup and remaining in the trade that much longer. Any chart posted here is merely a snapshot of current technical momentum and not indicative of where price may lead forward.

Thanks for reading and remember to always use a stop at/around key technical trend levels.

Twitter: @TradingFibz

The author trades futures intraday and may have a position in the mentioned securities at the time of publication. Any opinions expressed herein are solely those of the author, and do not in any way represent the views or opinions of any other person or entity.

: Worrisome to Broader Market?")