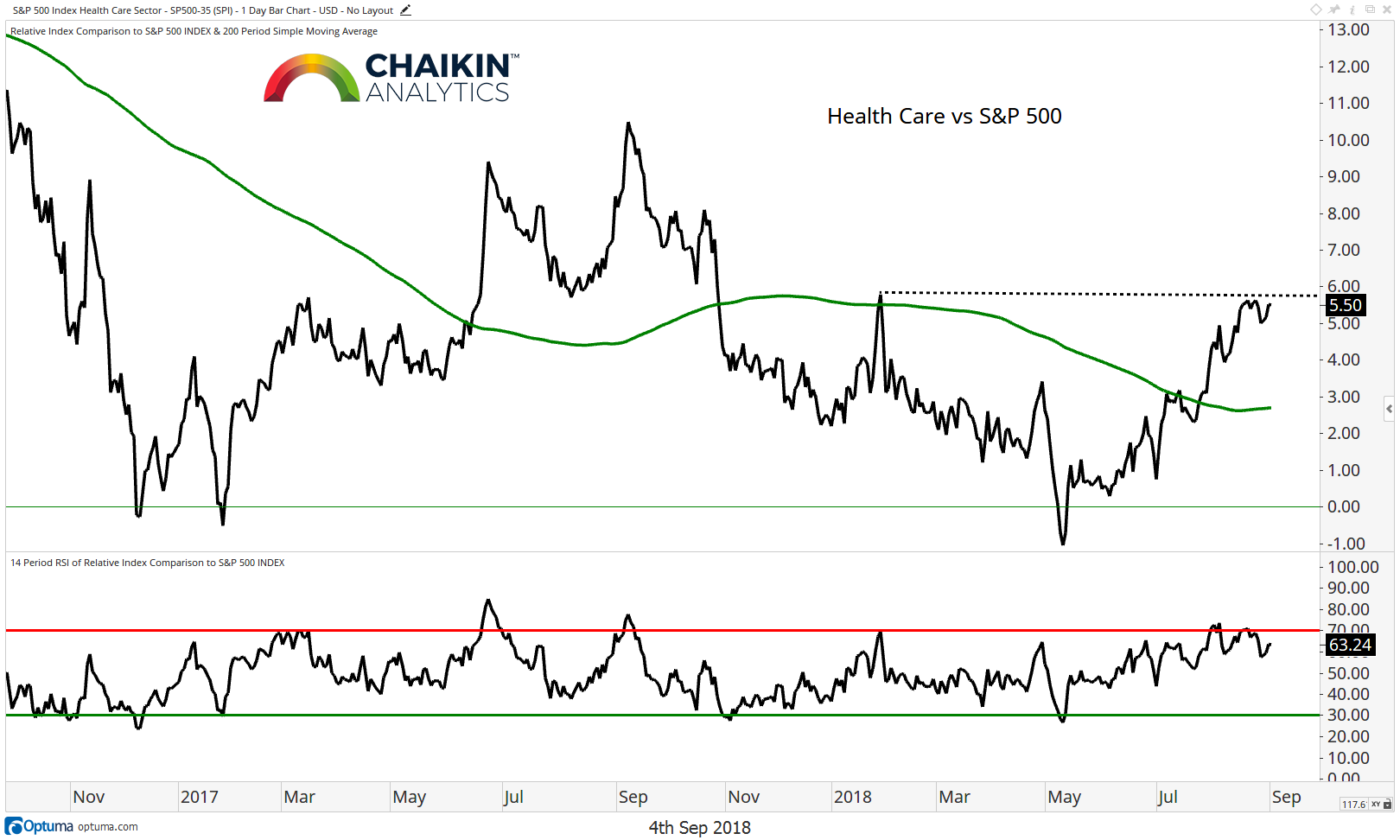

The RSI of the ratio remains in bullish ranges and recently became overbought which speaks to the strength of the emerging trend. We see this group as emerging leadership. In particular, we are closely watching the large Pharmaceutical stocks which are joining Services and Equipment as market leaders.

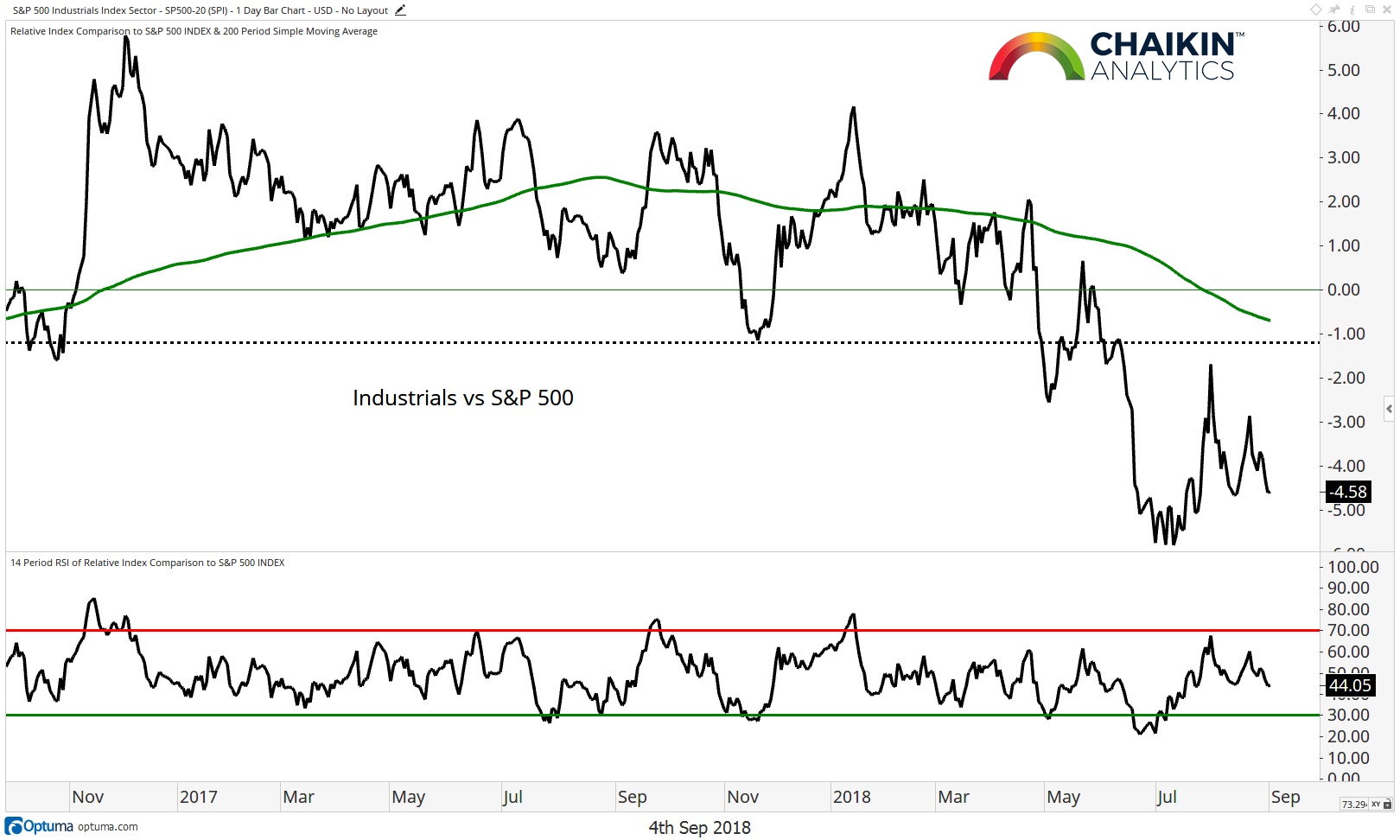

S&P 500 Industrials Sector Relative to the S&P 500

The Industrials sector is trying to halt the decline relative to the S&P 500. The sector remains below the falling 200-day moving average and the RSI was not able to reach overbought levels during the recent advances but is trying to move to bullish ranges. The group continues to trade below resistance and likely needs more time to form a relative bottom. In a positive development, the Power Bar ratio for the sector remains bullish but from a trend perspective, the sector is still weak. An ideal scenario would be a test/hold of the recent lows which would set the stage for a move higher.

S&P 500 Information Technology Sector Relative to the S&P 500

The Information Technology sector is consolidating within the context of a secular uptrend relative to the S&P 500. The RSI of the ratio was not able to register an oversold reading during the recent pullbacks which speaks to the strength of the trend. The sector remains above the rising 200-day moving average and the RSI has not become oversold since November 2017. Based on the Power Bars in Chaikin Analytics, the sector remains a leader with a bullish ratio which is stronger than the S&P 500. Within the sector, Software and select Internet names remain leadership, offsetting weakness in Semiconductors. Additionally, Hardware names have broken to new relative highs on the back of strength in AAPL.

S&P 500 Materials Sector Relative to the S&P 500

The Materials sector continues to be the worst performer from a trend perspective but there is the possibility that a counter-trend rally could emerge as there is a positive divergence between price and RSI. The sector remains below the declining 200-day moving average and heavy resistance. The Power Bar Ratio for the sector remains bearish and is the weakest of the sectors which we track. More time will be needed for Materials to form a relative bottom.

S&P 500 Real Estate Sector Relative to the S&P 500

The bottoming process continues for the Real Estate sector relative to the S&P 500 as the sector has traded around the 200-day moving average, however, more time is likely needed for the reversal to take place. In a positive development, the RSI became overbought during the July rally and has not registered an oversold reading since early 2018. A break through the July 5th high would signal that a new uptrend is likely developing.

S&P 500 Utilities Sector Relative to the S&P 500

The Utilities sector is also in the process of forming a base relative to the S&P 500. Utilities have a bullish Power Bar Ratio and are the strongest sector in the market based on that metric. On a relative basis, the sector remains below the falling 200-day moving average so more time is likely needed for the base to form. The RSI is trying to shift to bullish ranges after a large positive divergence at the June low. A break up and through the July 3rd highs would signal that a new uptrend is likely underway.

Take-Away: Despite some of the rotation which has taken place over the past few weeks, the major trends for the S&P 500 sectors remain in place. The Technology sector remains in an uptrend as does Consumer Discretionary. The Health Care sector is emerging leadership while Real Estate and Utilities are trying to form relative bases. Materials, Industrials and Consumer Staples have bearish relative trends. However, Materials appear extended in the near-term while Staples appear likely to resume their relative decline.

Twitter: @DanRusso_CMT

Author may have a position in mentioned securities at the time of publication. Any opinions expressed herein are solely those of the author, and do not in any way represent the views or opinions of any other person or entity.