By Andrew Nyquist The Euro was never given a fighting chance. Figuratively, and quite possibly literally. From conception, economists and investors questioned the Euro’s long-term viability. Formed with good intentions, the EU overlooked the Euro’s problematic structure consisting of a monetary union without full fiscal union. And after the past 4 years in crisis, it is clear that those concerns have become reality. The Euro crisis is maturing into full bloom, phase 2.0.

No doubt, the early days of the crisis were more forgiving, if not confusing. Socially, the people had more capacity for stomaching financial assistance packages for the likes of Greece, Ireland, Portugal, Spain, and numerous pensions and banking institutions. But those times are changing. And fast. With the German elections fast approaching, politics is beginning to infect the motherland. Large power brokers are doing what they can to manage the populace and the political process to give the impression of confidence, and to try and avoid the need to add another Euro crisis acronym to its growing list of band-aids: EFSF, EFSM, ESM, OMT, and LTRO. Just when you think a major restructure, treatise amendment, Euro Bonds, or other grand solution is about to be introduced, the Euro crisis just seems to find new ways to “patch” and carry on.

BUT, the complexion of the ongoing Euro crisis may have changed recently, for better or worse, with the Cyprus bailout package (if you want to call it a bailout). With politics (and differing financial views) in play, it is unclear if this was German muscle or true collaboration. As well, was the motivation for introducing the depositor tax solely to send a message to banks about the new format for receiving assistance (i.e. hitting depositors). Or was it simply a one-off occasion that needed extreme action? Over the weekend, the German Finance Minister stated, “the savings accounts in Europe are safe.” Then again, he also stated that Europe was enjoying a “very fortunate era.” Uh, say what?

Maybe it’s simply a combination of all of the above, leaving all options on the table while sending an indirect message to member states that they need to get their fiscal houses in order… a psychological reset of sorts. That seems logical, but it is also problematic in that social unrest is on the rise and bailouts are growing increasingly unpopular. And now depositors across the EU member states are worried. So what will the EU do when another emergency arises?

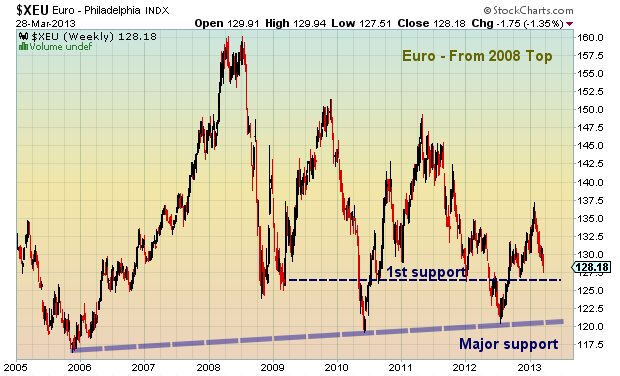

Below is chart of the Euro highlighting the current downtrend and key support levels to watch. In summary, a weekly close above the downtrend line would be bullish (see Euro chart 1). However, a sustained break of 1.265 would be bearish and open up the potential for a flush down to 1.20 near term (major support – see Euro chart 2).

Euro Chart 1 – Recent Downtrend: Resistance to Watch

Euro Chart 2 – From 2008 Top: Key Support Levels for Euro Crisis

Twitter: @andrewnyquist and @seeitmarket

No position in any of the mentioned securities at the time of publication.

: Worrisome to Broader Market?")