“Volatility” is a pedestrian word on Wall Street.

Traders, investors, and the media throw it around as if everyone understands its financial definition.

What matters, of course, is outcome. Volatility is an important determinant of outcomes and therefore deserves close consideration.

The word “volatility” refers to rapid and unpredictable change, but how many investors truly understand financial volatility?

How many investors grasp the influence volatility has on their investment results/outcomes?

Even more critical, who understands that volatility is an inverse gauge of liquidity, the foundation on which smooth-functioning markets and asset prices rest.

Textbook Volatility Defined

Volatility is a measure of the historical dispersion of returns around a mean. The greater the dispersion, the higher the volatility, and ultimately the range of potential outcomes.

Volatility is typically quoted as +/- 1 standard deviation. For instance, 14% annualized volatility means, with 68% certainty, we should expect annualized returns to be +/- 14%. The volatility formula describes a normal bell-shaped curve in which price changes should be contained.

Normal implies there are equal odds the market falls 1% or rises 1% versus the average change. The graph below depicts a bell-shaped curve. The diagram also highlights standard deviations and the percentage of data that falls within each deviation.

Normal Is Not Reality

The assumption of a normally distributed bell curve is at the heart of finance. Embedded in that assumption is the idea that market participants are rational and markets efficient. It drives risk management, option pricing, and many economic and market theories. The problem with such analysis is that the assumption is flat out wrong.

In a normal shaped curve, the S&P 500 should never move by more than five standard deviations up or down. By “never,” we mean once every 3.5 million trading days (approximately 14,000 years). Since 1970 there have been 34 such days. In March of 2020 alone, there were 7!

Using Volatility to Define Risk

Quite often, investors use volatility to define risk. For instance, with S&P 500 data from 1970, an investor can assume, with 95% certainty, that they will not lose more than 2.16% on any given day. By annualizing volatility, we can create measures of longer-term risks.

Investors often take the relationship between volatility and risk as gospel. That mistake often leads investors to underappreciate risk. Astute investors must understand the flaws in volatility assumptions and prepare for the statistically impossible.

Liquidity and Volatility

Now forget the bell curves and complicated statistics. Let’s redefine volatility to something simpler and more practical.

“Volatility is the opposite of liquidity, by definition.” – Per Todd Harrison @toddharrison

Here is what Todd means.

Market A has buyers and sellers willing to execute many shares in tight price increments around the current price.

Market B has few buyers and sellers willing to execute. Their bids and offers are smaller in size and in a less uniform range of increments around the current price.

A will trade up and down, penny by penny, in a somewhat orderly fashion.

B will trade up and down in much larger increments as buyers and sellers must relent more on price if they want to execute at the moment.

A is more liquid than market B. As a result, A will also be less volatile than B.

Liquidity is Fluid

Liquidity dynamics are fluid. If, for instance, confidence were to erode and uncertainty increases, liquidity conditions underlying Market A will deteriorate rapidly and look more like Market B. Such a situation leads to an imbalance in bids and offers, and it becomes less clear where the market-clearing price is.

As a result, prices “gap” or lurch down as potential buyers step away. Desperate seller then panic to find a price to transact. In other words, volatility soars when markets are less liquid. Conversely, volatility is low and stable when markets have an equilibrium of bids and offers concentrated around a common price.

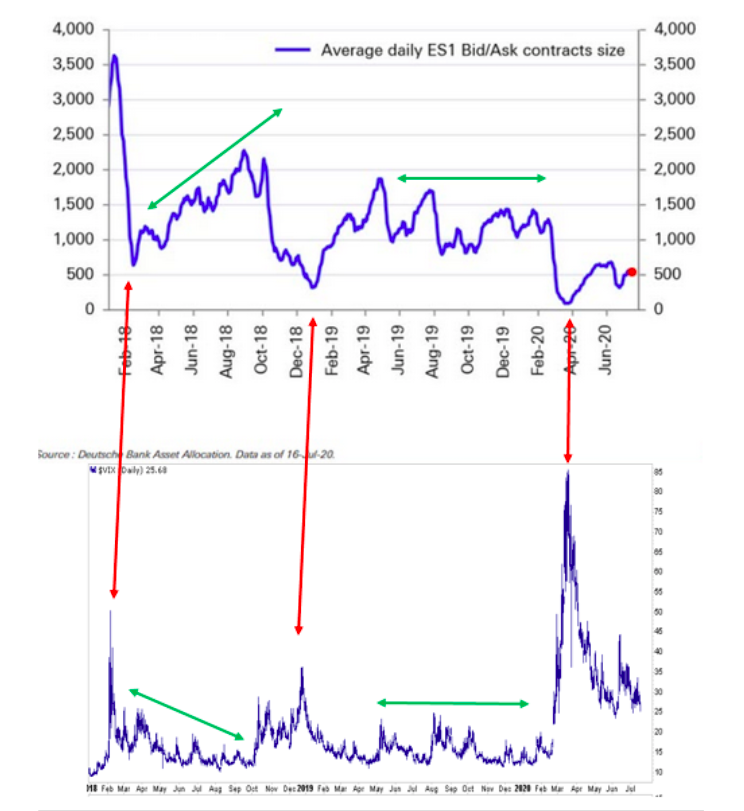

This dynamic is shown in the graph below comparing volatility to average bid/offer sizes.

From March through May, daily price changes were enormous. With no warning, major index prices would instantly gap higher or lower by a half a percent or more. At its peak, implied volatility, as shown above, reached 85. That compares to the range of 10-20 during most of 2019.

Volatility Tendencies – Fear of Loss

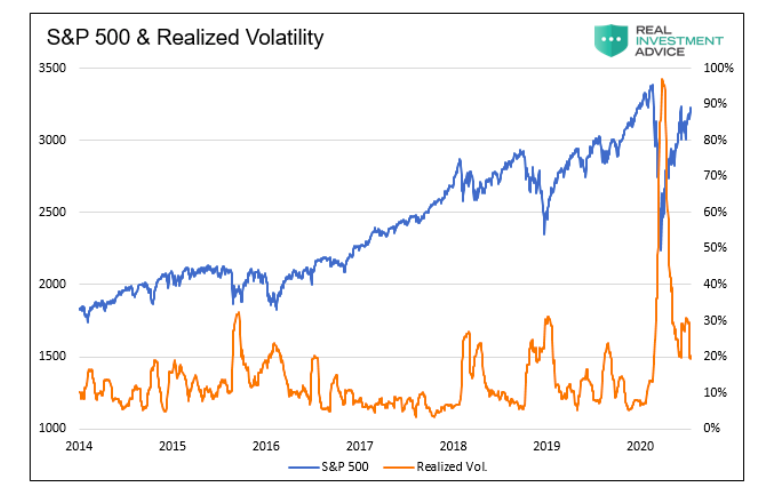

The graph below, similar to the one above, shows that volatility tends to remain low or fall in bull markets and rise quickly during drawdowns. Why is that?

To answer the question, just consider the following quote from Larry McCarthy- “Higher prices bring out buyers. Lower prices bring out sellers.” In behavioral terms, sellers tend to be more irrational than buyers. In practical terms, liquidity runs away when fear and uncertainty increase.

Fear has a more powerful short-term influence on markets than greed. Behavioral studies show investors make irrational decisions that favor protection over return. For instance, when asked to choose between receiving $90 or taking a 90% chance of winning $100, most people will avoid risk and take the $90. Mathematically, the expected outcome in both cases is $90, but most people choose to avoid the risk of getting nothing.

Fear, or risk of losing, is a greater impulsive driver of markets than greed. Greed takes time to develop. Fear develops suddenly and with little notice.

Summary

When investor confidence is high, liquidity is high, and volatility is typically low. Plenty of buyers and sellers willing to trade help assure orderly markets. However, when potential buyers become concerned about the risk of loss, liquidity fades. Buyers step away, sellers will take almost any price to protect against even steeper declines, and prices become more volatile. The suddenness of increased volatility and the false assumption of normally distributed prices leads to statistically impossible drawdowns.

Currently, volatility is two times pre-COVID levels. While sharply lower from March and April, liquidity remains problematic.

Volatility reminds us that the market structure is not stable. As a result, markets are more susceptible to sharp price changes. While most markets have been rising in recent months, the liquidity situation argues that bad news or a change in sentiment could result in substantial and nearly instantaneous losses.

Liquidity is poor, complacency is high, trade with caution.

Twitter: @michaellebowitz

Any opinions expressed herein are solely those of the author, and do not in any way represent the views or opinions of any other person or entity.

")