There was a time when a cattle rancher in need of new shoes had to find a shoemaker who wanted a cow. This was the barter system which clearly impeded trade and specialization of labor (that cattle farmer may have given up and decided to make his own shoe).

To ease trade, mediums of exchange gradually became prevalent. Initially these were livestock, skins, weapons, then rare items such as seashells then to coins that contained precious metals. Currency had to store wealth to grease the wheels of trade.

Coins gave way to notes (easier to carry), then to electronically stored currencies (no need to carry). We could keep going to virtual currencies, like bitcoin, but that is not where we are going today.

The benefit of a medium of exchange, aka currency, is it can be exchanged for anything that is for sale. That is the amazing thing about money, and it unleashed much greater economic efficiencies. $10 can be spent on lunch, a beer or two, candy, gas, shoe repair, etc. This is where the value of fiat currencies comes from, everyone’s is in agreement as to what it can be exchanged for.

Even though $10 is $10 is $10, and you would not sell your $10 for less than $10 nor would a rational buyer pay more than $10, our minds do not treat every $10 the same. Our minds account for money and other assets differently, depending on how we earned it, in what form the money is and how we bucket it. Mental Accounting is a behavioral concept that attempts to explain how our minds value different things, money or asset, and how this impacts our behavior.

Why are individuals more willing to gamble $10 if it is given to them vs. if they worked to earn it? Why do we spend more if paying with a credit card compared to paying cash? $10 is still $10, yet we value and treat it differently. Money is fungible, as it can be used for anything and shouldn’t have labels. Yet, due to mental accounting we are more likely to label money, making it less fungible.

Mental Accounting When Investing

How we treat investment capital is also impacted by mental accounting. A popular scenario is when investors take the winning proceeds on a trade and invest more aggressively with it, treating the gains as free money compared to money earned and saved. In the investor’s mind, they are investing with ‘house money’, causing you to put less emphasis on your personal return objectives and risk aversion. Yet, what really matters is the whole portfolio, not the profit or loss on an individual trade or bucket of money.

Mental Accounting & Company Spin-offs

Behavioral finance is a growing discipline, with more research published regularly as it gradually enters the mainstream of the investment world. As managers of Canada’s first behavioral finance-based fund, we leverage much of this research to find what we believe are instances in the market when behavioral biases cause investors to make mistakes and assets to be mispriced. For an active manager, a mispriced asset is an opportunity to profit. One of the strategies in the fund targets mental accounting during company spin-offs.

Occasionally, companies will spin-off a division or business line. The motivation varies from sometimes being required by regulators for competitive reasons or because the company wants to become more a pure play in their core industry. Spinning off a division that is not core is often rewarded in the market place. These spin-offs are often done by distributing shares in the spun-off companies to existing shareholders of the parent.

Mental account arises when an investor or portfolio manager who owns the parent company receives shares of the spin-off. Depending on the size of the spin-off relative to the parent, this distribution can often be viewed as free since you never explicitly paid for it.

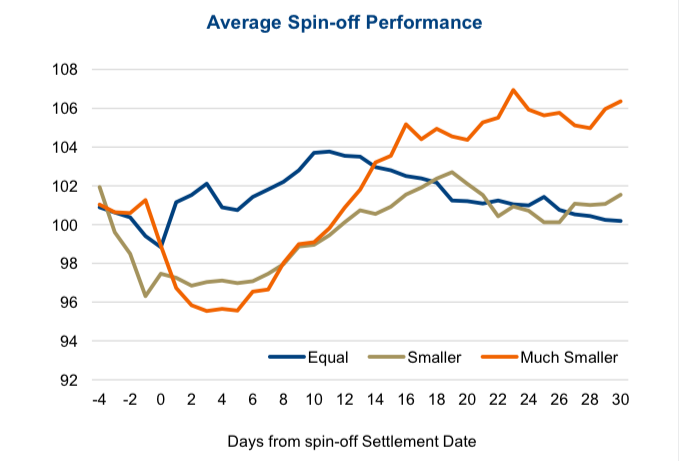

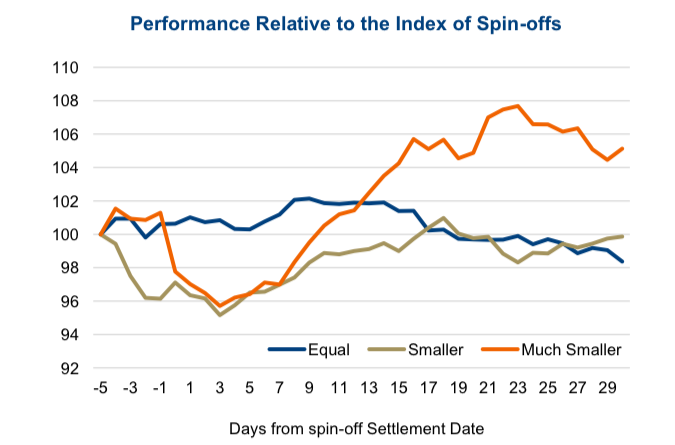

Our research found the way investors treat this spin-off was a function of the size of the spin-off relative to the parent company. Notably when the size of the spin- off position is materially smaller than the parent, it creates a perplexing problem for the investor. Suppose you own the parent company and its weight in your portfolio is 2%. They spin-off a division into your portfolio and it only has a weight of 0.3%. You now have a few choices. Keep in mind holding a 0.3% position will likely not have any material impact on your portfolio and you likely didn’t originally research much into this division given its size within the parent. You could complete due diligence on the spin-off and decide to build a larger meaningful position. Or, since you never really paid anything for it, just sell and move on. It seems many investors pick the latter path, which is also the easier one.

We analyzed spin-offs over the past seven years in the U.S. market and found if the spin-off was small relative to the parent, an interesting pattern emerged. Once the spin-off is complete, the shares typically see strong selling pressure on high volume. We assume this is due to investors simply blowing out their small position. After a number of days, this selling pressure and volumes often stabilizes, allowing the share price to recover. This creates an opportunity to buy during the weakness and wait for the shares to normalize.

This is a simplified description of our Neglect trading strategy that targets mental accounting. In reality, we incorporate several additional factors that we believe help improve the strategy’s risk/return characteristics. But at its core is this often- recurring pattern for spin-offs, weakness at first and then recovery. Equal, smaller and much smaller are the buckets for spin- offs as a function of the size of the spin-offs relative to the parent. This analysis covers the S&P 1500 over the past eight years.

We strongly believe behavioral biases can impact many investors during certain market situations, and this can create great investment opportunities.

Charts are sourced to Bloomberg unless otherwise noted.

Twitter: @sobata416 @ConnectedWealth

Any opinions expressed herein are solely those of the authors, and do not in any way represent the views or opinions of any other person or entity.