Citigroup’s Citi Surprise Index (CSI) is a real-time model, designed to analyze the accuracy of Wall Street’s economic forecasts. A positive index value indicates that recent economic data is stronger than the consensus of economists’ expectations. A negative reading denotes economic data which is worse than expectations.

Unbeknownst to most investors, the CSI also serves as a gauge of sentiment and provides unique insight into how well economists understand the current economic cycle.

Appreciation for the multitude of messages provided by the Citi Surprise Index allows investors to stay a step ahead of the economic models that Wall Street, and by default most investors, rely heavily on to forecast market levels and securities prices. This is more important than ever now as markets appear more concerned with economic data’s deviation from forecasts and less concerned with the absolute reading of the very same data and what it signifies for economic growth.

At 720 Global, our objective is to help investment professionals outperform and differentiate themselves in many ways. We believe offering unique and substantive analysis, such as this unique way to interpret the CSI, affords insights that go well beyond the obvious and superficial.

The Citi Surprise Index

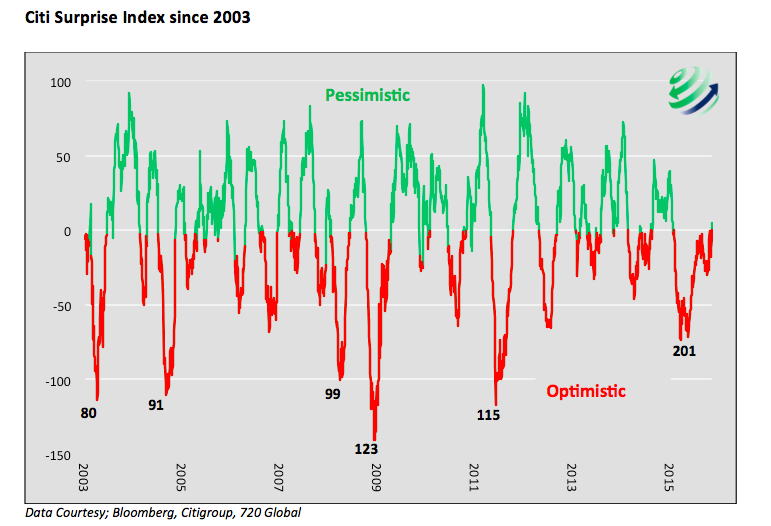

The graph below plots the CSI since 2003. Positive readings are in green and negative readings in red. Bear in mind that a positive reading means economists have underestimated economic data, thus the label “Pessimistic” in green at the top. Conversely, negative readings indicate economists have overestimated economic data, thus the label “Optimistic” at the bottom. The figures below selected points are the number of days the index was consecutively negative (more on that later). The simple takeaway from the chart of the Citi Surprise Index is that economists constantly shift between periods in which they are overly optimistic and overly pessimistic. This gyration is to be expected as economists notice errors in their forecasts and adjust their models to reflect the current environment.

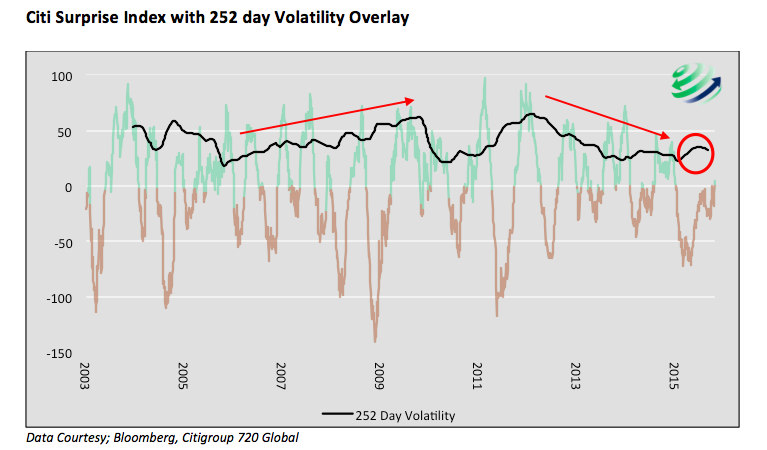

Interestingly, the adjustments to their models do not result in better forecasts as evidenced by the continual see-saw pattern of the index. The second graph further highlights this point by plotting the 1 year volatility (standard deviation) of the Citi Surprise Index. This graph illustrates the extent to which economists’ consensus forecasts deviate from the actual outcome without regard for direction. Since 2003, there are gradual ebbs and flows in the volatility of the index but not a clear sustainable downward trend, which would signal an improvement in forecasting skills.

720 Global considers 3 factors to make the most of understanding this data set.

The first factor is the duration of forecasting errors, or the amount of time the index is consecutively positive or negative. Said another way, it is the length of time that economists consistently over-estimate or under-estimate economic data. Longer periods of consistent over or under estimation are a warning that economists are slow to recognize the economy is accelerating or decelerating at a different pace than that of the prior months.

The second factor is the magnitude of errors, or how far the index is from zero. Readings significantly below or above zero indicate that consensus forecasts are missing by a wide margin. This alerts one to the magnitude in which economic trends are not being captured. More alarmingly though it can also signify that economists are tardy in their recognition of a change in the direction of the trend.

continue reading on the next page…

: Worrisome to Broader Market?")