Prices are still pretty high, but inflation appears to have continued to cool or decelerate in 2025. Will this trend continue in 2026, or will inflation become an issue once again?

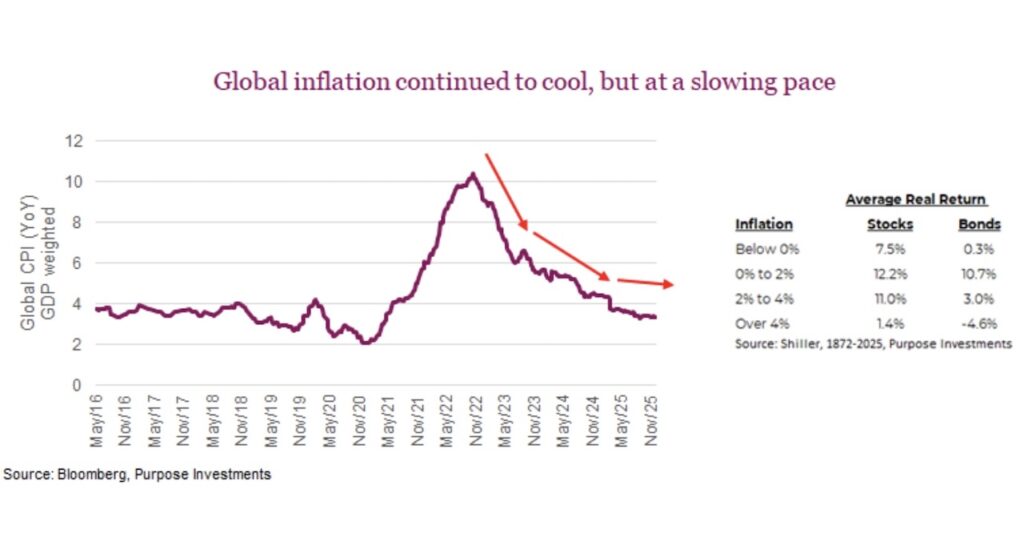

Inflation did continue to cool last year, as the World Economy Weighted Inflation dropped from 4.4% to 3.3%. Supply chain pressures are low, and wage growth and wage intentions have moderated substantially. Let’s not forget that oil prices in the $50/bbl range are a big help too.

And while money growth is creeping a bit higher globally, velocity is falling. That’s a long way to say the setup for an inflationary spike, similar to 2021/22, just isn’t there.

Inflation in the 2-4% range isn’t a bad thing; in fact, it’s sort of the sweet spot for equities, more so than bonds. Companies have pricing power and lots of top-line growth. It’s when inflation gets close to that 4% level that equity markets need to start to really worry.

Inflation may become an issue in 2026, but likely just in small pockets. The inflation spike that the global economy is still recovering from was driven by macro forces that were pervasive. It’s now more of a country-by-country issue. The U.S. is at higher risk given aggressive fiscal spending for a few years, some erosion of central bank independence, and an output gap that is positive (not a gap). The output gap measures the actual economic output compared to the estimated potential that would not be inflationary. The U.S. is running a little too hot. Germany, Japan, France, and Canada all have negative gaps, so if these economies accelerate, it shouldn’t be inflationary until the gap is closed.

Given that the U.S. is the most important inflation data point for markets, this is a risk in 2026. Fiscal spending, immigration policy, and tariffs are inflationary, as is the weaker US dollar. Technology, including AI, may prove disinflationary, but not today. Productivity gains are still a premonition; meanwhile, the data centre buildout is clearly inflationary. Just look at the price of memory or processors – it’s nuts. Low oil prices help, as does a softer labour market, but the risks are to the upside in 2026.

Inflation over the past four years has eroded purchasing power by over 20%. Thankfully, portfolio returns has more than kept up. Beyond the near term, should we be concerned about inflation as it pertains to long-term funding goals (a.k.a., a very comfortable retirement)?

Good point: inflation this year matters for markets, but over the longer term, inflation is a tax on the future you. We continue to believe that over the next five years or so, inflation will be higher than it was in the 2010s and much more volatile. Inflation in 2021/22 was a supply/demand shock, but secular factors have been gradually becoming more inflationary, or less disinflationary.

Here is our short take on them:

Globalization – Whether driven by tariffs or supply chain diversification, the trend in globalization has certainly slowed. This has likely moved from a disinflationary factor to an inflationary one.

Labour/Demographics – For many years, we have had more savers than borrowers, which puts downward pressure on yields and inflation. This balance is gradually softening, and with immigration restrictions, this pace may accelerate.

Policy – This differs from country to country. Erosion of central bank independence will soften the market impact of monetary policy, the main tool to fight inflation. This is a bigger risk for the U.S. and a few developing countries at the moment, less so for most other central banks. However, one commonality globally is the rise of fiscal spending with limited political consideration of deficits. The hawks are gone as more countries pivot to fiscal spending to help drive economic growth. We celebrate it from a growth perspective, but it will lift inflation.

Debt – Total debt is disinflationary, as it crowds out investment and consumes capital to maintain. And there’s a lot of debt out there.

Technology – Anything that improves productivity is disinflationary. Even with all the technology spend over the past 30 years, productivity growth has not accelerated, typically hovering around 1-2%. Maybe AI accelerates this. However, as we’ve pointed out, this is a down-the-road belief, as the use cases and instances expand to become meaningful. In the meantime, the unbridled capex spending on AI infrastructure is certainly inflationary. This will likely feed into more cyclicality of inflation.

To counter the risk of higher and more volatile inflation to your portfolio and financial plan, there are some options. Equities, especially those that pay dividends, are a good defence. Dividend growth, paid out of nominal earnings, has a long history of growing faster than inflation. Real asset exposure also helps. While we are short-term cautious on Canadian equities because of the great run they enjoyed in 2025, which have valuations a bit pressed, the TSX is an index rich in real asset exposure. It’s certainly worth consideration for combating the impact of inflation.

This report is authored by Craig Basinger, Chief Market Strategist at Purpose Investments Inc.

Sources: Charts are sourced to Bloomberg L.P., Purpose Investments Inc., and Richardson Wealth unless otherwise noted.

The author or his firm may hold positions in mentioned securities. Any opinions expressed herein are solely those of the authors, and do not in any way represent the views or opinions of any other person or entity.