The Federal Reserve announced in late October that there is a live possibility that they will raise rates in December. The very announcement of that initially caused bonds yields to spike (going from 1.98% on October 14th to 2.34% on Nov 10th) and caused losses for those that are heavily invested in USTs.

Traditionally, the Federal Reserve lowers interest rates to spur the economy and raises rates to slow it down. There was one jobs report in October that was very positive (and that seemed to spur the Fed on), but virtually all of the significant data released since then has shown economic weakness both here in the U.S. and abroad.

For instance, the UK recently announced that it is emerging from its troubles and stimulus is no longer needed. Then the UK Construction PMI was released showing a dramatic slowdown: dropped from 58.8 to 55.3. The UK has been stronger than other European countries but may just be the last to begin slowing.

It Is All About Economic Growth

If your underlying economy is growing, then people will more freely spend and invest in things like housing. The more people spend and invest the easier it is for companies to grow their sales and earnings and for the stock prices to go up. That’s not the situation we are in now.

Here is a list of current Purchasing Manufacturers Index (source: Hedgeye) numbers from around the globe (a number less than 50 represents contraction as opposed to expansion):

Purchasing Manager’s Index (PMI) Readings:

- U.S.: 48.9

- China: 49.6 (official) or 48.6 (Caixin)

- Brazil: 43.8

- Canada: 48.6

- Russia: 37.1

- South Africa: 47.5

- South Korea: 49.1

And here’s a look at earnings growth (according to Bloomberg data).

3Q Earnings Growth

- U.S. (SPX) = -4.6%

- Japan (Nikkei) = -9.5%

- U.K. (FTSE 100) = -30.5%

- China (Shanghai Comp) = -18.9%

- Brazil (Bovespa) = -42.7%

- Canada (TSX) = -32.4%

- Russia (MICEX) = -5.6%

So companies are purchasing less because of lower demand around the world. They are selling less and not making as much profit so their earnings are going down. It’s one thing for that to happen to a single company, it represents a trend when it begins to effect the majority of companies.

Result: Slowing economic growth here in the U.S. and globally. This is part of a longer-term trend and will likely take months to years to play out. I believe that the expansion that started in 2009 if coming to an end as all cycles do. This cycle has lasted longer than most, but it can’t go on forever.

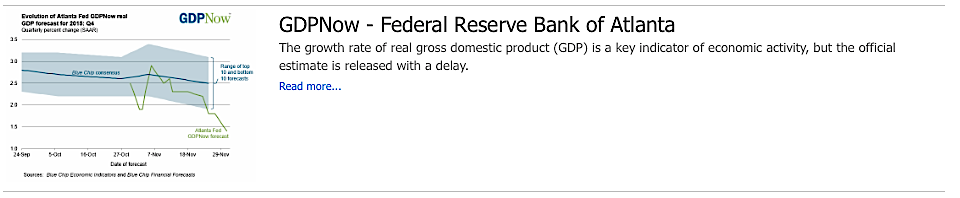

Even the Fed’s Predictive GDP Tracking Algorithm Agrees With This Assessment

The Atlanta Fed has a predictive tracking algorithm of current quarter US GDP. In early November it was predicting 2.8%, but that number has declined significantly as more data points came out. Just two weeks ago the Fed was predicting Q4 GDP of 2.2%. Now, post the ISM and PMI numbers, the prediction has dropped to 1.4. In other words, it has declined 50% in less than 5 weeks!

Still, it is very possible that the ‘data dependent’ Federal Reserve will raise rates at the December meeting. If it does, it won’t be because the data supports it. It could be because they are trying to salvage any vestige of credibility or it could be that they are trying to raise them so that they can lower them in a few months to try to arrest a slowing economy! This, frankly, is unbelievable that the most influential country in the world may be preparing for this.

To underscore the utter chaos regarding the Federal Reserve and its actions, the head of the Atlanta Fed Dennis Lockhart (a voting member) says there is “compelling evidence that the Fed should raise interest rates”. Note that Dennis Lockhart said that the same day that his banks’ GDPNow indicator dropped from 1.8% to 1.4%.

Business Insider: Fed’s Lockhart Says Rate Case Compelling

History shows how abnormal this course of action will be:

- The Federal Reserve hasn’t raised rates when ism < 50 in over 2 decades.

- The Federal Reserve hasn’t EVER raised rates when both ISM and PMI < 50 like they are now.

If they don’t raise interest rates, it may scare the markets because it is an admission of slowing growth. That could have a very negative impact on the stock market and drive yields lower in the bond market.

The bottom line is that, although I believe that they will end up not raising rates in December, there is no way to know for sure. The data doesn’t seem to matter anymore, though, so we don’t want to be caught by surprise. As a result, it is too risky to remain heavily invested in US Treasury bonds ahead of such a coin-toss event. Therefore, I used the recent drop in yields as an opportunity to lighten up on longer term US treasury bonds by selling roughly 1/3 of my positions in the iShares 20+ Year Treasury Bond ETF (TLT) and the Vanguard Extended Duration Treasury Bond ETF (EDV). I am not completely moving out of USTs because over the next 3 months, I believe the data will win out with bond traders and that US treasuries will outperform stocks by a considerable margin.

Thanks for reading.

Further reading from Jeff: Is The Fed Ready To Tempt Fate In December?

Twitter: @JeffVoudrie

Author holds various long positions in TLT and EDV at the time of publication. Any opinions expressed herein are solely those of the author, and do not in any way represent the views or opinions of any other person or entity.

Showing Bullish Buy Potential")