There is no denying economic activity is slowing but so far, the market has not cared much as it has taken a backseat to inflation angst. Slowing economic activity has also been masked by decent labor markets as service jobs are still being replenished from the pandemic-induced capacity reductions.

This is still one weird economy being influenced by the reverberations from the pandemic. The 2023 economic forecasts for the U.S. have evaporated to nearly zero, like Canada. The Eurozone and UK have seen their prospects for 2023 turn negative.

It has been our experience that when the consensus economists change forecasts to this degree, they are trying to catch up with reality. In other words, those lowered estimates are probably still too optimistic. This raises the question: Will we see a 2023 United States recession, shallow recession or no recession at all? Here are our thoughts, some are positive and some negative:

[ + ] Healthy Consumer – Much is said about the health of the consumer. Not so much the Canadian one, but the United States and European consumer has less debt and has saved over the pandemic years. Labor markets remain very healthy and wage growth is positive.

[ + ] It was always going to look like a recession – The pandemic-induced behaviours brought forward a lot of spending on durable goods at the expense of services. This helped supercharge the global economy, since buying an

iPad has a bigger economic impact than buying a pint of beer. As we ‘society’ came off this ‘goods’ buying high, and re- allocated to services, it was bound to manifest in a slowdown.

[ + ] Desynchronized economic activity – In 2008 and 2020, all economies went over the cliff at the same time. One was credit- driven, the other a pandemic. Today, economic growth is much more desynchronized. China slowed a lot in 2022 and may now be starting to improve as Covid policy is changed, along with some encouraging real estate signs. Europe is likely in a recession now, given inflation and a hit to energy. Canada may be in a recession in 2023, thanks to our overly sensitive economy to housing. The US may slow afterwards, but others may be on the mend by then. This desynchronized activity is good as it lessens the blow to markets.

[ + ] Xi pivot – There is much talk of a potential Fed pivot in 2023, which we really don’t see occurring unless something goes terribly wrong in the economy or markets. A Fed pause is likely the best scenario. China, on the other hand, has been experiencing a continued economic slowdown due to a real estate crisis (of sorts) and the zero Covid policy. On a positive note, it appears the zero Covid policy is being steadily dismantled. The path is still unknown, but economically speaking, this is good news. There are also some signs that the real estate pain may be starting to ease.

[ – ] Rate hikes / yields – It always seems the economy is slow to react … and then it suddenly does react. Higher interest rates impact consumers, business spending and the cost of capital. It is debatable how long the lag is between changes in rates and when it is felt in the economy, but if it is nine months, then only one of the seven Fed rate hikes has been felt so far. Oh, and that one was the small 25bps variety. The economy is about to really start to feel the rest.

[ – ] Wealth effect – The global bear market in equities and bonds has reduced total wealth by $139

trillion. That is $25 trillion from equities and $114 trillion from the global bond market. These global market capitalization measures are in US dollars, so let’s adjust for the rising USD and the damage is more reasonable at about $65 trillion (rough calculations now, fortunately when talking trillions, it doesn’t have to be exact). But global inflation last year based on the World Economy Weighted inflation index was 9.7%. Which means the world’s wealth, ignoring the market price performance, became almost 10% less valuable. Add that back in and we are about back to the $139 trillion in reduced real wealth. This drop will begin to weigh on the economic decisions of consumers and businesses.

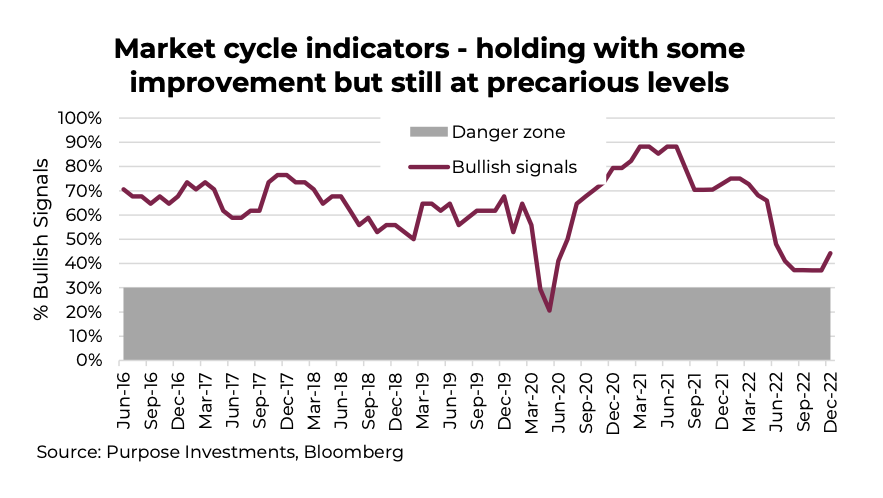

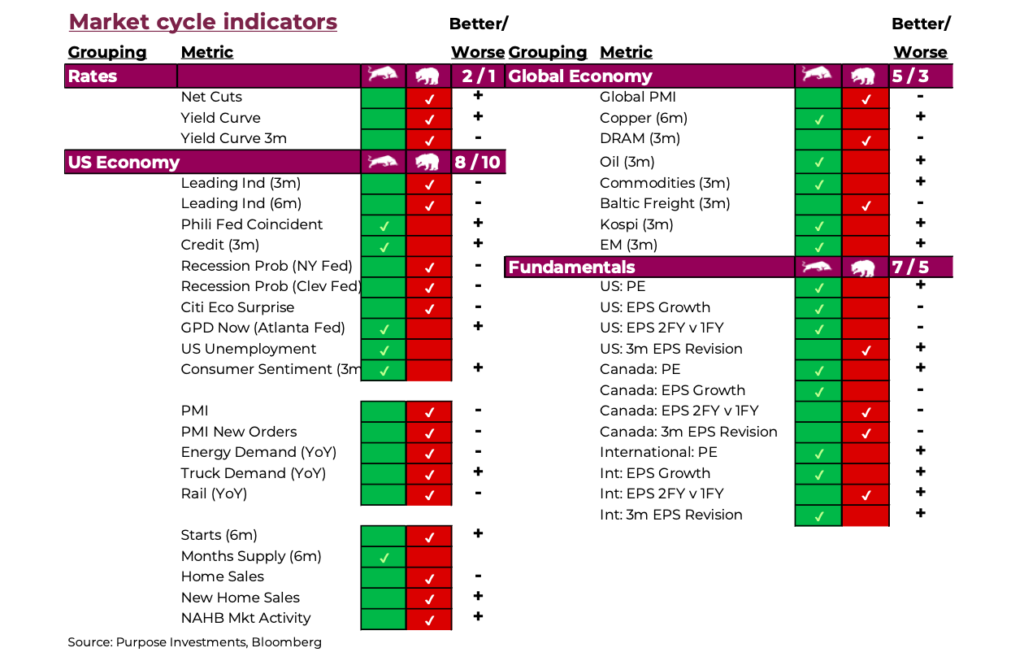

Source: Charts are sourced to Bloomberg L.P., Purpose Investments Inc., and Richardson Wealth unless otherwise noted.

Twitter: @ConnectedWealth

Any opinions expressed herein are solely those of the authors, and do not in any way represent the views or opinions of any other person or entity.

")

Trading Near Top Of Price Range")

")