The following outlook provides our investment thoughts for the coming year – 2018.

We did not include specific recommended asset allocation weightings for the major asset classes, as that offering is a part of our premium services. Nonetheless, the analysis and commentary below is in-depth and we hope will be of value to you.

Market Fundamentals

The confluence of improving synchronous economic global growth and hyper-inflating asset markets is urging central bankers to pause extraordinary policies and, in many cases, begin reversing them. While not obvious to most, monetary policy error has been in play since quantitative easing commenced in 2009, but the consequences will not appear until future central bank actions to raise interest rates and reduce their balance sheets affects commerce. The yield curve, credit spreads, and financial conditions can provide indications of when this may occur.

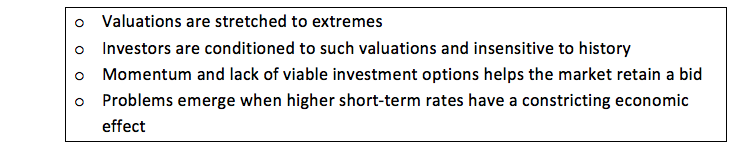

Market Fundamentals Commentary: Record highs in stocks, near-record lows in bond yields and historically tight credit spreads present significant challenges for investors. Economic data has improved, but many fundamental economic gauges remain soft relative to pre-crisis averages and inconsistent with asset price levels and valuations. Most investors do not seem at all concerned as money continues to move into risky asset classes, a classic sign of a bubble. While a defensive posture seems prudent, the technical picture remains supportive of further gains. One should respect the momentum behind these moves for the foreseeable future but be mindful that liquidity can evaporate quickly.

The primary investment theme remains “buy the dip.” That approach has worked amazingly well, a testament to the sustained strength of markets. Thanks in no small part to gradualism from the Fed on interest rate and balance sheet normalization, the blind assumption is that the favorable trajectory of risk assets can be endlessly extrapolated into the future.

There is a distinct difference between taking a defensive posture and a negative one. Remaining full-bore aggressively long at this juncture is a speculative endeavor akin to letting our kids play in the median of a busy highway. Proper care and stewardship of wealth means being protective and forward-looking to avoid large losses.

“The peer pressure and career risk of bolstering one’s defenses in a Pamplona-style bull run are palatable, but wealth is most effectively compounded by avoiding large losses not chasing returns with the irrationally exuberant. Many investors and others are stumbling confidently forward playing the role of the genius in a bull market. The prudent manager worries about the trifles of liquidity at a time when it is so plentiful it seems unreasonable to worry. Liquidity comes at a cost, but excess liquidity in times of crisis offers both priceless protection and clear-headed decision-making opportunities that are rare indeed.” – Liquidity Defined 12/14/2017, The Unseen

Outlier scenario – The market is far more sensitive to changes in interest rates than currently perceived. If the Fed continues to increase the Fed Funds rate and reduce their balance sheet in response to low unemployment and moderate levels of inflation, economic activity will decline. The result is a recession that initiates the unwinding of leverage accumulated in the system compounded by and revealing many layers of hidden risks.

Federal Reserve Outlook

The Fed gets new leadership early in the year in Jerome Powell, but he appears to be using the same playbook as Janet Yellen.

Federal Reserve Commentary: Given his time as a Fed board member and non-controversial positions on policy, Fed Chair nominee Jerome Powell should have no trouble being confirmed. He echoes many of Janet Yellen’s perspectives, and his demonstrated comportment is similar to that of the post-GFC era Chairmen. In the near-term, such a status quo transition is constructive for risk markets. However, the lengthy duration of the current economic cycle and the lofty valuations present when Powell assumes command make it hard to argue that the current environment is stable.

Outlier scenario – The inability of the Fed to effectively respond to a weaker economy due to elevated levels of inflation and/or a dramatically weaker U.S. dollar alters market expectations about the Fed “put” that has been in place for the past 30 years.

Bond Markets

Yield curve flatter as Fed interest rate hikes continue but inflation remains tame/below target

Bond Markets Commentary: U.S. Treasury yields are bi-polar. Short maturity yields are rising with Fed rate hikes while long-maturity yields are stable to lower. This dynamic produces a flattening of the yield curve revealing short-term optimism and long-term doubt. On an absolute basis, yields remain very low. The 2-year Treasury yield is 1.82% while the 10-year yield is 2.40%. The 2s-10s yield curve spread resides at the lowest level (0.58%) since the financial crisis of 2008.

Investors looking for income in the safety of the Treasury market will die of thirst long before achieving their targets. Accordingly, many investors are reaching for additional yield in riskier categories, namely high yield credit and dividend-paying stocks. This game has been going on for a long time. Despite the relative yield enhancement those alternatives offer, the question of whether or not an investor is appropriately rewarded for taking that risk still exists.

Non-investment grade or “junk” bond yields range from 4% to 10%, depending on the company and sector, with the overall average yield at about 5.75%. A bond is relegated to junk status precisely because of the elevated risk of default. At current market yields, junk bonds pose an inordinate threat of record low recovery value and terminal realized yield. Using the average yield for junk bonds of 5.75%, an average default rate of 5% and a generous recovery rate of 50%, a high yield debt portfolio is mathematically identical to a risk-free asset with a yield of 3.25%. That amounts to a risk-adjusted premium of only 0.85% over 10-year Treasuries (3.25 – 2.40). A yield pickup of less than 1% is hardly compelling, especially when one considers the downside from current valuation levels is immense.

Investors who think they get a nice yield boost from owning high yield debt are not considering the risk-adjusted outcomes. The risk-adjusted premium over Treasuries should be at least 200 to 300 basis points. Fixed income portfolio allocations should reside predominantly in the defensive havens of high-quality sovereign, well selected municipal and investment-grade corporate bonds. We recommend no allocation to junk.

Outlier scenario – Rising debt levels, inflation and global concerns over future monetary policy causes interest rates to rise as marginal buyers (Japan, China, Saudi Arabia, etc.) turn to sellers to reduce U.S. debt and U.S. dollar exposure. A disorderly rise in interest rates creates sudden distress and defaults in credit markets.

Stock markets

Markets remain supported as financial conditions are historically ultra-easy, despite the recent interest rate hikes

Stock Market Commentary: There are several measures used to justify current valuations, but they sound similar to those used in the dot-com Tech bubble. The relationships between valuation and fundamentals, on which cash flows are ultimately based, are grossly dislocated. Markets may well move higher, but to advocate a full allocation to equities under current circumstances ignores warnings of bubbles past. Stock market cap-to-GDP, price-to-sales, margin balances, cyclically-adjusted price-to-earnings ratios (CAPE), and others argue convincingly that the stock market is either near historic valuations or well through them. Owning well-selected, single-name companies because they are fundamentally cheap, not relatively cheap, makes sense. Otherwise, limiting general equity allocation exposures is prudent until reasonable opportunities return. We suggest setting stop losses and/or options strategies to help limit downside risk and retain any additional upside.

Outlier scenario – Realization and acknowledgment that valuations are high and concern over future returns sparks initial selling as the market begins to collapse under its own weight. This sets off a broad exodus out of risky assets for similar reasons.

continue reading on the next page…

: Showing Some Signs of Emerging Strength")