A lot of talk has surfaced lately about the record level of short interest in the market… And with it comes a lot of misconceptions.

This Summer Bloomberg published an article entitled “Short Sales Are at Their Highest Level Since the Financial Crisis”. Several more articles would follow highlighting the highest level of short selling since 2008.

Following these articles I have seen a lot of misguided comments on “short interest” that strike me as showing a clear misunderstanding of market dynamics and behavioral finance.

Note that this research post was actually written this past summer and published on Medium.com, but I believe it is still pertinent for investors.

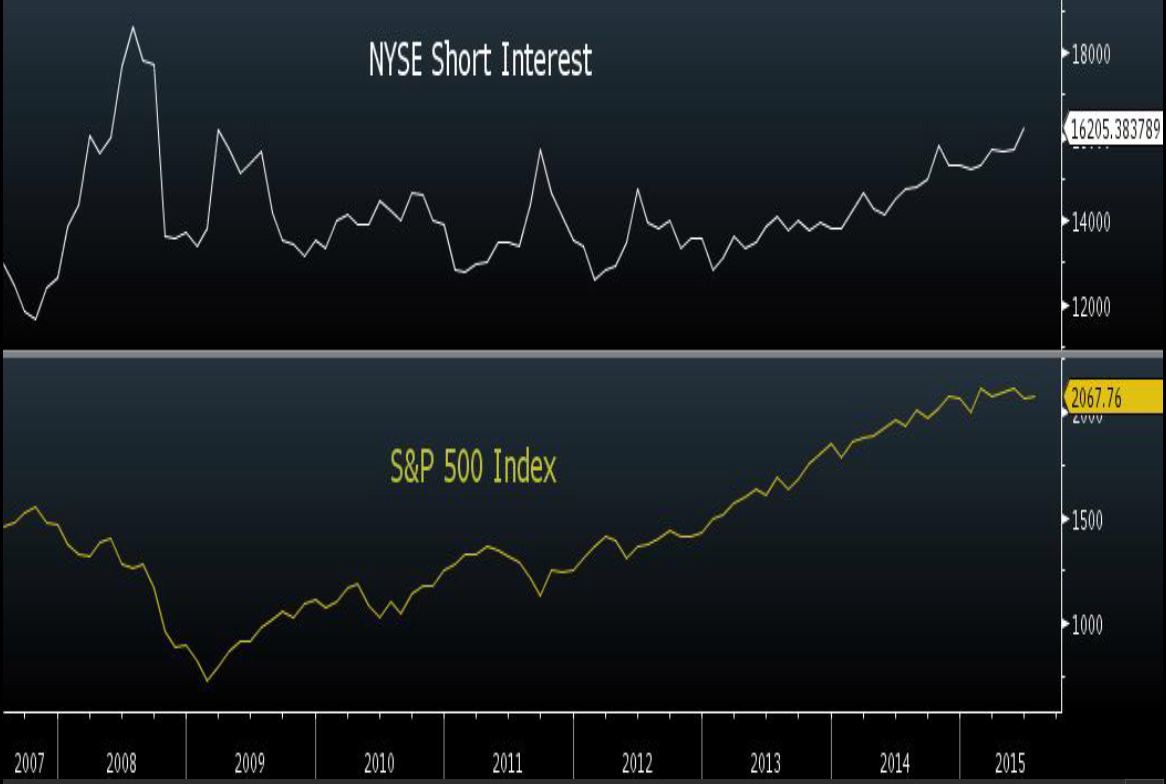

NYSE Short Interest vs S&P 500 CHART

A lot of these comments were portraying this news of a high level of short interest in the market as a positive “Best news for the market I have read this week.” “I love this chart”. Herein, I would like to dismiss this view.

The Short On Short Interest

If we look at individual stocks, a high or very high level of short interest is NOT a positive catalyst for a stock. A high level of short interest indicates that investors have a HIGH level of conviction that a stock is mispriced or that the underlying fundamentals of the business are deteriorating.

The vast majority of retail/individual investors do not engage in short selling and are generally more passive long holders of stocks via mutual funds and other vehicles like ETFs.

More often than not investors making short bets are sophisticated investors that spend a considerable amount of time and resources on researching their trades/investments before they decide to put them on. Does that mean they will be right? No it doesn’t, but often the research or thesis will be flawed and a lot of other market forces come in play to drive stock prices, but if we want to not be single result oriented and think in term of EV expected value, as a whole they will often be onto something.

Again, if a sophisticated investor puts down a large amount of money on the line betting that a stock is mispriced or a failing business, he often does so with an informed opinion.

Shorting is complicated, very risky and costly. It also comes with a cost of carry, so I will venture that it requires a much higher level of conviction than other types of bets than can be made in the market.

What About Short Squeeze’s?

Short interest does create a reservoir of buying power for a stock, as short positions will have to be covered at some point in most cases. A high short interest creates the potential for a “short squeeze”, but a “short squeeze” is just that, without a fundmental catalyst it will remain a mechanical event of short duration that will eventually be corrected. Some short-term traders can view a high short interest as a positive as they can try to ride a “short squeeze” move. Also a high short interest will often create a lot of volatility in a stock and exacerbate intra day moves, which is what you look for if you are a short-term trader.

But people that are lining up “high short interest” along with some other attributes of a stock as a catalyst for buying that stock are misguided.

continue reading on the next page…

: Creating Bullish Divergence?")

and Semiconductors (SMH): Concerning Price Pattern?")