China’s equity market and economy have been under pressure of late. Should we be concerned for the broader global markets and economy?

Let’s dive in, starting with the China stock market.

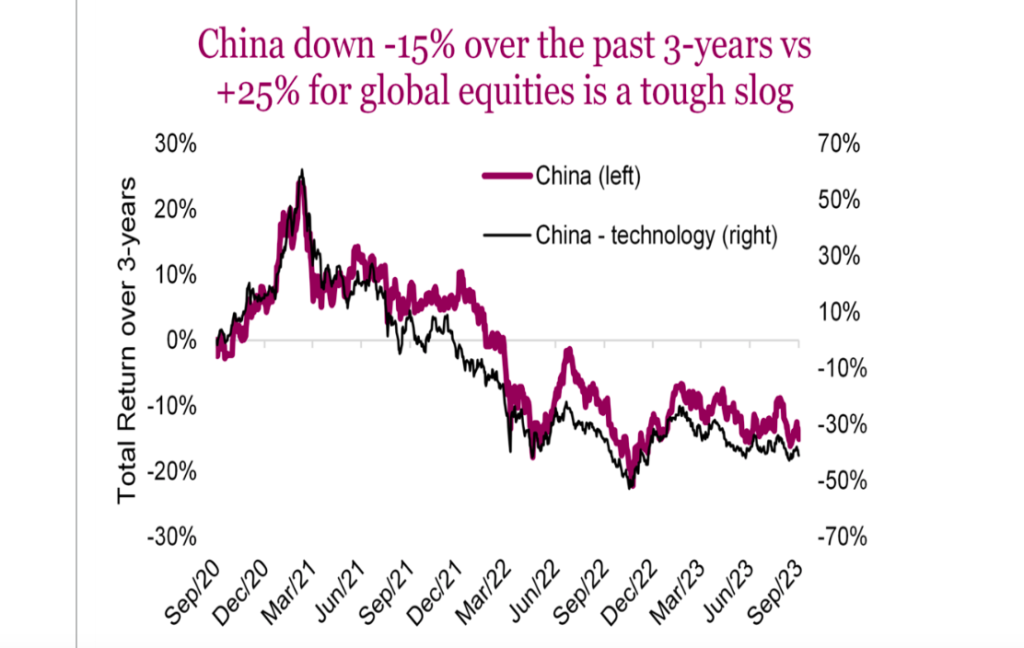

There’s no denying the Chinese stock market has had a tough go. Over the past 3 years, the Shanghai Shenzhen CSI 300 index is down about 15%. This compares to a period when global equities have risen 25%. And if you adjust to common currencies, it gets even a bit worse. China’s equity market has certainly endured some bad news over the past few years. Their housing industry is in a multi-year corrective phase, and Covid lockdowns didn’t help either. However, China’s market has something in common with the U.S. – as goes tech, so goes the market.

While Chinese technology companies certainly see bigger swings than the overall market, pretty much all the peaks and troughs line up (first chart). This means that if you are either bullish or bearish on China’s equity market, it is primarily a call on their technology companies. It is worth pointing out that Chinese tech companies suffered similarly to U.S. tech in 2021 and 2022. But U.S. tech rebounded HUGE this year while China tech failed. Semiconductor constraints and global investor risk appetites have probably led to much of this divergence. Given we are not bullish even on U.S. tech, it is even harder for us to get excited about China tech, which is more support for our low or near non-existent exposure to emerging markets.

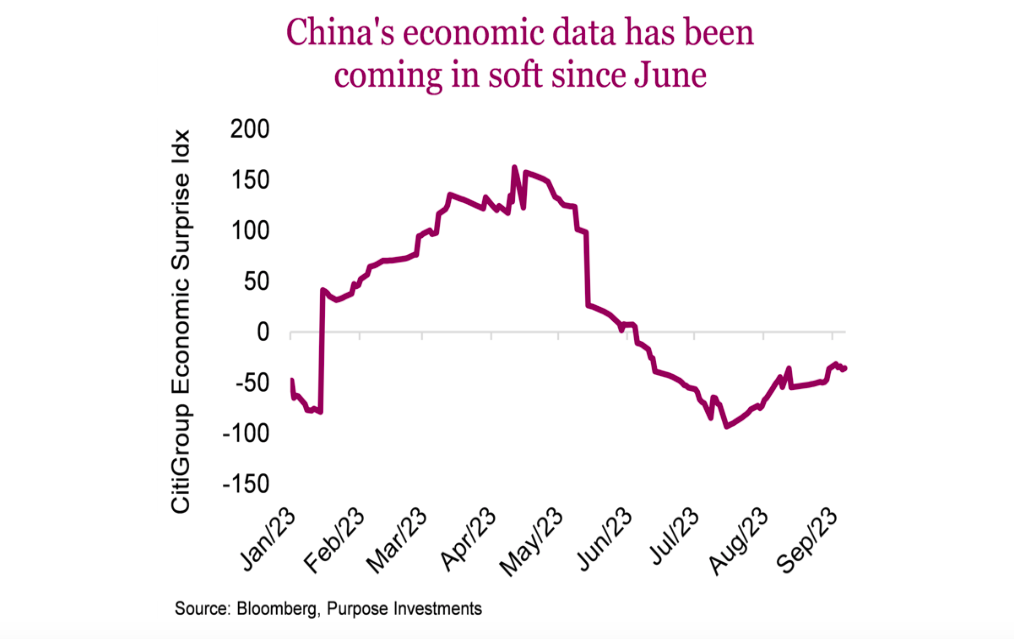

So, what about the economy? That matters much more, given the size of said economy and its impact on commodities, global manufacturing, trade, etc. Chinese economic data has been coming in soft, or below consensus expectations, all summer long, and this continues to feed concerns about the growth path of the world’s second-largest economy. Some of this should not be too surprising, given the global manufacturing industry does appear to be contracting to some degree. We can say this is a precursor to a broader economic slowdown, or we could attribute it to changing consumption away from goods back to services as pandemic behaviors get back to normal. Nonetheless, things are slowing in China. And compounding things is their real estate industry, which continues to languish. Real estate in China is as important as it is in Canada; as a percentage of GDP, it’s a heavyweight.

This is where things get a bit more challenging and divergent. You don’t need an economics degree to decipher that consumer-related activity is holding up OK in China; manufacturing is weak, and real estate is even weaker. The consumer has become more important for China’s economy over the past decade as the percentage in the middle-income bracket has risen. Encouraging on the surface, retail spending is up 7.3% so far this year compared to this point last year. That does sound incredibly strong, but this is being compared to Covid lockdown periods. So, it should be up nicely. Unfortunately, compared to dollar levels before the lockdowns, it’s pretty flat, which is not good. On a positive sign, Macau gambling revenues are rising, still well below pre-pandemic but certainly closing the gap quickly.

Real estate is not good. And a real estate crisis is a common byproduct of extended periods of economic advancement that lifts much of a population into the middle class or better. It happened in Japan, it happened in South Korea, and it happened in many of today’s developed economies if you look back far enough. This could be China’s turn. Many signs are there, from loose building standards to excess debt among developers, and leverage among consumers.

It is difficult to say how long this could last, and government stimulus/intervention is certainly evident. Our preferred index to watch is one we created two years ago that tracks the average price return of real estate developers listed in China and Hong Kong. The premise is straightforward: the stocks will turn ahead of any improving sign in the economic data or elsewhere. So far, there’s not much to be optimistic about. And yes, this index has lost over 60% of its value in a couple years.

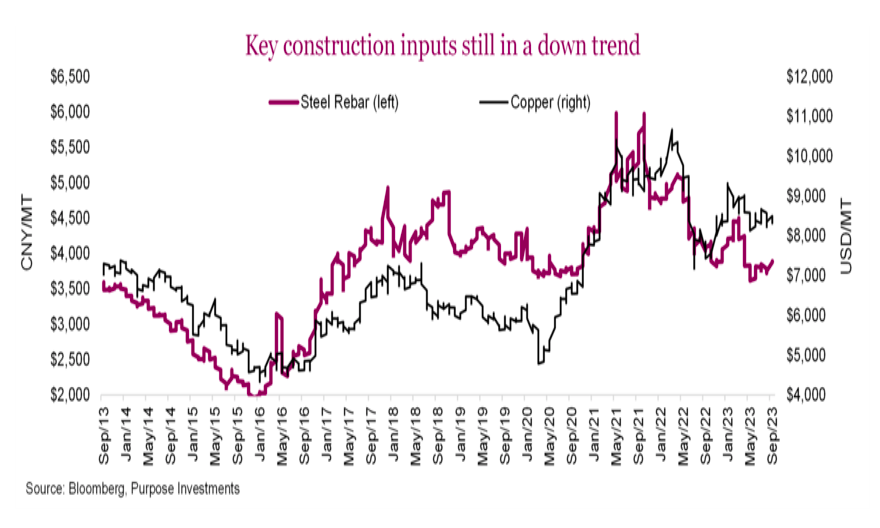

Real estate in China is important, but not because any of us are looking for a second home. It’s the knock-on effects of real estate and construction on the global economy. When China builds, whether homes or infrastructure, this has helped provide an economic boost that goes well beyond their borders. Looking at commodity prices of key building inputs, the trend has been lower but not aggressively. These too provide a signal for signs of further deterioration or improvement in China’s real estate market.

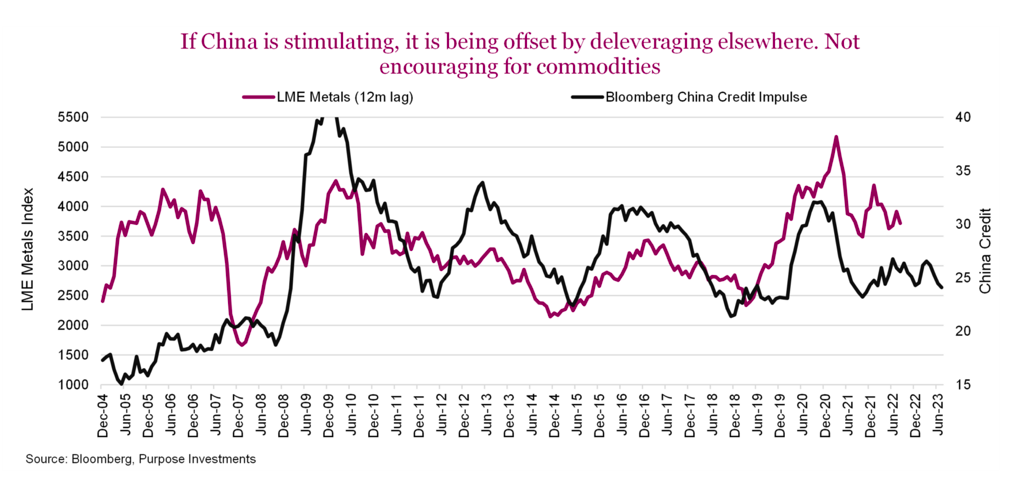

Overall, it’s not that encouraging. Historically, though, it has been government stimulus or changing of rules that has helped lift the economy out of a funk and, in many cases, helped out the global economy. Just look at the relationship between stimulus in China and the price of base metal commodities (copper, nickel, tin, lead, etc.), 12 months in the future. Stimulus would kick start projects, which would lead to planning and then purchasing of materials. And there has been some announced stimulus, but it seems elsewhere in the economy deleveraging is offsetting.

Of course, the stimulus taps could be turned on higher, or real estate could turn. But for now, the momentum is in the direction of slower economic growth. On a positive note, imports of coal and oil continue to be robust. This may be pointing to more decent economic activity, but not the kind that consumes tons of steel, copper and concrete. The TSX and the global economy prefer the latter kind of activity.

Final thoughts

Valuations in China’s equity market are low, and perhaps this mitigates the risks somewhat, but not enough for us. Currently we remain with a negative view on emerging markets and that certainly includes China. More importantly, it’s the economy. A slowing China, should it continue, will be yet another headwind for the global economy. And while the slowdown could be classified as ‘little’ at the moment, given the size of China’s economy and consumption, even a little trouble matters.

This report is authored by Craig Basinger, Chief Market Strategist at Purpose Investments Inc.

Source: Charts are sourced to Bloomberg L.P., Purpose Investments Inc., and Richardson Wealth unless otherwise noted.

Twitter: @ConnectedWealth

The author or his firm may hold positions in mentioned securities. Any opinions expressed herein are solely those of the authors, and do not in any way represent the views or opinions of any other person or entity.

: Showing Some Signs of Emerging Strength")