Big Picture:

One of the truths of markets is that we don’t get to choose the market environment. Investors want markets that go up all the time, traders usually want volatility, and premium sellers want implied volatility higher than realized volatility. Not all of those environments exist simultaneously and diversification helps us manage trading in different environments.

Even though it seems like trading another equity market shouldn’t have a huge impact on performance because of market correlation, the reality is that the results can be significant. To take diversification a step further, when we start adding additional strategies across various timeframes, it can really help smooth the equity curve.

One of the big issues with diversification is managing our emotions and holding true to a strategy or market that has been challenging to trade. It’s temping to look at your diversification, pick what has worked recently and reallocate equity. If we make that choice, we effectively remove the diversification that helped in the first place. Additionally, shifting strategies makes an assumption that what has happened recently will continue. In behavioral finance speak, we’re falling prey to recency bias. It’s important to keep in mind that what happened recently is not necessarily what will happen next. Sure, it might be . . . but it might not.

Diversification relies on the assumption that we don’t know the best choice for a given set of conditions or we don’t know with enough certainty. If we did know or had a structural advantage (think HFT, GS, or the Fed), there would be no need to diversify.

I will be the first to agree that pretty much any non-directional strategy in the Russell 2000 (RUT) has been challenging this year. That doesn’t mean that we should stop trading RUT or go on the endless hunt for some new trade. What we need to do is evaluate what’s been working, what hasn’t been working, why, and what it all means. It’s not always fun, but digging into the details of what we’re doing is where we find answers.

This week we had a healthy move up in the equity markets and my timing on the RUT July CIB was impeccably poor. At the same time, the trade size was small and there was no way to predict that move. Combined with several BWB trades at different maturities and in different underlyings, the impact of the poor entry timing was manageable. The point . . . diversification of strategies and markets works.

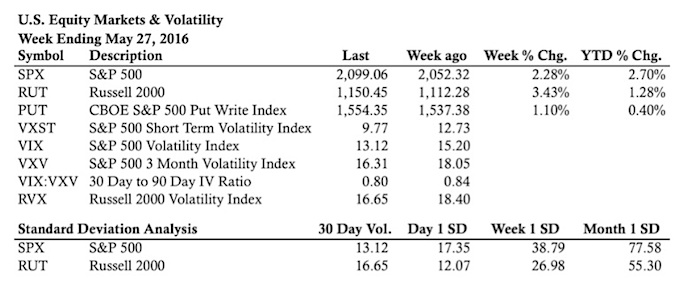

Volatility:

Volatility was hit hard this week and went into the weekend near the lows. Short term implied volatility fell more than longer term volatility in confirmation of market calm. The CBOE short term volatility index ($VXST) headed into the weekend at the lowest level since July 2015. In other words, the last time things were this calm was right before last August! (that’s sarcasm, not prediction)

The wide spread in implied to realized vol narrowed this week as implied fell and 20 day realized rose.

The VIX:VXV ratio dropped considerably this week.

Market Stats:

Thanks for reading and best to you in the week ahead.

Twitter: @ThetaTrend

The author holds positions in mentioned securities at the time of publication. Any opinions expressed herein are solely those of the author, and do not in any way represent the views or opinions of any other person or entity.

: Showing Some Signs of Emerging Strength")