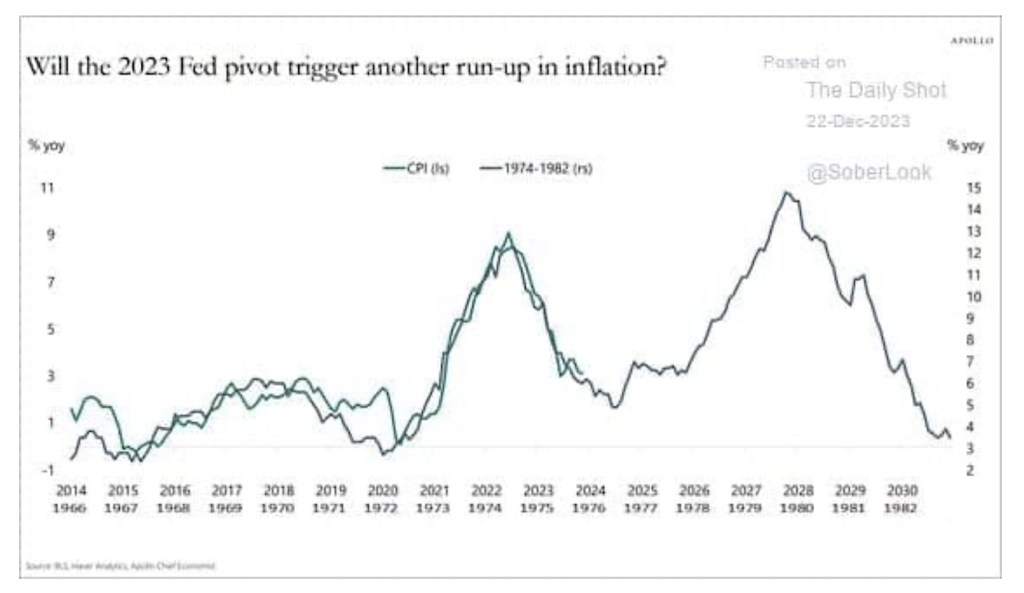

We wrote this four-part inflation series in response to the graph below, implying that prices are on the same inflation roller coaster ride as the 1970s.

If you have read the first three parts of this series (ONE, TWO, and THREE), you have a better appreciation for some similarities and differences between inflation of the last few years and that of the 1970s. With that wisdom, we share our opinion.

Desert Before Dinner

We always conclude articles with a summary. Given the gravity of inflation on investment returns, we think it is worth starting with our opinion and then providing details to support it.

We strongly believe the recent inflation outbreak was overwhelmingly the result of the pandemic and the governmental, Fed, corporate, and personal reactions to it. The virus and its economic effects were felt around the world, making matters even more impactful,

Unprecedented fiscal and monetary actions amplified the demand for goods and services well beyond norms. At the same time, the production of many goods was severely limited, and transportation lines were broken. Consequently, the supply of most goods and many services was severely constrained, and at the same time, demand was recovering rapidly.

Given such unique events, and barring an unforeseen calamity like the pandemic, another inflation surge is not likely.

The multiple bouts of inflation in the 1970s were not the result of one exceptional incident but many bad decisions. Furthermore, the Federal Reserve and government repeatedly, and unbeknownst to them, employed policies that increased prices for fifteen years. The Fed has learned many lessons since then, which instills confidence in our opinion. However, the government has little regard for them, which does pose a threat to our opinion.

As the pandemic-related stimulus slowly but surely exits the financial system and the economy and the supply lines fully heal, inflation will continue to fall back to or below the pre-pandemic average.

That said, the odds of another round of higher inflation are not zero, as we will elaborate.

That 70s Show

Before we start, it is worth reviewing a few snippets from That 70s Show, an article we wrote last December. The article discusses the economic environment of the 1970s and how it differs from today’s.

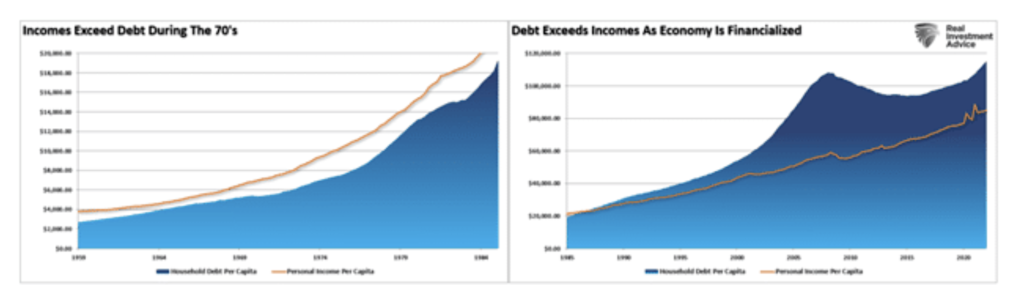

The first quote and graphs below show how the debt burden has changed over the last fifty years.

While the Fed is currently engaged “in the fight of its life,” trying to quell inflation, The economic differences are vastly different today. Due to the heavy debt burden, the economy requires lower interest rates to sustain even meager economic growth rates of 2%. Such levels were historically seen as “pre-recessionary,” but today, they are something economists hope to maintain.

Next, the mix of what the nation produces and consumes has reversed.

Such is a critical point. During “That 70s Show,” the economy was primarily manufacturing-based, providing a high multiplier effect on economic growth. Today, the mix has reversed, with services making up the bulk of economic activity. While services are essential, they have a very low multiplier effect on economic activity.

The Federal Reserve Has Learned From The 1970s

The Fed has often admitted it played a significant role in generating multiple waves of inflation in the 1970s. At the time, low unemployment was the primary goal. Such was a lingering relic from the Great Depression. Higher inflation in the name of lower unemployment was acceptable.

Furthermore, the Fed did not appreciate the potential for a price-wage spiral or changes in consumption patterns due to inflation and how they could affect employment.

The Fed’s tragic errors from the 1970s appear to haunt them today and provide instructive guidance.

Consumer Behaviors and Price-Wage Spirals

In August 2021, Jerome Powell stressed evidence that consumer behaviors change with inflation. Per Powell:

The 1970s saw two periods in which there were large increases in energy and food prices, raising headline inflation for a time. But when the direct effects on headline inflation eased, core inflation continued to run persistently higher than before. One likely contributing factor was that the public had come to generally expect higher inflation—one reason why we now monitor inflation expectations so carefully.

In February 2023, Powell made the following statement, assuring the public that the Fed was aware of the potential for a price wage spiral.

“If we continue to get, for example, strong labor market reports or higher and higher inflation reports, it may well be the case that we have to do more and raise hikes more than is priced in,”

Money Supply > Fed Funds

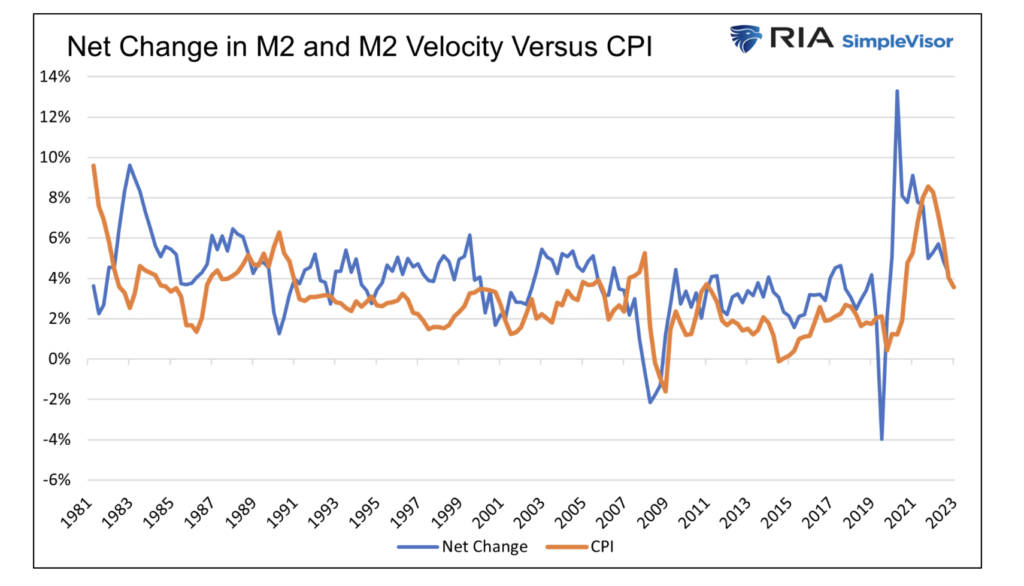

Even of greater significance, the Fed now realizes that the money supply is a crucial inflation component. However, equally important is money velocity, or the rate at which money is spent. The combination creates inflation or deflation.

The Fed is to fault for inflation. They allowed the money supply to proliferate as they kept doing QE and targeting a zero Fed Funds rate despite the velocity of money rebounding rapidly. The graph below shows how the money supply quickly grew while velocity accelerated and inflation ensued.

However, starting in 2022, the Fed turned extremely hawkish. Not only did they raise the Fed Funds rate to over 5% in two years, but they initiated QT. The result of their actions was not only to slow the growth of the money supply but also to cause it to contract.

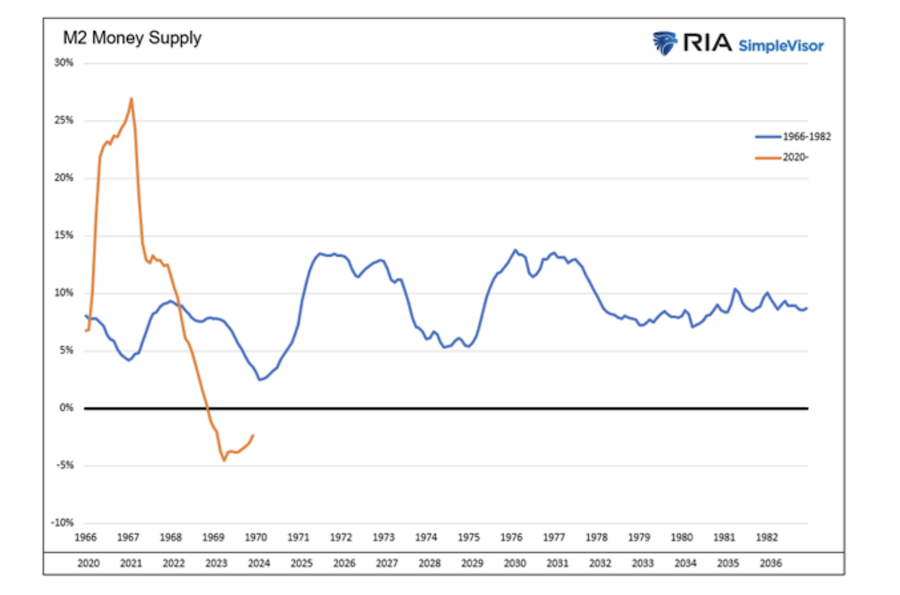

The graph below lines up the money supply from 1966 to 1982 with our recent period. In the 1970s, the Fed never allowed the money supply to shrink. They were singularly focused on the Fed Funds rate. The lesson learned from that day was that managing the money supply is a much more impactful tool on prices and economic activity than adjusting the Fed Funds rate. The last time the money supply contracted, as it is now, was during the Great Depression and World War 2.

The Fed and Jerome Powell were willing to endure a recession and higher unemployment to bring inflation back to its target. CBS News titled an article, “The Fed Plans To Sharply Boost Unemployment.” In it, Powell is quoted regarding unemployment: “I wish there were a painless way to do that,” Powell said. “There isn’t.”

Fed President Susan Collins offered, “I do anticipate that accomplishing price stability will require slower employment growth and a somewhat higher unemployment rate.”

However, The Government Seems To Beg For More Inflation

Unlike the Fed, the federal government did not learn its lessons from the 1970s. After the economy was well on its way to recovery, their reckless spending pushed the money supply higher than it would have been and created a tailwind for inflation. Recent deficits are well below those witnessed in 2020 and 2021 but are abnormally large, given such a robust economy.

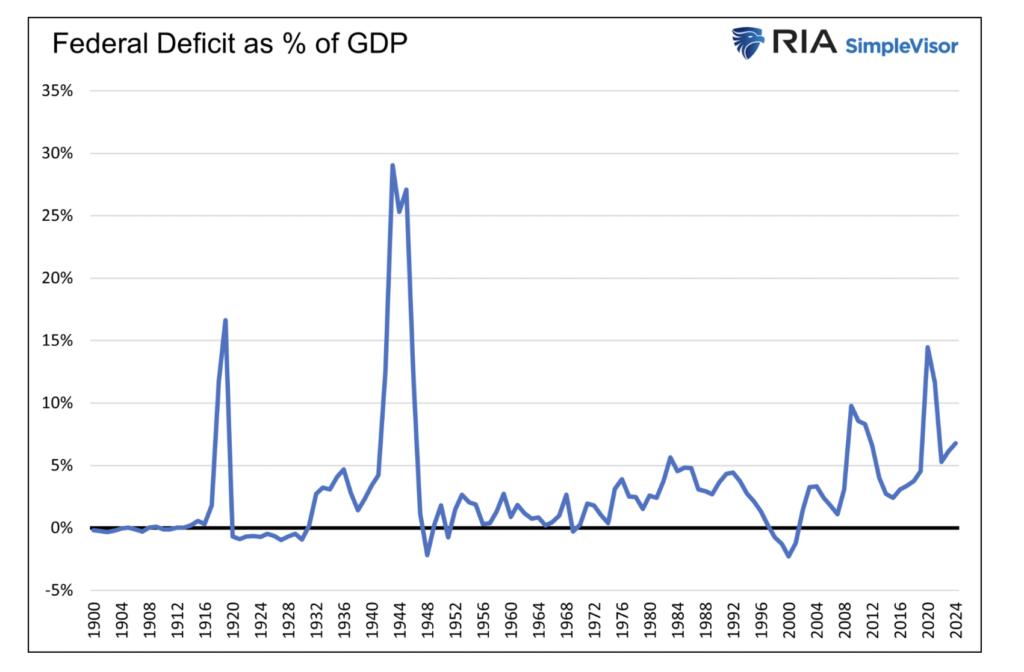

In the fiscal year 2023, the federal deficit was 5.7 percent of GDP. This year, the CBO estimates it will increase to 6.8 percent of GDP. The graph below shows the only other times the deficit, as a percentage of GDP, has been higher than today was during World War 1 and 2, the 2008 financial crisis, and a few years ago during the height of the pandemic. Those were emergencies.

Supply Side Factors

One of the significant factors behind recent inflation was the unprecedented global shuttering of the economy. The limited supply of goods and handicapped transportation systems grossly restricted the amount of goods on the market.

While production problems still exist, they have primarily normalized. In the 1970s, the government unknowingly incentivized goods shortages via wage and price control measures. Lacking the ability to raise prices to reflect the increasing costs of their inputs, some companies had no choice but to limit or halt production and curtail supply. Today, the government is not taking action to stop or restrict the production or transportation of goods.

The gross distortions to the supply side of the inflation equation were solely related to the pandemic and should not be forecasted to return in such an impactful way.

Everything Else

We now run through a litany of other contributors to inflation.

Oil Shock

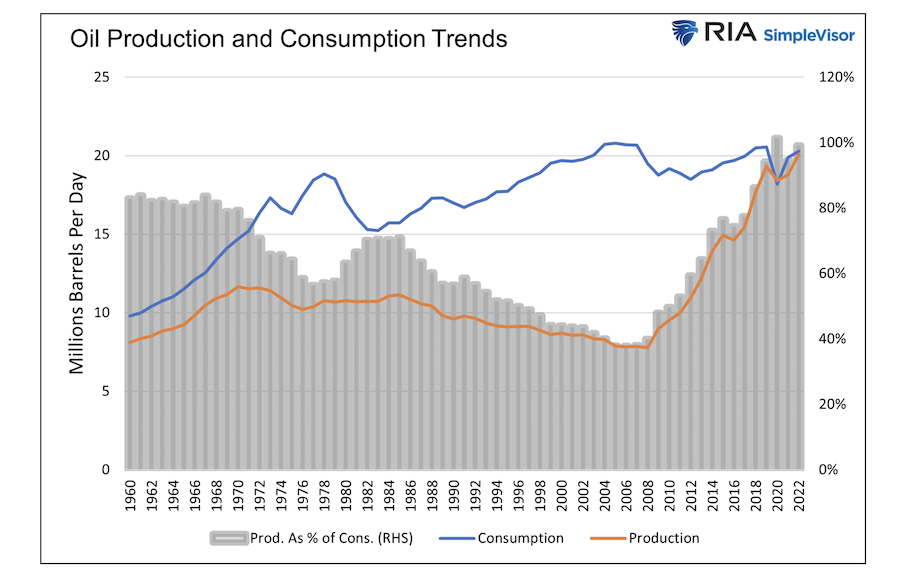

Our dependency on foreign oil has declined substantially, as shown below. Before 2008, the U.S. depended on imports for about half of its oil needs. Since the abundance of shale oil, we have become energy-independent.

While the situations in the Middle East and Russia may escalate, an embargo like that of fifty years will be much less damaging. However, short term price spurts can happen as oil prices are based on global factors.

The Unions Lose Power

Throughout 2022, Jerome Powell incessantly fretted about the potential for a price wage spiral. Recent union negotiations with the automakers, Hollywood writers and actors, FedEx, and other companies fueled concerns of a price wage spiral.

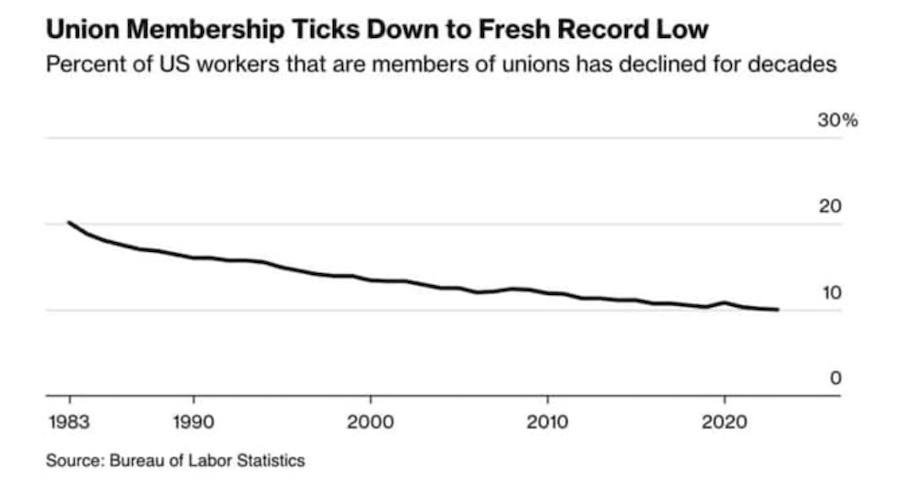

Regarding the potential for a price wage spiral, we must consider that in the 1970s, unions carried much more bargaining power, and one out of every five workers was a union member. The graph below from Bloomberg shows that union membership has consistently decreased since. It now stands at only 10% of workers, limiting the potential for unions to drive wages higher for the entire workforce.

Further new technologies, off-shoring jobs, and the ability to hire remote workers are also helping keep a lid on wages.

Economic Landscape

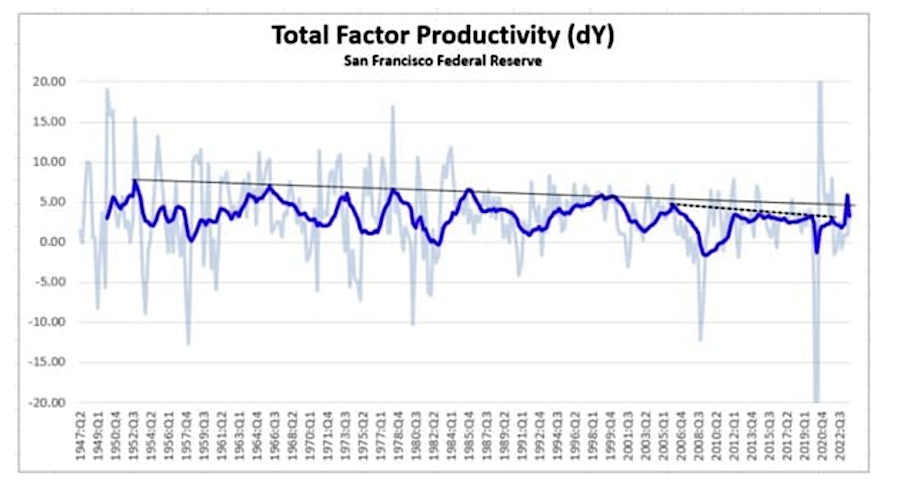

Today’s economic landscape, including debt load, demographics, and productivity growth, differs from the 1970s. The Fed projects the nation’s long-term economic growth rate at 1.85%. Such lines up with slowing productivity growth, as shown below.

From 1960 to 1985, real GDP averaged 3.7%, more than double the current trend growth. In the 1970s, the population grew by over 1% annually. Today, that number is half a percent and is expected to decline steadily.

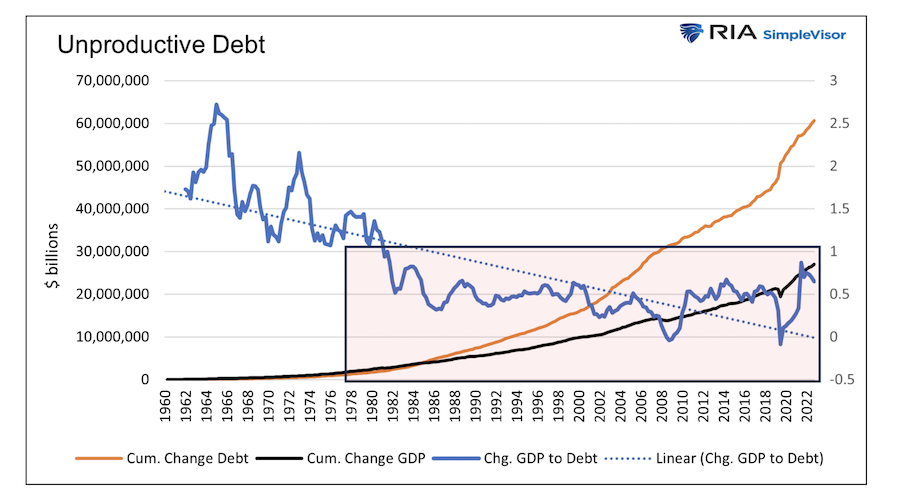

Also, of incredible importance, debt was not a considerable headwind to growth 50 years ago. Since then, debt has grown four times faster than GDP, as shown below. Given our heavy dependence on debt and, therefore, low-interest rates, the economy’s ability to tolerate higher inflation is much less than in the ’70s.

Fiscal dominance, whereby the Fed must set monetary policy to keep the government solvent, is now necessary. Given the economic and demographic trends noted above and the ever-increasing debt, it’s hard to imagine that the Fed will tolerate above-trend inflation or higher interest rates for sustained periods.

Fiscally fueled demand has been a crucial driver of inflation over the past few years. However, if demand factors, as noted above, resume pre-pandemic trends, GDP will slow, and significant demand-driven price increases are not likely.

Lastly, the government has a negative debt multiplier. Each dollar of debt eventually takes away from economic growth. As recent deficit spending turns from stimulus to headwinds, economic growth will continue to trend lower. With it, inflation will follow.

What Might Change Our Opinion?

The Treasury and Fed introduced a new recession-fighting playbook in 2020. The combination of direct checks and benefits to the public alongside grossly easy monetary policy played a significant role in fueling inflation.

If that playbook becomes the rule and not an exception, we could see periods of higher than trend inflation. But even with such a fiscal reply to a recession, supply line problems will not be the problem they were a few years ago. Given the unlikelihood that the global economy will shut down again, higher inflation due to fiscal and monetary negligence is possible, but not at the levels we witnessed in 2021 and 2022.

Summary

At its core, inflation is too much money chasing too few goods. That was the case in 2020 through 2022. This is not the case anymore.

The 2020s aren’t the 1970s by any stretch of the imagination! While the lead graph from Apollo may show recent inflation trends align well with those of the 1970s, we think it is grossly misleading.

Twitter: @michaellebowitz

The author or his firm may have positions in mentioned securities at the time of publication. Any opinions expressed herein are solely those of the author, and do not in any way represent the views or opinions of any other person or entity.