To paraphrase Warren Buffett, by most accounts the 5 year tide of the Federal Reserve’s grand experiment in monetary accommodation is about to start going out – now we’ll see if markets (and Fed policymakers, so don’t go into this with a full stomach) have been swimming naked.

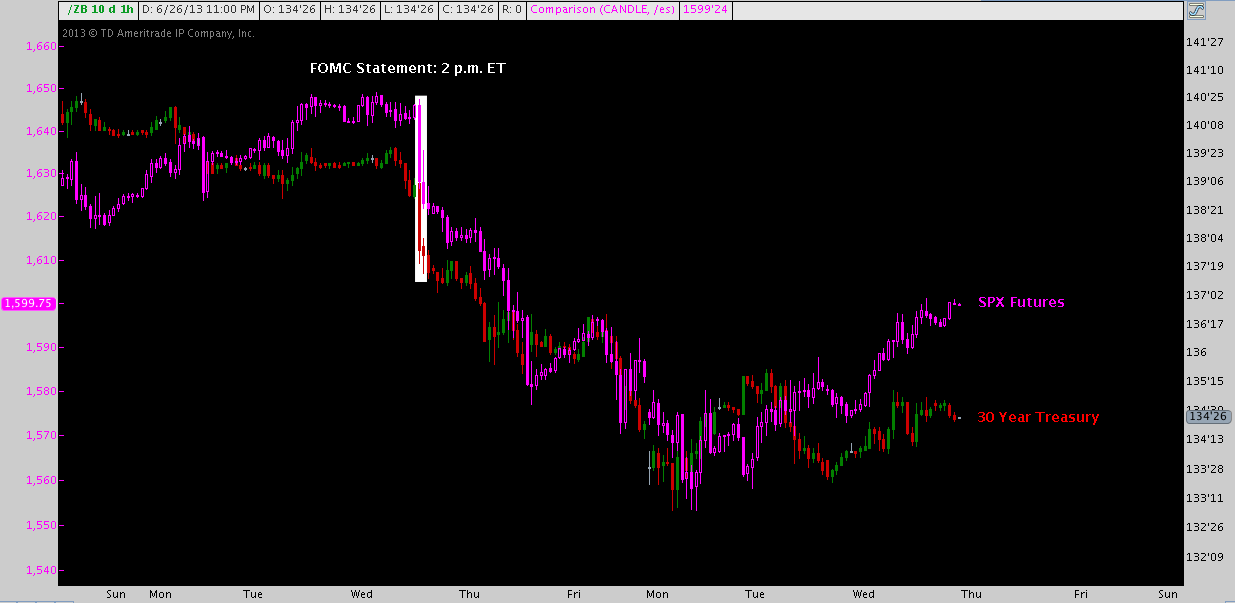

Take a look at the performance of the S&P 500 (SPX) or the 30-year US Treasury bond (symbol: ZB) over the past 6 market days. Rightly or wrongly, last week’s FOMC statement and accompanying press conference are being construed as the cresting moment that splits the flow and ebb of the era of LSAP (Large-Scale Asset Purchases).

Treasuries actually began their correction much earlier. USTs have been falling with little reprieve since the previous FOMC meeting concluded on May 1, where the Fed began disseminating its “taper” message in earnest, typified by Bernanke’s May 22 concession “In the next few meetings, [the FOMC] could take a step down in [its] pace of purchases,” before Congress’s Joint Economic Committee. A little late to the Red Wedding but not to be outdone, stocks have corrected 7.5% peak-to-trough since hitting their all-time high that same day.

These last 5 years of singular reliance on central bank largesse have inculcated a powerful lesson: grasp of the prevailing macro narrative is an unyielding rule of market survival. Even though stocks are only negligibly off all-time highs and the specter of a tighter Fed policy has loomed patiently waiting its turn for 5 years, the sudden yearning to answer “Why is this happening?” once again burns unabated across every market segment. Where there’s a need, a market grows up to satisfy it; and there’s no shortage of voices attempting to inform, with timeworn Fed platitudes and superficially plausible guidance everywhere. So it’s more than a little disconcerting when the FOMC makes the admission – as Bernanke relayed at last Wednesday’s press conference – that it doesn’t quite know what’s going on.

In the past week everyone who cares has had a crack at all the questions one would expect to hear about the FOMC’s apparently hawkish turn. As usual, there’s a lot we don’t know.

- What changed between their May 1 and Jun 19 statements to substantially brighten the Fed’s economic assessment?

- What will ultimately trigger tapering of the Fed’s asset purchases?

- What could cause Fed policy to regress back into an easing cycle?

- When will rates begin rising?

- Will Fed policy mandate sale of Treasury and/or MBS inventories; or will it let issues mature on-balance sheet? Both?

- Who’s dovish and hawkish with the QE endgame now visible to the naked eye on the horizon?

- Who will the next Fed Chair be and how might they alter course?

- When has the FOMC – individually or collectively – made an economic forecast that was even vaguely corroborated by subsequent developments?

In an effort to fill in the explanatory gap always left in the Fed’s cryptic wake, it’s safe to say the wider journo-analytical community has exhausted the speculative potential of this list. More’s the pity, then, that these questions go nowhere, though they’re posed anew every 6 weeks.

But then there are incisive answers we can’t do without to questions we didn’t know we had, graciously provided by the likes of WSJ Fed propagandist reporter Jon Hilsenrath who ex post facto condescended after 2 days of post-FOMC market mayhem on last Friday to affirm, “yes: the market completely missed the Fed’s dovishness”. Is the lockstep “supportive of asset prices” for so long finally broken?

Other prominent observers have noted this emerging market-FOMC messaging disjunction, but seem to attribute fault more so to the Fed. According to Fed President and noted policy hawk Jeffrey Lacker today, “it has been a rocky period over the last couple of months for communication from the Fed”, further noting “We had to solve a new communications puzzle for ourselves this time”.

Similarly, IMF Chief Economist Olivier Blanchard opined yesterday: “Conceptually it (QE exit) is not fundamentally very difficult, but there is a problem of communication on how you do it”. Of course, convincing communication is a challenge when “The Fed has no clue what will happen when it starts selling assets”.

These points raise a line of inquiry that I think is far more worthy of our interest as managers of risk for whom wondering the prudence of attributing an 11% probability to a 25bps bump up in the discount rate at the April 2015 meeting makes no whit of difference. Not out of a perverse desire to see it fail but to recognize and act preemptively if it does: how can the all-too-fallible Fed go wrong?

- What’s this “problem” or “puzzle” of “communication”? How crucial is communication to the success of Fed policy?

- Why does the Fed think it’s policies have been and will continue to be effective? Is it right about the past or future?

- From the context of Bernanke’s press conference last week: What does the FOMC not know? Should it?

- What implications do the Fed’s forward guidance missteps (or market’s misapprehension of them) have for its credibility?

- Does the Fed policy have a built-in theoretical blind spot that has been benign but may now complicate its exit from QE?

“Creature from Jekyll Island” this is not; nor am I concerned with building an argument supporting Fed iconoclasm. Each of these questions have all been asked before in some form or fashion; but only as the (in)efficacy of post-crisis Fed policy is laid bare will their answers finally begin to take shape. In the next installment on Fed policy, we’ll consider these questions in the breaking context of the Taper era.

Twitter: @andrewunknown and @seeitmarket

Author holds no position in the securities or instruments mentioned at the time of publication.

Beastie Boys “Ill Communication” album cover art copyright Capitol Records

Any opinions expressed herein are solely those of the author, and do not in any way represent the views or opinions of any other person or entity.

{kind=link}