The equity markets rallied last week as investors looked past the financial and currency turmoil in Turkey, seeing the S&P 500 (NYSEARCA: SPY). Instead, investors focused on the renewed trade talks between the U.S. and China and the strong second-quarter earnings reports and positive economic news.

The Conference Board’s Leading Economic Index (LEI) soared 0.6% in July, the most in five months.

The year-over-year change of the LEI, which is comprised of 10 economic components whose changes tend to precede changes in the overall economy, climbed to 6.3%, the fastest pace in four years. Nine of the ten indicators within the report were positive indicating that the outlook for the economy remains broadly positive.

Despite some positive economic news, there is little room for complacency and some evidence that stocks will remain in a trading range as we move deeper into the third quarter. The Reuters/University of Michigan Consumer Sentiment Index preliminary survey for August shows the lowest reading in nearly a year. The survey showed consumers remained positive on current conditions but less confident about the future economic conditions. Additionally, inflation pressures are building that have ramifications for consumer spending and Federal Reserve monetary policy.

The Federal Reserve is widely anticipated to raise rates in September. Another rate increase in December would mark the ninth hike in a row and could provide a headwind for the economy.

The fact that housing starts and building permits are below what they were a year ago suggests that higher interest rates are already taking a toll on important sectors of the economy.

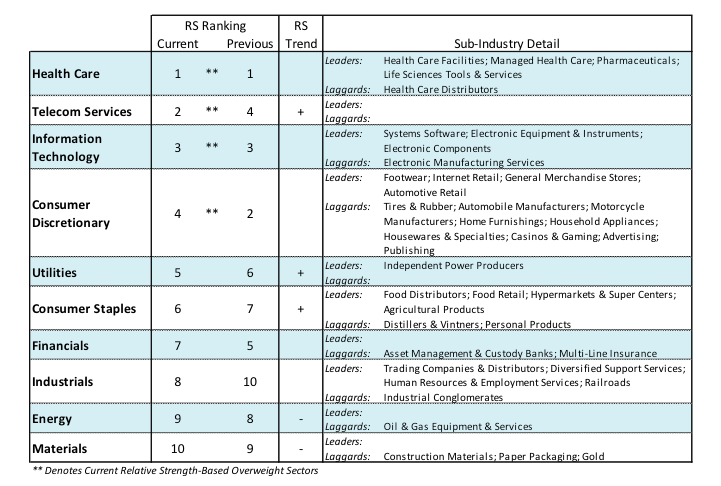

This held true again last week as the rally was led by consumer staples and utilities that climbed more than 3.00% and health care that climbed 2.50%. Defensive sectors continue to gain in terms of relative strength. We recommend diversifying into these areas of the market as we move deeper into the third quarter.

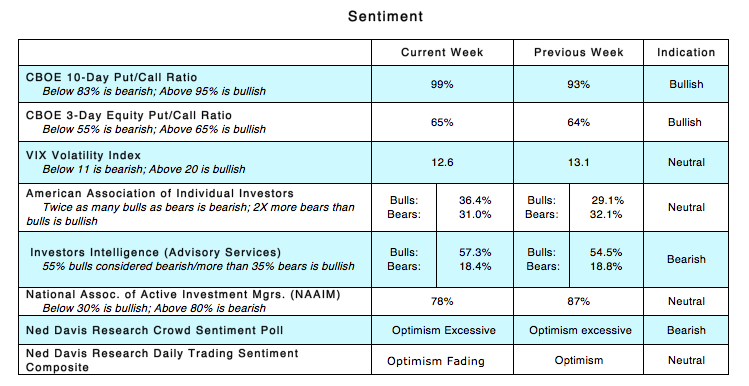

The technical indicators including investor sentiment and stock market breadth are mixed. Put/call ratios have been moving higher as options traders have been aggressively buying downside protection. The fact that often-wrong options traders are looking down is considered a positive using contrary opinion.

Offsetting this, however, is the growing optimism among the advisory services. The latest Investors Intelligence (II) data shows advisory service bulls moving to their highest level since early February suggesting too many are bullish. The conflicting sentiment data is expressed in the widely followed Ned Davis Daily Trading Sentiment Composite, representing a wide range of indicators of investor psychology, which is sitting at dead neutral. Stock market breadth remains problematic.

Despite the gains in averages last week, fewer issues hit new 52-week highs but a growing number of stocks reached new 52-week lows. Additionally, despite the run back toward the January highs, the percentage of stocks trading above their 50-day moving averages remains below the June peak. The fact that half of this year’s gain in the S&P 500 Index is attributable to just three stocks provides testament to the fact that the advance has been narrow and dependent on the technology sector for traction.

Twitter: @WillieDelwiche

Any opinions expressed herein are solely those of the author, and do not in any way represent the views or opinions of any other person or entity.