How things can change with a new week. After struggling last week and posting losses, the major US stock market averages are off to the races this week. The S&P 500 Index (INDEXSP:.INX) closed up over 1 percent on Monday.

Of interest are the 10 Year Treasury Note Yield (INDEXCBOE:TNX) and US Dollar Index (CURRENCY:USD). Both closed lower last week… The 10 year note yield closed at a new low for 2017 (2.06%), while the US Dollar Index finished the week at its lowest level since 2014.

But both of them are bouncing along with U.S. equities to start the week.

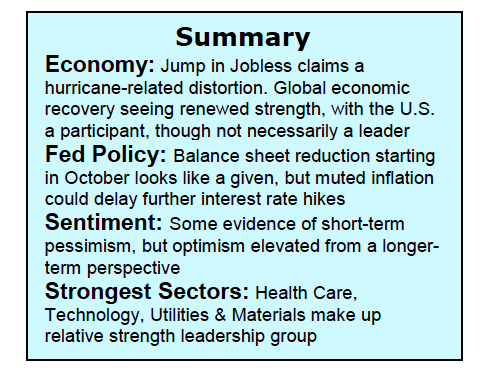

The Federal Reserve in focus… The focus of the next FOMC meeting (September 19-20) is likely to be the beginning of the process of drawing down the Federal Reserve’s balance sheet. Each forthcoming report on inflation is likely to receive heightened scrutiny as the market tries to discern the likelihood of an interest hike in December. This could increase the attention on this week’s CPI report (due to be released on Thursday).

Themes… Multiple commodities have broken out to new multi-year highs in 2017, wage growth has been relatively muted, and inflation overall has retreated from its recent high. Select commodities are due for a breather but watching how this theme plays out will be important.

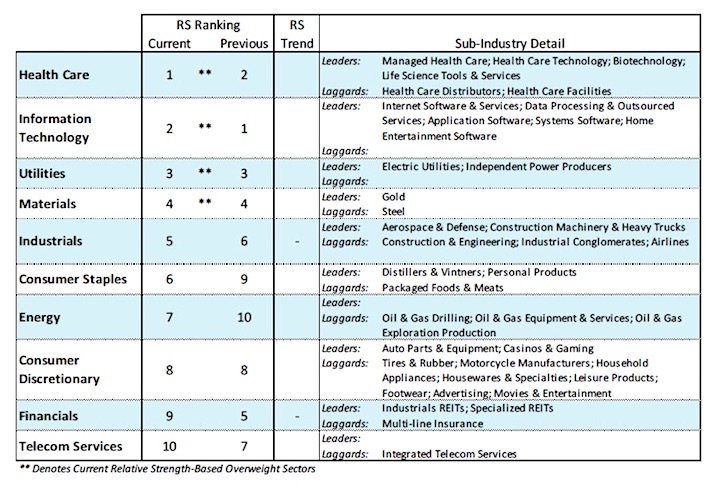

Bond yields are bouncing this week, but the overall decline has weighed on the Financials sector, which has seen a sharp drop in relative strength in recent weeks. Absolute and relative weakness by the Broker/Dealer group, which tends to be a leading indicator for the market overall, argues against a “lasting” near-term upside breakout in the S&P 500.

Stocks entered this week on slightly firmer footing as the new low list has contracted and the number of stocks making new highs has begun to expand again. This improvement is encouraging given the deterioration that had been seen across a variety of breadth indicators since earlier this summer. More gains are needed if the popular stock market averages are to do more than just test their recent highs. The percentage of S&P 1500 industry groups in uptrends has dropped toward 55%, and more than one-third of the stocks in the S&P 500 are trading below their 200-day average.

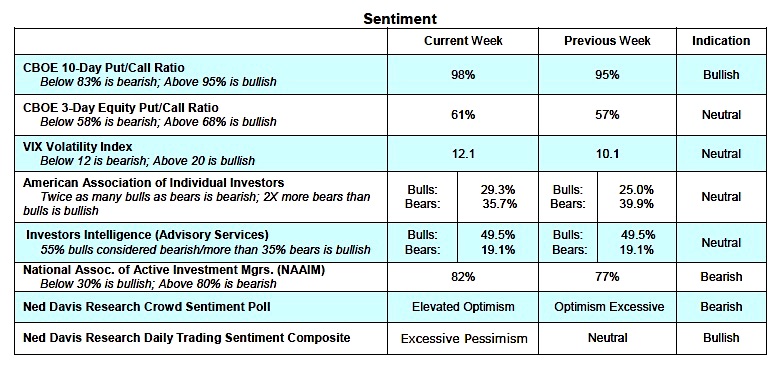

Stability in the broad market is important given the otherwise challenging technical backdrop for stocks. Momentum remains lackluster, investor optimism remains elevated, and stocks have entered a seasonal period that can at best be described as challenging (even if the sordid history of years ending in “7” is not given undue weight). The trading range of the past two months is being pressured to the upside but broad participation is necessary for it to last.

Twitter: @WillieDelwiche

Any opinions expressed herein are solely those of the author, and do not in any way represent the views or opinions of any other person or entity.