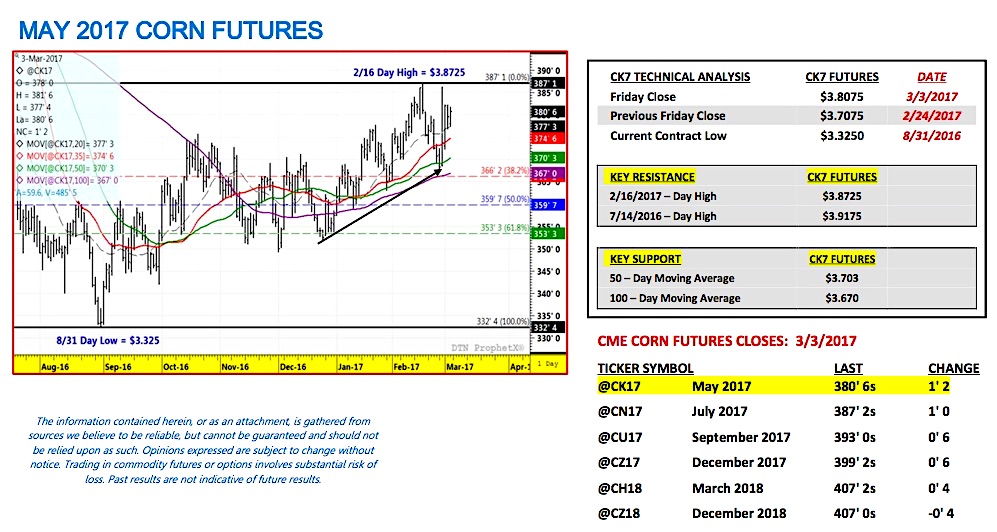

May corn futures moved higher this week, closing up 10-cents per bushel week-on-week, finishing on Friday (March 3) at $3.80 ¾.

On Tuesday, May corn futures took a run at the recent 2017 day high of $3.87 ¼; coming within a penny. However ultimately the buy paper hesitated and corn futures drifted back lower the rest of the week.

WEEKLY MARKET HIGHLIGHTS (2/27 – 3/3):

On Tuesday corn futures reacted positively to a report that President Trump was close to issuing an executive order that would materially alter the Renewable Fuel Standard. Sources indicated that Carl Icahn, special advisor to President Trump, had struck a deal with the Renewable Fuels Association on shifting the “point of obligation” for meeting biofuels quotas from refiners to fuel blenders in exchange for a waiver allowing for year-round blends of E15 (gasoline blended with 15% ethanol).

Corn Bulls immediately gravitated to the suggestion of E15 possibly becoming a reality, which in turn created what proved to be a very short-lived, yet entertaining 15 ¼-cents per bushel rally in December corn futures. This move resulted in a new 8-month high of $4.04 CZ7 being achieved mid-session. However as additional details pertaining to the legitimacy of the purported deal became public, the buy paper largely evaporated. December corn futures still managed a 5-cent higher close at $3.93 ¾ that afternoon, albeit well off the day highs.

What are the key takeaways from Tuesday’s RFS news thread and the ensuing price reaction?

- Any changes to the RFS will likely not come via an executive order. The fallout from this story, which has since been discredited from the White House, has been both swift and contentious. Icahn, who is the majority owner of a refiner (CVR Energy) has taking his share of condemnation for orchestrating a deal that would seemingly financially benefit his interests directly. Therefore I would not be surprised to see President Trump remove Icahn from having any specific involvement concerning the regulatory future of the Renewable Fuels Standard moving forward.

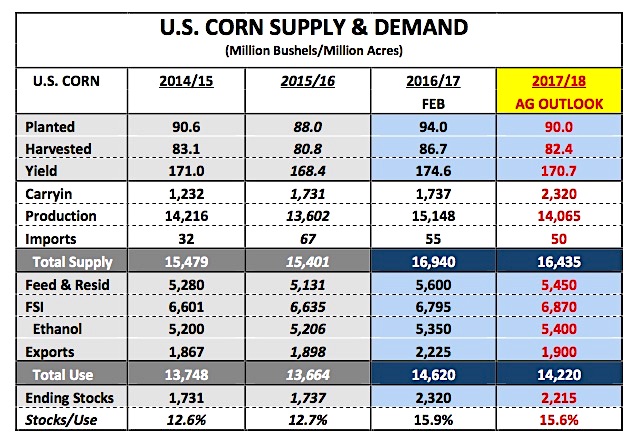

- That said Tuesday’s corn futures price action revealed just how big of a game changer a move to E15 in the U.S. gasoline supply would be for both the ethanol industry, as well as, the corn market. Consider that 5,350 million bushels of U.S. corn (or 37% of total U.S. corn demand) will be consumed in the 2016/17-crop year to produce ethanol. And yet ethanol’s current market share in gasoline blends has largely been capped due to what’s known in the industry as the E10 Blend Wall (gasoline blended with 10% ethanol). Suffice it to say should a future transition to E15 actually occur; corn demand for ethanol would once again increase exponentially. It’s the one major demand center that maintains the element of potentially massive increases, assuming some of the current obstacles to higher ethanol blends are eliminated.

What is the short-term price impact for corn futures?

Clearly this story has already exceeded its 24-hour shelf life. Therefore I don’t think it will provide any sustainable upward momentum over the short-term, especially given the market’s inability to close over the recent day high in May corn futures from 2/16 of $3.87 ¼ during Tuesday’s session. It’s apparent that pushing through and over that key area of price resistance will necessitate a storyline with actual staying power. That said long-term the RFS is still something that needs to be addressed by the Trump administration. Let’s not forget Trump won the election with a number of key Corn Belt states voting for him (Iowa, Michigan, Ohio, and Wisconsin all voted Trump in 2016 versus Obama in 2012). Iowa stands out the most given its standing as the largest state corn and ethanol producer in the country. Approximately 47% of all the corn grown in Iowa is used to produce ethanol. Therefore I’d be very surprised to see Trump issue an executive order with potentially negative consequences for either Iowa corn or ethanol producers.

KEY CK7 PRICING CONSIDERATIONS FOR THE WEEK ENDING 3/3/2017:

May corn futures (CK7) closed on Friday (3/3) at $3.80 ¾ finishing up 10-cents per bushel week-on-week.

Key takeaways from this week’s price action:

- The higher weekly close in May corn futures was without question a welcomed signal for Corn Bulls. That said Tuesday’s price action in particular was also a strong indicator that it’s going to take a real fundamental story of substance to take out and close over the 2/16 day high in May corn futures of $3.87 ¼. On Tuesday (2/28) May corn futures managed a day high of $3.86 ¼, riding the coattails of the RFS and E15 newsflash; however it was clear buyers were still hesitating at that key resistance area, unwilling to chase longs until the ethanol storyline had been fully vetted. That tells me the 2/16 day high is something technicians are watching closely. The same pattern emerged in December corn futures with CZ7 trading up to a day high of $4.04 on Tuesday (2/28), slightly higher that it’s 2/16 day high of $4.03 ¾; however once again the buy paper resisted pushing their bids at that level.

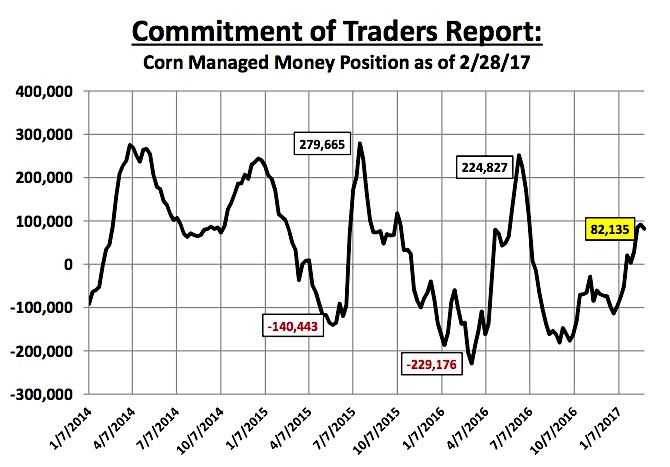

- Friday’s Commitment of Traders report also showed Money Managers taking a step back versus continuing to expand their current net long positions in both corn and soybeans. As of the market close on 2/28, the Managed Money long in corn stood at 82,135 contracts, down -10,081 contracts week-on-week. In soybeans the paper flow was similar with Money Managers trimming their net soybean long to 131,576 contracts, down -22,731 contracts week-on-week. I still believe the money wants to own both corn and soybeans this spring; however with U.S. and World ending stocks in both commodities still at record to near record levels, buyers can afford to be patient. Furthermore I too would hesitate before adding longs above key resistance considering the U.S. is still several weeks away from spring planting in the Corn Belt.

I’m still seeing strong support on corrections (i.e. 50-day moving average = $3.703 in May corn futures, 100-day moving average = $3.67). Additionally the 5 and 10-year seasonal patterns still favor sideways to higher corn prices at least through mid-May.

Thanks for reading.

Twitter: @MarcusLudtke

Author hedges corn futures and may have a position at the time of publication. Any opinions expressed herein are solely those of the author, and do not in any way represent the views or opinions of any other person or entity.

Data References:

- USDA United States Department of Ag

- EIA Energy Information Association

- NASS National Agricultural Statistics Service