To further appreciate the ramifications of the reigning economic regime, consider that China gained full acceptance into the World Trade Organization (WTO) in 2001. The trade agreements that accompanied WTO status and allowed China easier access to U.S. markets have resulted in an approximate quintupling of the amount of exports from China to the U.S. Similarly, there has been a concurrent increase in the amount of credit that China has extended the U.S. government through their purchase of U.S. Treasury securities as shown below.

The Company Store

To further understand why the current economic regime is tricky to change, one must consider that the debts of years past have not been paid off. As such the U.S. Treasury regularly issues new debt that is used to pay for older debt that is maturing while at the same time issuing even more debt to fund current period deficits. Therefore, the important topic not being discussed is the United States’ (in)ability to reduce reliance on foreign funding that has proven essential in supporting the accumulated debt of consumption from years past.

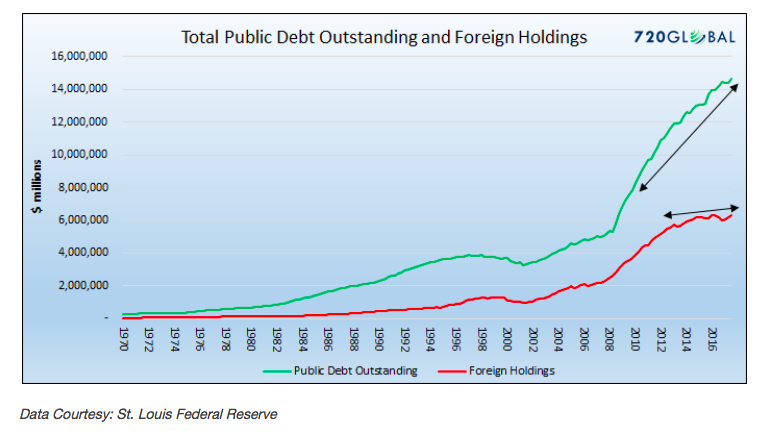

Trump’s ideas are far more complicated than simply leveling the trade playing field and reviving our industrial base. If the United States decides to equalize terms of trade, then we are redefining long-held agreements introduced and reinforced by previous administrations. In breaking with that tradition of “we give you dollars, you give us cheap goods (cars, toys, lawnmowers, steel, etc.), we will most certainly also need to source alternative demand for our debt. In reality, new buyers will emerge but that likely implies an unfavorable adjustment to interest rates. The graph below compares the amount of U.S. Treasury debt that is funded abroad and the total amount of publicly traded U.S. debt. Consider further, foreigners have large holdings of U.S. corporate and securitized individual debt as well. (Importantly, also note that in recent years the Fed has bought over $2 trillion of Treasury securities through quantitative easing (QE), more than making up for the recent slowdown in foreign buying.)

The bottom line is that, if Trump decides to put new tariffs on foreign goods, we must presume that foreign creditors will not be as generous lending money to the U.S. Accordingly, higher interest rates will be needed to attract new sources of capital. The problem, as we have discussed in numerous articles, is that higher interest rates put a severe burden on economic growth in a highly leveraged economy. In Hoover’s Folly we stated: Further adding pressure to U.S. Treasury securities and all fixed income securities, a weakening dollar is inflationary on the margin, which brings consideration of the Federal Reserve and monetary policy into play.

It seems plausible that a trade war would result in potentially controversial intervention from the Federal Reserve. The economic cost of higher interest rates would likely be too high a price for the Fed to sit idly by and watch. Such policy would be controversial because it would further blur the lines between monetary and fiscal policy and potentially jeopardize the already tenuous independent status of the Fed.

Importantly, this is not purely a problem for the U.S. Still the world’s reserve currency, the global economy is dependent upon U.S. dollars and needs them to transact. Any disruption in economic activity as a result of rising U.S. interest rates, the risk-free benchmark for the entire world, would most certainly go viral. That said, for the godless Communist regimes of China and Russia, a moral barometer is not just absent, it is illegal. Game theory, considering those circumstances and actors, becomes infinitely more complex.

Summary

Investors concerned about the ramifications of a potential trade war should consider how higher interest rates would affect their portfolios. Further, given that the Fed would likely step in at some point if higher interest rates were meaningfully affecting the economy, they should also consider how QE or some other form of intervention might affect asset prices. While QE has a recent history of being supportive of asset prices, can we assume that to be true going forward? The efficacy of Fed actions will be more closely scrutinized if, for example, the dollar is substantially weaker and/or inflation higher.

There will be serious ramifications to changing a global trade regime that has been in place for several decades. It seems unlikely that Trump’s global trade proposals, if pursued and enacted, will result in more balanced trade without further aggravating problems for the U.S. fiscal circumstance. So far, the market response has been fidgety at worst and investors seem to be looking past these risks. The optimism is admirable but optimism is a poor substitute for prudence.

In closing, the summary from Hoover’s Folly a year ago remains valid: It is premature to make investment decisions based on rhetoric and threats. It is also possible that much of this bluster could simply be the opening bid in what is a peaceful renegotiation of global trade agreements. To the extent that global growth and trade has been the beneficiary of years of asymmetries at the expense of the United States, then change is overdue. Our hope is that the Trump administration can impose the discipline of smart business with the tact of shrewd diplomacy to affect these changes in an orderly manner. Regardless, we must pay close attention to trade conflicts and their consequences can escalate quickly.

Thanks for reading.

Twitter: @michaellebowitz

Any opinions expressed herein are solely those of the author, and do not in any way represent the views or opinions of any other person or entity.