“The words of men may temporarily suspend but they do not alter the laws of financial dynamics. The fundamentals always take precedence eventually”- 720 Global on 11/30/2015

The quote above was from “Washington’s Warning” an article that scrutinized stock buybacks and the unforeseen impacts they may have. In that piece as well as an earlier missive, “Buybacks; Connecting Dots to the F-word”, we rebuked the short-termism stock buyback fad. Both articles made the case that corporate executives, through stock buybacks, promote higher short-term stock prices that serve largely only to benefit their own compensation. The costs of these actions are felt later as the future growth for the respective companies, employees and entire economy are robbed.

The ConocoPhillips (COP) Poster Child

This case study details how the “the laws of financial dynamics” have caught up with ConocoPhillips (COP) and demonstrates, in my opinion, how shareholders are suffering while executives prosper.

$COP

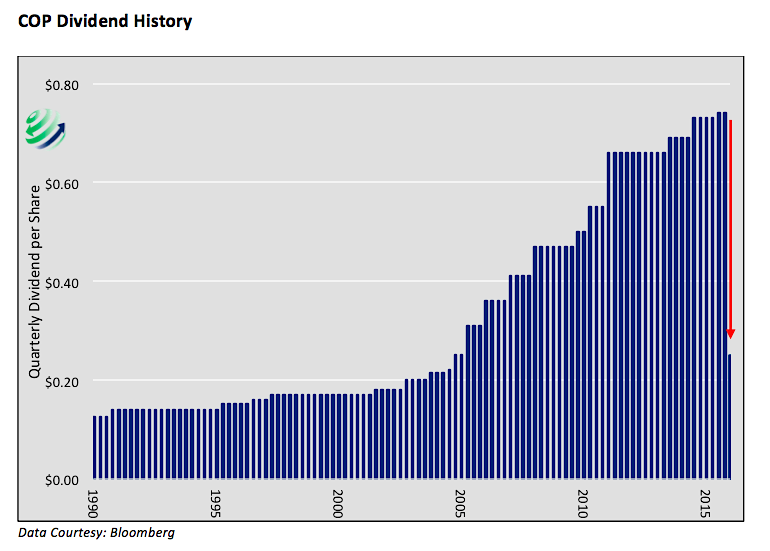

On February 4th, 2016 ConocoPhillips (COP), in reaction to their fourth quarter earnings release, slashed its quarterly dividend from $0.74 to $0.25 per share, a level not seen since March 2005. COP also lowered its current year capital expenditure (capex) budget by $1.31 billion, marking the second reduction in as many months. The actions are a direct response to the plummeting price of crude oil and the damage it is having on COP’s bottom line. The company’s net loss for the fourth quarter 2015 was $3.50 billion or $0.90 per share.

While the losses and expense cuts are not shocking given the severe decline in crude oil prices, the dividend cut was a jolt to many investors. ConocoPhillips has consistently paid a dividend, as shown below, since 1990. During that 25 year period the dividend was increased 19 times but COP had never decreased it, until now. Even during the financial crisis of 2008/09, COP raised its dividend despite the price of crude oil dropping $100 per barrel.

Maybe the biggest cause for the shock is not the steadfastness of their prior dividend policy, but official corporate presentations. On the first page of their 2016 Operating Plan (Analyst & Investor Update – December 10, 2015) they make the following statements: “Dividend is highest priority use of cash” and “DIVIDEND Remains Top Priority”. The statements are repeated in the summary on the final page. The cover of their most recent annual report has a word cloud diagram with “dividend” shown among other key corporate values.

What Could Have Been

The dividend and capex reductions are prudent measures undertaken by management to help manage corporate assets and bolster their financial conditions during an historic swoon in revenue. This article does not question those actions, it instead asks if such drastic measures would be necessary had management not spent enormous sums of capital on corporate stock buybacks in the preceding years.

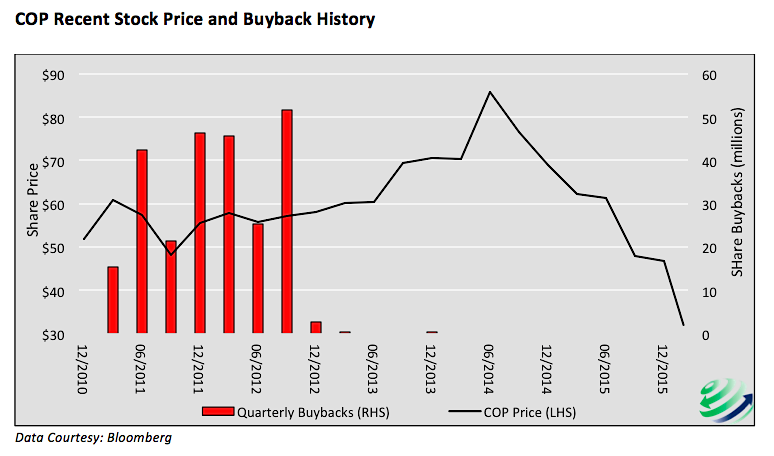

Since 2011, ConocoPhillips repurchased 251.316 million shares representing roughly 20% of their shares outstanding, at an approximate cost of $14.168 billion. The majority of these purchases occurred between 2011 and 2012 when the stock traded between $48 and $58 per share. Today the stock trades at $32 per share, matching prices last seen 12 years ago. The graph below charts the share price of COP with an overlay of the share repurchases (stock buybacks) by quarter.

Now let us contemplate what COP’s current financial situation might look like had management and the board of directors not engaged in stock buybacks / share repurchases. First of all, COP would still have the $14.168 billion spent on corporate stock buybacks since 2011, which could be used to support the $0.74 per share dividend for almost 5 years. More importantly, the company could be in the envious position of employing the capital to buy assets that are being liquidated by other companies at cents on the dollar. Shareholders are suffering in many ways from the abuses of management in years past and likely will continue to do so for years to come.

continue reading on the next page…