While I was away from my desk, the core stock market ETFs we follow (i.e. the Economic Modern Family) stayed busy.

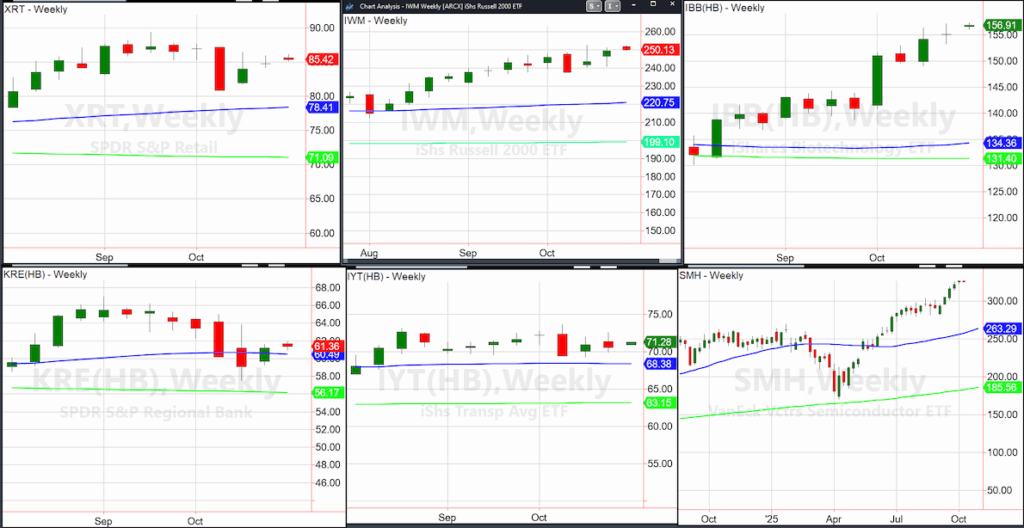

As of today, on the weekly charts, only the Semiconductors Sector ETF (SMH) and the Biotechnology Sector ETF (IBB) seem to be as optimistic as the S&P 500, Dow Industrials, and NASDAQ 100.

While SMH (Semiconductors) makes a new all-time high, IBB (Biotechnology), while doing well, remains under its peak high from 2021.

Plus, the Retail Sector ETF (XRT) and Regional Banks ETF (KRE) are two of the weakest links amongst these core ETFs.

The Russell 2000 ETF (IWM) sits just below the all-time high price established 2 weeks ago.

All in all, the price action is mixed and more neutral than bullish.

That is divergence.

Looking at the Transportation Sector ETF (IYT), the price is barely above the 50-Day Moving Average (blue).

From early October until now, the price is stuck in the middle of the high and low of the month.

IYT grossly underperforms the S&P 500 ETF (SPY) looking at the Leadership indicator.

And Real Motion and the red dots have gained momentum, but nothing is all that notable.

So why then, with all time highs in tech and the indices, is this very important sector to the US economy so meh?

The under-performance of the U.S. Transportation Sector (often proxied by the Dow Jones Transportation Average/ “Transports” index) relative to the Dow Jones Industrial Average (DJIA) and broader equities can be traced to several inter-related structural, cyclical and investor-sentiment drivers.

- Markets see weaker “goods/logistics” growth ahead (or are discounting a slowdown) versus the industrial/growth side of the market.

- Transportation firms face rising operational costs (fuel/maintenance/labor/insurance)

- The move in the economy toward services and digital goods reduces “heavy goods movement” growth as a share of total activity.

- Investor perception: if a slower growth/soft landing (or mild recession) is anticipated, transportation lags early, so it is being discounted ahead of other sectors.

Looking back at the IYT Daily chart, 2 closes over the 50-DMA will be positive and a return to a bullish phase.

However, with Regional Banks, Retail, and now this sector so underperforming, we do not want to see this as a canary in a coal mine.

Transportation is more cyclical, facing weak freight/demand growth, margin/cost headwinds, and has a lesser growth narrative compared to tech/growth sectors driving the market.

Weak links cannot become anchors.

Again, before you cross the street, it is always prudent to look both ways.

Twitter: @marketminute

The author may have a position in mentioned securities at the time of publication. Any opinions expressed herein are solely those of the author and do not represent the views or opinions of any other person or entity.