In spite (no, actually because of) last week’s flatlined +0.1% Q1 Advance GDP Growth reading (published by the BEA here), Goldman Sachs’ Kris Dawsey announced in a note to clients that the firm anticipates “a solid bounce-back in activity in Q2”, aggressively pushing their estimate for next month’s Preliminary reading “up to 3.9%.”

A +3.8% swing in quarter-over-quarter GDP growth is uncommon enough; but that doesn’t quite cover it. Citing “adverse weather, a large inventory correction, and a likely temporary drag from net exports” the firm sees the BEA revising it’s Q1 figure down in the Preliminary and Final readings to -0.6%. If correct (we know: but just entertain this notion for a moment), the net Q/Q change in GDP Growth would approximate +4.5% (note this is net change, not the absolute growth rate).

Does that sound like a lot? In the 268 quarters (since Q1 1947) that the BEA has tracked GDP Growth (data here) , Q/Q GDP Growth has exceeded +4% only 13.4% of the time. Nearly every quarter was immediately post-crisis, whether in the market, economically or geopolitically: the periods immediately after World War II, the Korean War, the 1973 Oil Crisis and all-but-forgotten Crash of 1973-1974 and the Early 1980s Recession account for nearly all of them in the first 50 years of data.

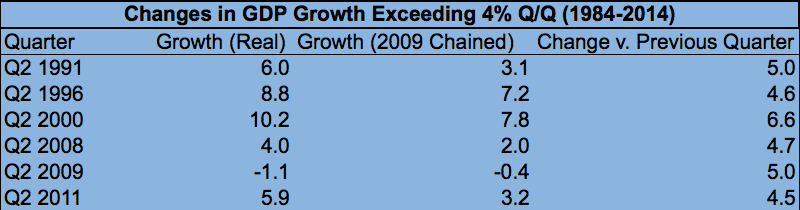

In the last 30 years, the number of Q/Q +4% swings has decreased precipitately. In the 120 or so quarters since Reagan’s second term began, Q/Q GDP Growth has exceeded +4% only six times, or about 2% of the time.

Goldman could be right; and given the emergent data and Advance reading, it’s increasingly clear their estimate for Q1 2014 is correct (inscrutably, they’re much better with retroactive estimates v. forecasts). This only serves to bring their outlying Q2 estimate into greater relief.

The six times the Q/Q change was over +4% in the last 30 years, they also (with one exception) came during or just after crisis, including the Early 1990s S&L Crisis/Recession, amidst the D0t-Com bust and that recession, bookending the most intense passage of most recent debacle and lastly the US Debt Crisis/S&P Downgrade. Interestingly, they’ve all been in Q2. Like every other stat produced by the mid-Nineties, 1996 stands alone. Here they are:

World War II, Oil Shock/Market Crash, Deep Recessions, Near-Failure of the Global Financial System, Sovereign Debt Crisis…and if Goldman (among others) is even vaguely right, you can add: Unusually Cold Winter.

Twitter: @andrewunknown and @seeitmarket

Author has no exposure to any securities mentioned at the time of publication. Commentary provided is for educational purposes only and in no way constitutes trading or investment advice.

Any opinions expressed herein are solely those of the author, and do not in any way represent the views or opinions of any other person or entity.

: Worrisome to Broader Market?")