Earlier this week Analog Devices (NASDAQ:ADI) announced a $14.8B deal for Linear Tech (NASDAQ:LLTC), one of the largest Tech deals this year. This follows a flurry of semiconductor deals across the industry, boosting the sector (NASDAQ:SOXX).

Less than two weeks ago Softbank announced a $28B deal for ARM Holdings (NASDAQ:ARMH) in another chip deal. The semiconductor deals are coming at a high price as well, ARMH bought at 16.8X next year’s sales and LLTC at 8.2X.

A few other semiconductor deals in the industry over the past 18 months include:

- ASML Holding (ASML) bought Hermes Microvision for $3B in June

- Cavium (CAVM) bought Q-Logic (QLGC) for $1.36B in June

- NXP Semi (NXPI) sold Standard Products for $2.75B in June

- ON Semi (ON) bought Fairchild Semi (FCS) for $2.4B in November

- Western Digital (WDC) bought SanDisk (SNDK) for $19B in October

- LAM Research (LRCX) bought KLA-Tencor (KLAC) for $10.6B in October

- Skyworks (SWKS) attempted to buy PMC Sierra (PMCS) for $2B in October, but was outbid by MicroSemi (MSCC)

- Mellanox (MLNX) bought EZ-Chip Semi (EZCH) for $811M in September

- Dialog Semi bought Atmel (ATML) for $4.6B in September

- Intel (INTC) bought Altera (ALTR) for $16.7B in June 2015

- Avago (AVGO) bought Broadcom (BRCM) for $37B in May of 2015

- NXP Semi (NXPI) bought Freescale (FSL) for $11.8B in March of 2015

Even more interesting is the fact that a lot of the larger players in semiconductor land have a lot of Mergers & Acquisitions (M&A) firepower at hand. And further, many have indicated willingness to add to the current flurry of semiconductor deals. Texas Instruments (TXN), Qualcomm (QCOM), Broadcom (AVGO), NXP Semi (NXPI) and Intel (INTC) are five of the largest names. Applied Materials (AMAT) and Taiwan Semi (TSM) are two other names, though their intentions in M&A are less clear. ADI and LRCX are coming off mega deals, so are not likely to do any other deals in the near-term. Skyworks (SWKS) has shown intent to be an acquirer as it needs to diversify away from Smartphones, and lost out on a $2B deal for PMCS last year. Slowing growth across the industry is causing the need for acquisitions to boost numbers, and to enter more favorable end-markets. It is well-known that slowing industry growth leads to increased M&A as management seeks cost synergies and revenue growth to maintain and enhance EPS growth. The strongest themes in Semi right now are in Auto, Data Center, and IoT.

Screening for potential M&A candidates involves looking for companies with positive growth, above industry-average margins, and to a lesser extent companies with a higher cost structure (acquirer could drive down costs and realize gains) and cheaper than average EV/Sales.

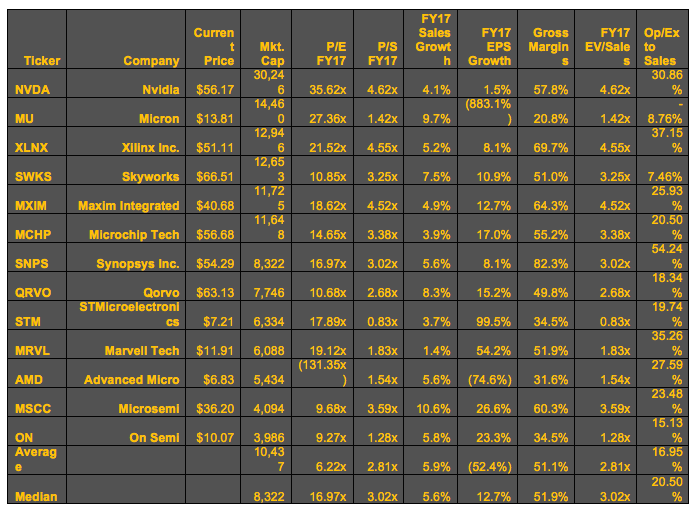

For easier comparisons I will break this down by size, first looking at $4B+ market cap Semiconductor companies that could be targets in a sizable deal. A breakdown of the key metrics is below:

Xilinx (XLNX) and Maxim (MXIM) are the two main names often mentioned as takeover targets for potential semiconductor deals. And from an options activity perspective, they are also the two that are seeing consistent large OTM call buying. Note as well that QRVO/ON each have seen some bullish activity for August expiration.

XLNX makes a lot of sense with its high Operating Expenses / Sales ratio combines with above-average margins, and it also a lot of new products contributing strong revenue growth.

Read more from Joe: Smart Money Positions For Rotation Into Financials

MXIM also has very good margins and its strong presence and growth in Automotive makes it a very attractive target.

Microsemi (MSCC) at 3.59X Sales with one of the best growth profiles and 60% margins stands out as a perfect target, even though it is coming off a $2B deal for PMCS. It has a lot of key customers across Communications, Aerospace/Defense, and Industrial markets. It’s Smart-Fusion 2 consumers far less power than competing chips, and it has strong exposure to security solutions/services, which is a focal point going forward with so many connected devices.

Marvell (MRVL) has struggled over the years but trades very cheap at 1.83X Sales and a high OpEx/Sales ratio above 35%. The issue is its end-markets of Storage, Mobile, and Networking are not all that exciting in terms of future growth.

Nvidia (NVDA) is a best of breed name that is involved in a lot of strong markets (Auto, Gaming, AR/IR) and it has better than average margins, but also is prices above every other name in the group, and them becoming a buyer may be more likely.

Synopsys (SNPS) is a name that really sticks out with its high OpEx/Sales ratio, a name that could benefit from a deal, and gross margins above 82% are outstanding. SNPS is involved in the electronic design automation (EDA) market, and is more of a provider to the Semiconductor industry, not a chip maker, so it is probably not the best comparable for this study. It is more comparable to Cadence Design Systems (CDNS). SNPS paid $507M for Magma Design Automation in 2011, not long after Carl Icahn attempted to buy another EDA player Mentor (MENT). It’s an extremely concentrated industry, though could be interesting if a chip company wants to go this route, but I digress.

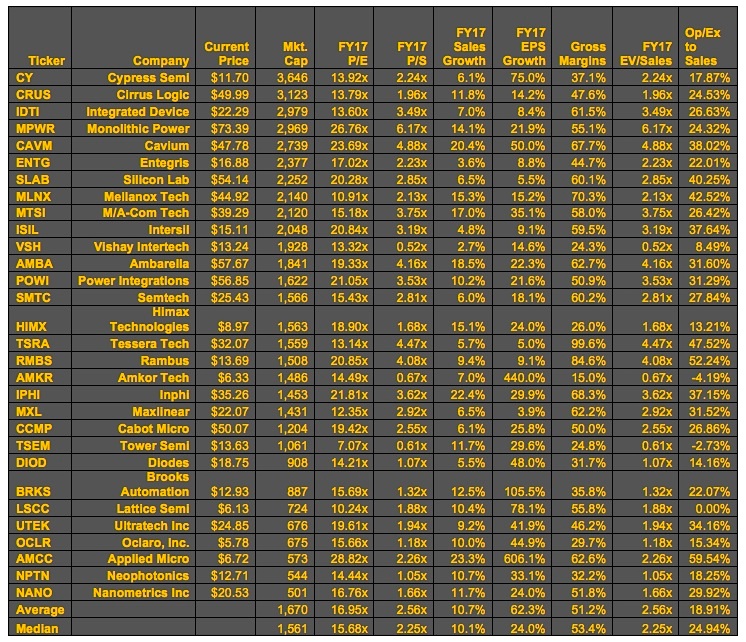

For the $500M to $4B group:

In this group I sorted by gross margins and then set up a multi-factor valuation approach looking at P/S valuations versus incremental to industry average margins. These names stick out as attractive M&A targets based on what acquirers will be using in searching for a target. The 7 top names came out as AMCC, CAVM, ISIL, IPHI, MXL, SLAB, and MLNX. CAVM is rich at 4.88X Sales and is undergoing a deal for QLGC, so not the best target.

But the other six names all have attractiveness for potential semiconductor deals.

continue reading on the next page…

: Showing Some Signs of Emerging Strength")