Do you like making money while you sleep? We, like many investors, enjoy that proposition.

It is that notion that supports the repurchase (repo) market.

The repo market is like the plumbing of the financial markets – critical for operation but not anything you pay attention to until it springs a leak; Well, last week the pipes started leaking.

What is the repo market?

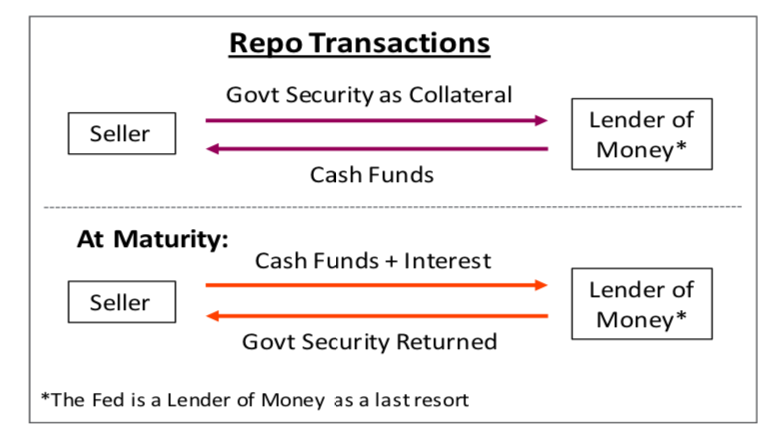

Here’s a simple explanation of the repo market: One party needs cash and sells an asset (typically a Federal government bond) to another party at a certain price and commits to repurchase that same asset for a different price on a future date (typically overnight or within a couple of days).

The price difference between these transactions is determined by the repo rate. If the borrower defaults and fails to return the cash, the lender keeps the government bond that was pledged as collateral.

A common example is when a bank that needs cash to meet customer demands. They undergo a repo transaction where they sell Treasuries to the Fed and agree to buy them back the next day (overnight repo agreement), at a slightly higher price. They tend to “roll” this transaction, doing it everyday, just adjusting the size of the transaction based on the amount of cash needed.

Why is it so important?

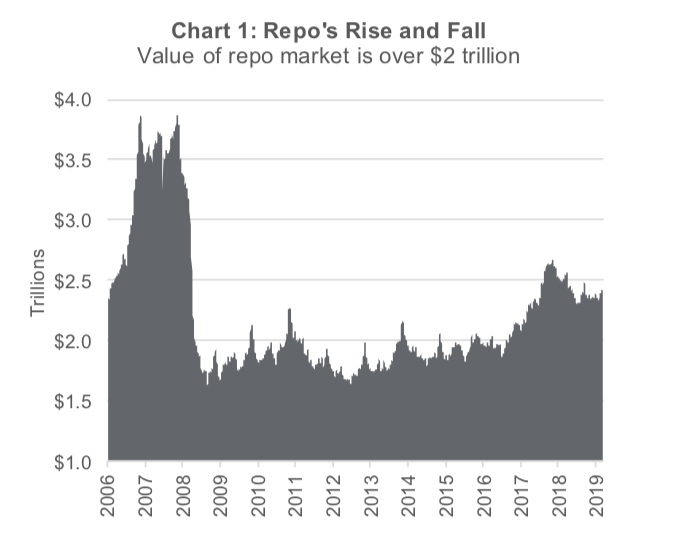

A traditional banking system is driven by the withdrawal of cash, backed by reserves. In contrast, the repo market is based on the withdrawal of repo agreements, backed by bonds. The repo market is crucial for a variety of financial transactions. It is also extremely large (Chart 1), currently over $2 trillion. These operations were fundamental to investment banks such as Bear Stearns and Lehman Brothers. During the 2008 financial crisis, the market lost faith in the bonds that were being used as collateral.

This prompted investors to pull out of the repo market all at the same time, similar to a traditional bank run. Arguably, the lack of liquidity in the repo market was the nexus of the last crisis, a fact that underscores the widespread interest in the latest situation, with the spike in the repo rate last week. However, since the last crisis, the U.S. Federal Reserve (Fed) has devised new rules to prevent such a calamity from happening again and this past week flexed that muscle.

What just happened?

Last week there was a series of events that caused the repo rate to spike and eventually forced the Fed to step in and ease market concerns. On September 16, corporate tax payments were due, making corporate America demand cash to pay uncle Sam. That, coupled with a treasury bond auction and continued strong demand for U.S. dollars from abroad, meant that there was insufficient cash in the U.S. financial system to meet those demands.

As we approach quarter end, concerns are mounting because banks will become more reluctant to liquidate their reserves and the need to make corporate tax payments will only increase.

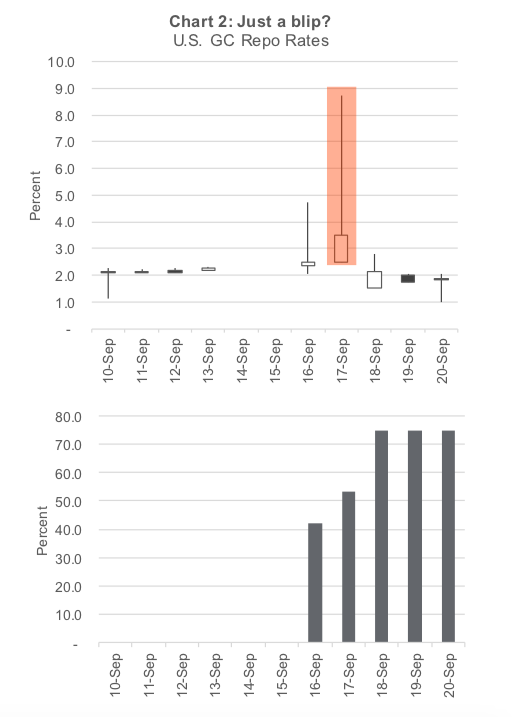

Last week things hit the fan with the repo rate going from 2% to almost 10% on September 17 as cash flowed out of the repo market. This caused the effective federal funds rate to rise to 2.3%, higher than the upper band of 2.25%. This occurred just as the Fed was reducing that upper band to 2% with a rate cut announced on September 18. It is important to note that although the rate spiked, it was a brief intra-day move on a limited number of transactions. The rate has moderated and as of today is lower than normal. Although a brief aberration, it is still worth understanding what happened and was is being done about it.

What is the Fed doing to fix the problem?

Chart 2 illustrates the massive spike in the repo rate at the beginning of last week as well as the cash made available by the Fed to lower and maintain the rate within the defined range. Being the lender of last resort, the Fed provided the liquidity the market needed to keep it functioning properly. But that was like putting duct tape on a leaky pipe – it was simply a patch job. The ‘central bank plumbers’ had to keep the patches coming as the week went on.

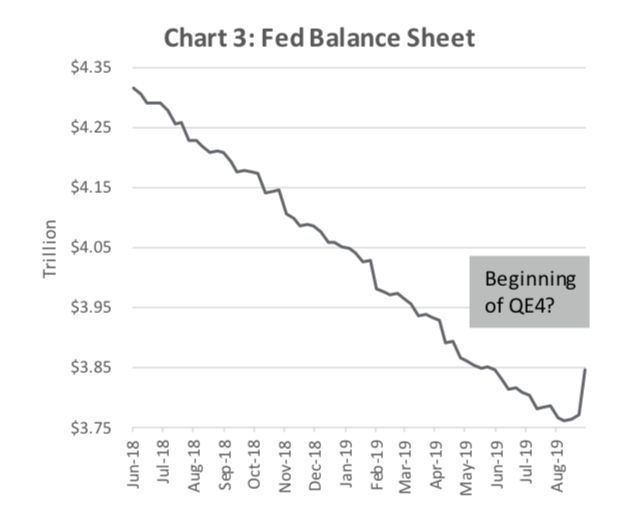

On September 20, the Fed announced that it would provide overnight repo operations for an aggregate amount of $75 billion a day until October 10 to help get the market through quarter end. Red Green would be proud of their pervasive use of duct tape! Fed chair Jerome Powell has set the stage with this balance sheet growth and has left many wondering if this is a precursor to further quantitative easing. Chart 3 illustrates the steady decline (quantitative tightening) of the Fed balance sheet and the recent spike higher.

Patch work has ramifications

Every U.S. dollar in circulation is a liability for the Fed. For all the cash in circulation, the Fed holds an equivalent liability on its balance sheet. And like any company, its liabilities need to match assets. The amount of dollars demanded continues to expand for a variety of reasons. This in turn is expanding the liabilities on the Fed’s balance sheet now that it is growing the other side of the balance sheet to offset that demand

So, should investors be concerned? It’s clear that the Fed should not be put in a position where it must step in to provide liquidity on a daily basis. For now it is working, but longer-term structural solutions should be in place to address the problem. There is evidence that the current dislocation in the market is more technical in nature, and temporary. However, this has shined a spotlight on a bigger issue: Despite low yields and a long bull run, liquidity risk remains and has likely been mispriced by the market for some time.

Source: All charts are sourced to Bloomberg L.P. and Richardson GMP unless otherwise stated.

Twitter: @ConnectedWealth

Any opinions expressed herein are solely those of the authors, and do not in any way represent the views or opinions of any other person or entity.

Flirting With Critical Support… Again")