The following article is a part of my Gone Fishing Newsletter that I provide to fishing club members each week to identify macro inflection points and actionable micro trade set-ups.

Incredibly Bullish Charts for Gold

The correction we experienced last week – wherein $2.6 Trillion was lost in the Global Stock Market – was due to the Velocity of the Rate Spike that triggered an Emerging Market and Volatility panic (the volatility index VIX doubled from my call) resulting in our market drop. At first, Gold (NYSEARCA: GLD) didn’t act as if it would be a safety play but on Day 2 it moved higher.

Since then, I have been ‘collecting’ evidence to support Gold as an Investment theme not just a Trade.

The Lurch

First, I had been waiting for “the lurch”… which is my technical term that happens to price AFTER huge volume has entered long and price stops moving down. This is my Tell that buyers are finally outflanking (absorbing supply of) the sellers. That was in play the week before our recent sell-off. Then AFTER markets sold off, Gold gained rapidly on Day 2 – more than 3% and by large percentages in individual miners. Since then Gold, Silver, Miners have been consolidating the “lurch”.

A similar trade was the US Dollar trade while it consolidated Jan-April of this year before it “lurched” forward for April-August (16 weeks of gains). Gold looks ready to do the same.

Shark Jumping

And Gold/Silver Miners appear to be preparing to ‘jump the shark’ – hurdle themselves over the apex of the descending wedge/trendline as shown below (GDX $21-22.50 price range). But as with shark-jumping, there is no Try….

Rotation Time

Since 1984, the S&P 500 to gold stocks ratio only reached today’s level once and mining stocks rallied almost 200% for the next 7 months. We should be close to an inflection point for historically undervalued gold stocks. @TaviCosta

Yuan Decoupling

The decoupling of the gold vs. USDCNH is among the greatest macro developments of late. With Chinese equity markets in free fall it’s becoming increasingly difficult for the PBOC to prevent the yuan from devaluing against both gold and USD. @TaviCosta

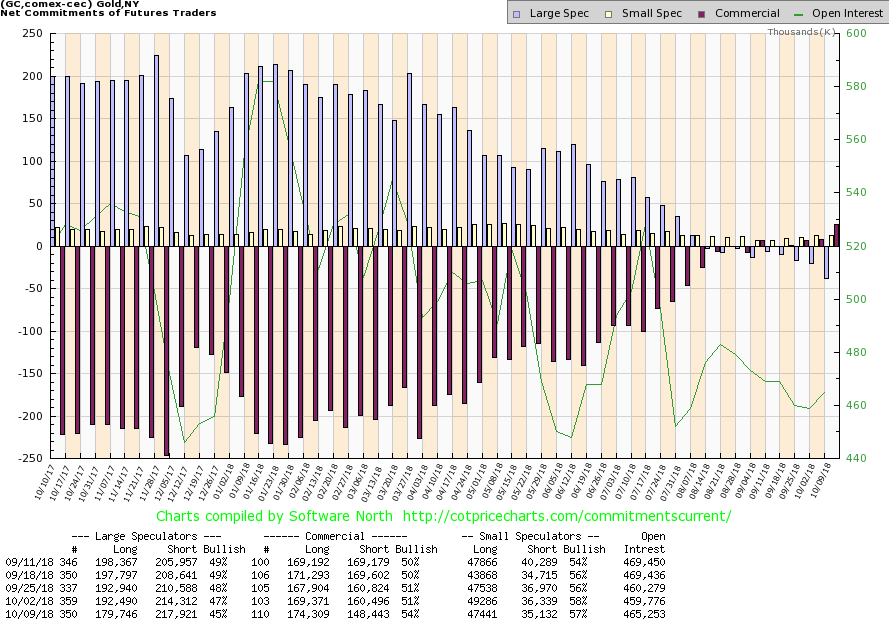

Anomalous!

Gold Commercials now NET LONG almost 26,000 contracts,,,,,HIGHLY HIGHLY ANOMALOUS. Richard in my Trading Room + 40yr Precious Metals MM.

Smart Money

Back in July, Richard wrote to share how Commercials – the smart money – were the least short since January 2017 and were getting closer to flat; managed futures managers had ‘abandoned the sector’ and the Major Gold producers were desperate for reserves. I share his thoughts as they are just as relevant then as now – even more so as we have traded down/through the seasonally weak period of Gold and should begin to emerge – assuming the above ‘decoupling’ thesis with Chinese Yuan holds true.

The smart money is considered the Commercials…..who are the least short they’ve been since January 2017. Remember Commercials will always have a bone fide reason for carrying shorts because the Commercial category includes parties holding physical long positions they need to hedge. Whenever the commercials get closer to being flat, like now, that is important. Also the managed futures managers have completely abandoned the sector. Hence the 99% reduction of their position in the sector. Another “tell” on the current sentiment.

As to Gold and the Gold stocks. First of all – a batch of big cap earnings came out for the majors in the last 24 hours. ABX GG NEM AEM …etc. they were all disappointing. The large cap producers are basically self liquidating entities that are unable to replace their annual production/depletion with newly found reserves. For that reason I am concentrating on the smaller cap GDXJ sector of the market. These large cap Gold companies are desperate for new reserves. I am invested in a small cap company that has a high grade surface gold deposit in Mexico and almost every major has been down there in the last two weeks and this is a discovery made only 3 months ago.

As for Gold. I am bullish based on COT positioning and sentiment … The Yuan slide as a result of the tariffs/currency war has really complicated things …. Gut feel we are very close to the end of this $1370/oz to $1210/oz washdown. We are $1230 now but as a veteran of the Gold sector you can never underestimate the ability of these mining companies to “under deliver”…

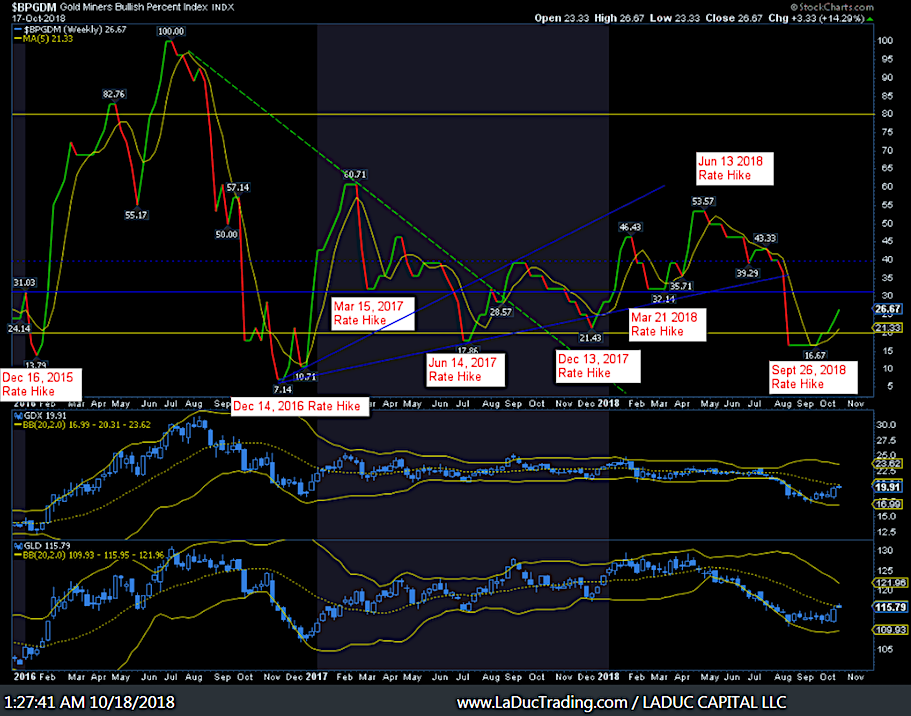

The Fed Tell

My favorite Intermarket analysis chart is still the “Fed Tell” – see if you can spot the pattern…

Threats Against Gold

Gold – sometimes fear/Central Bank distrust trade, sometimes currency/inflation trade, sometimes commodity/demand trade… but in 2018 it has clearly been a Yuan/Trade War Currency tool.To a degree, to trust in the Gold Trade is to put our trust in China as China represents a key risk for Yuan devaluation, even though their public talk is supportive Yuan:

“We will not engage in competitive devaluation, and will not use the exchange rate as a tool to deal with trade frictions” said PBOC Governor Yi Gang in his statement at the IMF meeting in Bali last weekend. With the Fed continuing to raise rates, a growth-focused PBOC keeping rates on hold will mean pressure for a weaker yuan

It doesn’t matter whether the proximate cause is offsetting the competitiveness drag from tariffs, or maintaining appropriate domestic liquidity conditions – the pressure on the yuan is in the same direction. @TomOrlik

Trump’s not-so-stealth tax on China Trade (I wrote about this in August) may have China rethinking their counter-cyclical factor to the yuan’s fixing. This is the 144-year-old postal treaty that has allowed Chinese companies to ship small packages to the United States at a steeply discounted rate. This is just another Trump Tariff on China and may be met with retaliation by China in the form of Yuan devaluation as it is not only a monetary policy to stem currency outflow from China but a tool in fighting Trump’s Trade War. This would be a headwind for Gold.

Summary

Market is complacent. As equities pull back, and inflation increases, a rotation will likely drive commodities like Oil higher into the $90s next year and metals e.g. Gold could quickly follow suit. As such, and in summary, here are my Top Reasons Gold is turning into an Investment:

- ‘Old-timers’ know, the 1st stages of a market correction is a Gold correction. We’ve likely had that correction in Gold this summer – $1370/oz to $1210/oz – as I warned in May.

- Central banks have accounted for a stunning 264 metric tonnes of purchases this year, or some 9.3 million ounces.

- Gold is in scarcity not abundance. New gold discoveries are rare indeed since Gold production peaked in 2015 and new mines takes many years to produce, if at all.

- Don’t be fooled; Gold can perform in a raising rate environment ( a la 1970s when Gold ran $34 to $900 and rates ran up from 5% to ultimately 16% in 1981).

- Inflation today is starting to surprise to the upside which can translate into overheating economies and rising inflation expectations. This is fuel for Gold’s advance.

- When markets flood with people going into cash – liquidity – the rotation into hard physical assets increases rapidly.

With that, we just had a market correction and I contend we are not done. More to the point of this article: Corrections Can Cause Gold Bulls to Stampede.

Come join me… I made it super easy for you to trade with me: 1. Pop into my LIVE Trading Room any time you want. 2. Get real-time Portfolio tracking of my trades with SMS/Email. 3. Think big picture with my macro-to-micro investment newsletter. You can also subscribe to my Free Fishing Stories Blog/Videos and find me on Twitter. Thanks for reading and have a great weekend!

Twitter: @SamanthaLaDuc @LaDucTrading

Any opinions expressed herein are solely those of the author, and do not in any way represent the views or opinions of any other person or entity.