Fortress Transportation and Infrastructure Investors (FTAI) is a new company I came across recently that looks to have upside into 2017.

It has a $1.03B market cap trading 0.96X Book and 8.4X EBITDA with a 9.68% dividend yield. Aviation leading is 52% of its business, Offshore Energy 16%, and Infrastructure at 31%.

FTAI leases 24 passenger aircrafts and 47 commercial jet engines and has no debt in its Aviation portfolio. Current development projects include Jefferson, a terminal in Texas for handling crude, ethanol and refined products; CMQR, a short-line railroad running from Montreal to Maine; Repauno, a privately owned seaport and multimodal hub near Philadelphia; and Hannibal, a privately owned industrial port and rail in the heart of Marcellus and Utica shale regions.

FTAI currently operates with a Debt/Capital ratio of 18% and targets a 50% long-term ratio. FTAI’s offshore energy segment has struggled with a lock of activity, but visibility and backlog improving into 2017. The company also owns and manages 83,000 shipping containers in a joint venture, but has a small impact to its top/bottom lines.

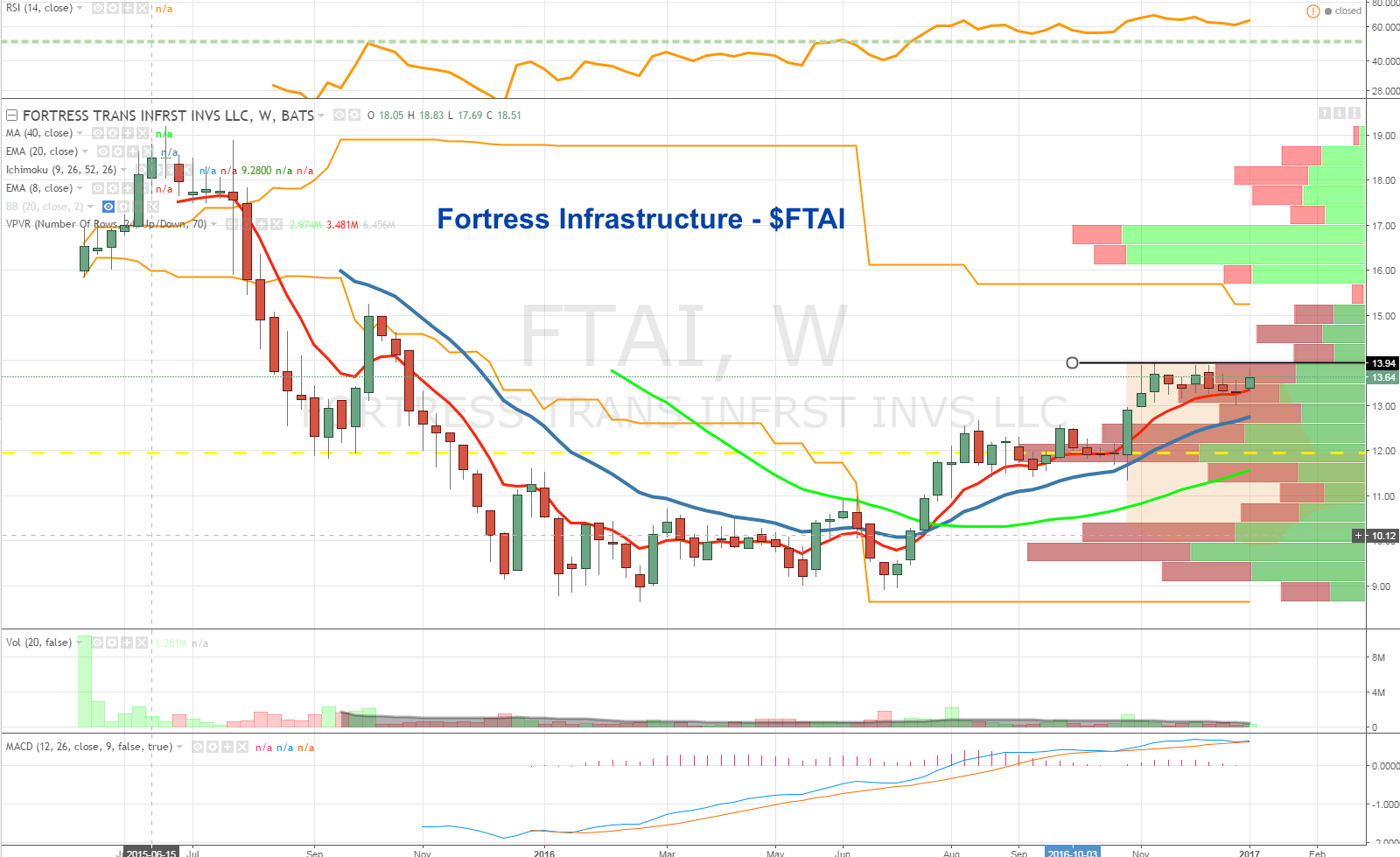

On the chart, shares are consolidating under the $14 level with a weekly bull flag and a volume pocket overhead to run to $15.70-$16.10, while traded as high as $19 in June of 2015.

In closing, the $1B company is not well known but offers an attractive yield and is well positioned in the US with upcoming developmental projects set to become further contributors to earnings. At less than book value with a strong balance sheet, shares look to have at least 30% upside.

Thanks for reading.

Twitter: @OptionsHawk

The author does not have a position in mentioned securities at the time of publication. Any opinions expressed herein are solely those of the author, and do not in any way represent the views or opinions of any other person or entity.

: Showing Some Signs of Emerging Strength")