The following is a recap of The COT Report (Commitment Of Traders) released by the CFTC (Commodity Futures Trading Commission) looking at futures positions of non-commercial holdings as of May 12, 2015. Note that the change is week-over-week.

10-Year Treasury Note: If we just focus on weekly closing prices, one would think that the 10-year yield had a boring week – closing essentially flat. But nothing could be further from the truth. From the intra-day low to high, the 10-Year yield swung 20 basis points. Last week, the range was 17 basis points. May is looking a lot like October last year, in which traders saw the yield swing between 1.87 percent and 2.17 percent in a single day.

Treasuries on the long end are showing some volatility. Early in the week, they got slammed even though the U.S. inflation and economic growth outlook remains subdued. It is possible that the sell-off in German bunds has begun to influence trader behavior. Or it could also be a lack of liquidity, both here and abroad. Food for thought: How willing are long-term holders such as insurance companies to lend their bonds these days?

There was a time mid-week when the 10-year yield broke out of its December 2013 downward sloping trendline, but it could not hold on to the breakout – data wouldn’t cooperate. From retail sales to industrial production to consumer sentiment, they all came in weaker than expected. The only silver lining was the weekly unemployment claims, but one has to wonder if claims are nearing an inflection point.

Looking at the COT report data, it is possible non-commercial traders covered some of their shorts. Monday, the 10-year shot up 12 basis points, followed by another six-basis-point rise the next day. It then gave it all back and some.

10 Year Note – Currently net short 132.4k, down 50.7k.

30-Year Treasury Note: The upcoming week will be important as it is packed with housing data.

The NAHB/Wells Fargo Housing Market Index for May comes out on Monday. April’s reading was 56, down slightly from the post-bubble high of 59 last September. Historically, builder confidence closely tracks both new-home sales and housing starts; currently, confidence has galloped ahead of both.

On Tuesday, investors will get housing starts data. Both February and March came in at under one million (SAAR). Post-bubble, housing starts slumped to as low as 478,000 (April 2009) and were as high as 2.3 million at the peak (January 2006). It’s worth noting, though, that builders haven’t been putting their money where their mouth is. Starts remain subdued, as does inventory.

Existing home sales for April are on tap for Thursday. March (5.19 million) was the highest since last September (5.26 million). The post-bubble recovery has seen home prices recover much faster than sales, which probably has priced out many potential buyers. The median price of an existing home peaked at $230,400 in July 2006. The post-bubble high of $222,000 in June 2014 never got quite that high but rose from $154,600 in January 2012. March came in at $212,100.

FOMC minutes for the March meeting are out on Wednesday. At the time, the mid-point of the central tendency of members’ estimates for real GDP growth this year stood at 2.5 percent. Since then, reacting to a barrage of weaker-than-expected data, consensus estimates have nudged lower, to 2.3 percent. It will be interesting to see what the committee thought was causing the weakness, which has softened further since.

It is also worth noting that four Fed officials, including the chair and vice-chair, are scheduled to speak this week. Chair Janet Yellen speaks at one o’clock on Friday afternoon and by then she will have seen April’s CPI data (that comes out that morning).

Last week, the 30-year yield managed to poke its head out of dual resistance, and it’s still above it. Technically, it is itching to go lower. Will the new support, which also approximates the 200-day moving average, hold?

30 Year Note – Currently net long 26.9k, up 15.9k.

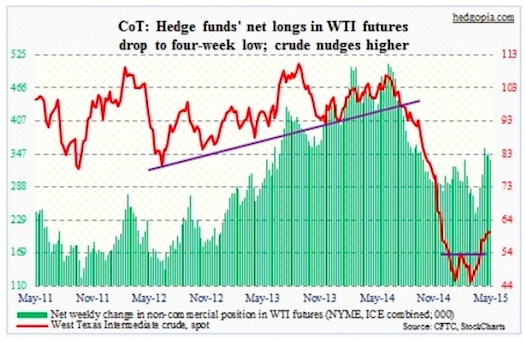

Crude Oil: The EIA raised its average forecast for West Texas Intermediate to $54.32/barrel this year from a previous forecast of $52.52, but lowered 2016 from $70.07 to $65.57. Year-to-date, spot WTI has averaged $51.36. If the EIA forecast is right, the crude has room to trade lower. Simplistically, if for the rest of the year the price remains unchanged from Friday’s close, it would have averaged $56.79 for the year, higher than what the EIA expects.

Global crude supplies continued to rise in April – by 3.2 million barrels per day year-over-year (courtesy of the IEA). This is huge. OPEC production remained high, as did production in Russia, Brazil, China, Vietnam and Malaysia.

OPEC’s next meeting is set for June 5th. And this data makes it unlikely that they will cut the current production quota of 30 million bpd. But perhaps thing will change by then. A Saudi official was quoted as saying the price drop has deterred investment away from expensive oil including U.S. shale, deep offshore and heavy oils. They appear to be happy with the status quo.

This is probably beginning to sink in for traders in the oil pits. For the second consecutive week, spot WTI has produced shooting stars/dojis on the weekly chart. The first line of support remains at 58, where buyers already showed up the past two Friday’s; 54 looks like a must-hold support level.

Crude Oil Futures – Currently net long 337.8k, down 10.3k.

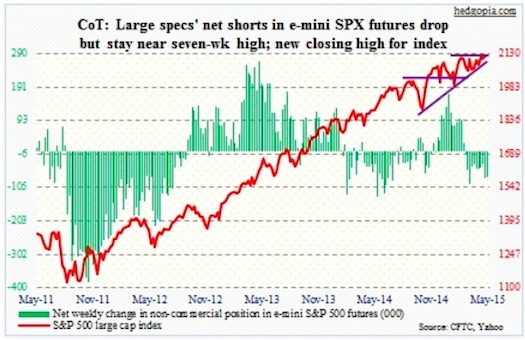

E-mini S&P 500: Another closing high for the S&P 500 Index this week… yet no breakout just yet. It’s worth noting that the broad large cap index never lost its October 2014 trend line, while other indices have; the Russell 2000 comes to mind. The gap between that trendline and its three-month lateral resistance is narrowing. It appears to be an ascending triangle. More often than not, this tends to resolve in a breakout, as that resistance continues to get pounded from down below.

The earnings bar continues lower. In and of itself, this is not good news, as it pushes multiples higher. But if the economy can shake off 1Q (1H?) weakness and come roaring back in 2H – which right at this moment is not looking like a safe bet – these lowered estimates can even nudge higher or lead to some surprises.

In the past three months, 1Q15 estimates for S&P 500 companies have gone from $27.98 to $25.93, 2Q15 from $29.99 to $28.56, 3Q15 from $31.02 to $29.98, 4Q15 from $32.32 to $31.69, 2015 from $121.31 to $116.16, and 2016 from $137.46 to $133.28. 2H15 estimates remain high, hoping the economy strengthens.

Per the COT Report data, Non-commercials continue to maintain a bearish bias. Would they be forced to cover if there’s a breakout?

SP E-Mini Futures – Currently net short 72.8k, down 6.5k.

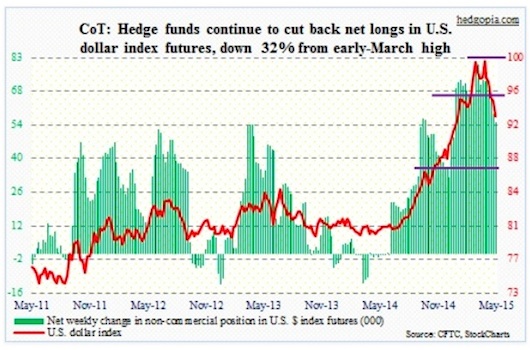

U.S. Dollar Index: The Russian Central Bank said it will be buying $100 million to $200 million a day from the domestic currency market. Russia’s reserves have shrunk from around $470 billion a year ago to $356 billion now. US Dollar purchases are designed to boost reserves, as well as weaken the ruble. But the news was not enough to stem the US Dollar’s downward trend.

Several bulls have left the once overcrowded US Dollar train. Non-commercials have reduced net shorts by 32 percent from early-March highs.

The US Dollar Index (93.18) is approaching a crucial technical level. Important Fibonacci support resides at 92.40; that marks a 38.2 percent retracement of the March 2014 to May 2015 rally. This could be a good spot to pause/stop the downward slide.

US Dollar Index Futures – Currently net long 55.3k, down 3.6k.

Euro: Eurozone GDP expanded 0.4 percent in 1Q sequentially, better than in the U.S. or the U.K. – it was the first time in four years this has happened. The question is: Is this self-sustaining? A lower euro probably went a long ways. However, from the mid-April low, the currency has rallied nearly nine percent.

Traders had amassed massive short bets in the currency, and they seem to be covering some of those; per the COT Report data, short holdings have declined 21 percent from the March-end highs.

Euro Futures – Currently net short 179k, down 11.2k.

Gold: Gold was one of several assets that failed to make sense this week, as a strong rally early in the week occurred as interest rates were rising. Could Gold be a safe-haven play again? Whatever led to the three-percent jump, Gold is now sitting just above both the 50-day and 200-day moving averages. Earlier, the metal straddled its 50-day for nearly five weeks before moving higher. Shorter-term moving averages, as well as the 50-day, have turned up.

A big technical test lies ahead, around $1,260.

Gold Futures – Currently net long 77.4k, up 5k.

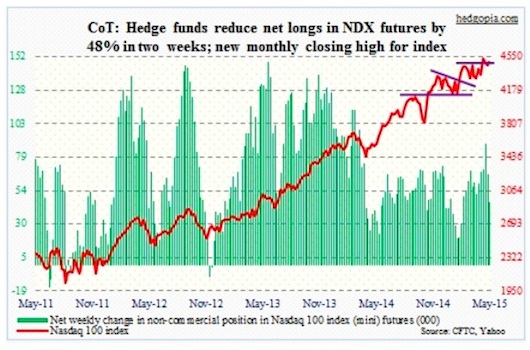

Nasdaq 100 index (mini): The 4480 level continues to be an important technical level (equates to $109 on the QQQ). On Friday, that level was defended once again.

Curiously, non-commercial traders have been cutting back net longs – down 48 percent in two weeks.

NASDAQ 100 Futures – Currently net long 66.9k, down 21.5k.

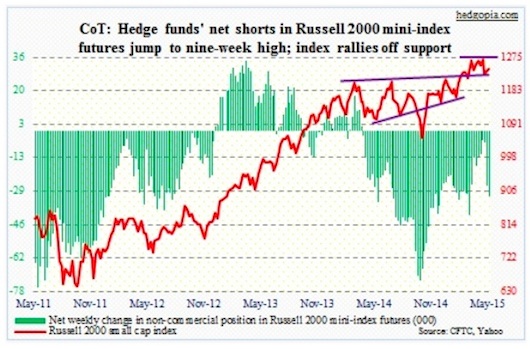

Russell 2000 mini-index: Three weeks ago, it suffered a double whammy, losing its 50 day moving average as well as the October 2014 trend line. The rally on Thursday (and Friday) stopped right beneath that average. The index has been under the 50 day for 12 straight sessions now. In contrast, both the S&P 500 and the Nasdaq 100 are comfortably above it. Even though the Russell 2000 is acting like a laggard, odds are good that it will soon retake that average. Note that shorter-term averages are turning up. It will be a different ball game if the Russell 2000 loses 1215.

These traders do not believe in the bullish scenario. They have been adding to net shorts.

Russell 2000 Futures – Currently net short 31.8k, up 5.1k.

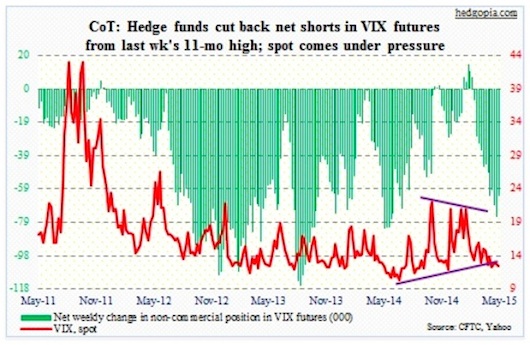

VIX: For the fifth time in the past five weeks, an attempt to push through 15 has been denied. Turns out these traders were prescient. Large specs’ rising net shorts in S&P 500 futures, the VIX to VXV ratio, the CBOE put-to-call ratio as well as the ISE equity call-to-put ratio were bearish, even as HRRI (below) and large specs’ VIX bets were sending bullish signals (see more here).

This week, these traders cut back a little, but net shorts still remain sizable.

As an aside, there has been a pickup in June call activity in recent sessions.

VIX Futures – Currently net short 63k, down 12.8k.

Thanks for reading.

Follow Paban On Twitter: @hedgopia

Read more from Paban on his blog.

No position in any of the mentioned securities at the time of publication. Any opinions expressed herein are solely those of the author, and do not in any way represent the views or opinions of any other person or entity.